Bearings are fundamental components in modern engineering, serving as the invisible backbone for virtually everything that rotates, rolls, or moves. From massive industrial wind turbines to the micro-motors found in medical devices, these precision-engineered components are critical for reducing friction and handling heavy mechanical loads. According to a comprehensive research report by The Insight Partners, the global bearing industry is currently experiencing a transformative growth phase, driven by rapid industrialization, automation, and the global shift toward cleaner energy systems.

Market Valuation and Growth Trajectory

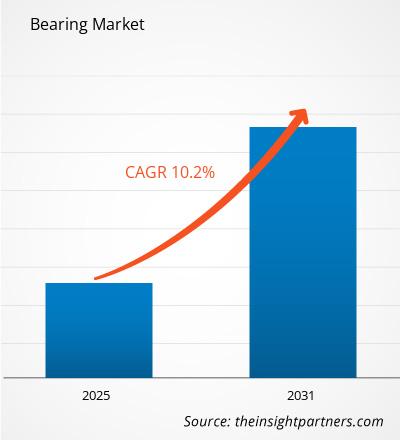

The Bearing Market size is projected to reach US$ 210.864 billion by 2031 from US$ 127.912 billion in 2024. The market is expected to register a CAGR of 7.51% during 2025–2031. This robust growth trajectory highlights an escalating demand across diverse sectors, particularly automotive, aerospace, heavy machinery, and robotics.

As developing economies expand their manufacturing infrastructure and developed nations modernize their industrial plants with IoT-enabled technologies, the reliance on high-quality, long-lasting bearings has never been higher. The steady Compound Annual Growth Rate (CAGR) reflects a market that is not just expanding in volume, but also shifting toward higher-value, specialized bearing solutions.

Primary Growth Drivers

Several macro-economic and technological trends are fueling this market expansion:

The Electric Vehicle (EV) Revolution: The automotive industry is undergoing its most significant shift in a century. EVs require specialized bearings that can operate smoothly at much higher rotational speeds (RPMs) while minimizing noise, vibration, and harshness (NVH). Furthermore, these bearings must offer low friction to maximize battery range and prevent electrical arcing from damaging internal components.

Industrial Automation and Robotics: The rise of Industry 4.0 has led to widespread deployment of automated manufacturing lines and robotic arms. These systems demand high-precision miniature and slewing bearings capable of precise, repetitive movements over millions of cycles without failure.

Renewable Energy Infrastructure: The global push for green energy has led to massive investments in wind power. Wind turbines rely heavily on large-diameter main shaft and gearbox bearings that can withstand extreme, unpredictable aerodynamic loads and harsh environmental conditions over a multi-decade lifespan.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPTE100000700

Key Market Players

The global bearing market is highly competitive, characterized by a mix of established legacy manufacturers who continually innovate to maintain their market share. The prominent companies leading the industry include:

SKF (Sweden) – A global leader recognized for its extensive range of rolling bearings, seals, and lubrication systems, heavily focusing on digital monitoring and sustainability.

Schaeffler Group (Germany) – Renowned for its INA and FAG brands, driving innovation in high-precision components for automotive engines, transmissions, and industrial applications.

The Timken Company (USA) – A specialist in tapered roller bearings, widely trusted for heavy-duty industrial machinery, rail, and aerospace applications.

NSK Ltd. (Japan) – One of the foremost suppliers of ball bearings and automotive components, known for exceptional reliability and motion control technologies.

NTN Corporation (Japan) – A major global supplier specializing in eco-friendly bearing designs and constant velocity joints for the automotive sector.

NACHI-FUJIKOSHI CORP. (Japan) – A versatile manufacturer integrating bearing production with cutting tools, hydraulics, and industrial robotics.

JTEKT CORPORATION (Japan) – Known for its Koyo bearing brand, providing advanced steering systems and high-performance bearings across global supply chains.

These industry giants are aggressively investing in Research and Development (R&D) to develop "smart bearings" equipped with integrated sensors. These sensors monitor temperature, vibration, and lubrication levels in real time, allowing operators to perform predictive maintenance before a catastrophic failure occurs.

Future Outlook

The future of the bearing market points toward a convergence of material science and digital technology. Over the coming years, expect to see accelerated adoption of ceramic and hybrid bearings which utilize silicon nitride ceramic balls inside steel rings due to their superior heat resistance, lower weight, and electrical insulation properties. Furthermore, sustainability will become a core focus; manufacturers are increasingly utilizing recycled steel and carbon-neutral production processes to meet strict corporate environmental goals. As industries across the globe continue to prioritize energy efficiency, the development of ultra-low-friction bearings will remain paramount, solidifying the bearing industry's role as a vital catalyst for global economic and technological progress.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The aerospace industry relies on structural components that ensure vehicle integrity, passenger comfort, and operational safety. Among these critical elements, aircraft engine mounts play a fundamental role. These specialized components connect the aircraft engine to the fuselage or wing pylons. Beyond providing mechanical support, engine mounts absorb severe engine vibrations, secure heavy propulsion systems, and minimize structural stress transferred to the airframe during flight maneuvers. Driven by a surge in commercial airline fleets, continuous military modernizations, and rapid breakthroughs in lightweight materials, this sector is poised for substantial financial expansion.

Market Size and Significant Projections

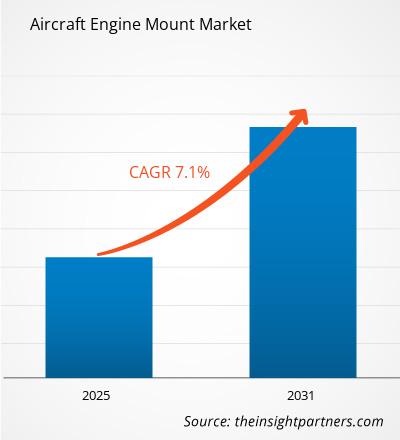

According to a comprehensive industry study, the global aircraft engine mount market is entering a phase of robust, continuous growth. The Aircraft Engine Mount Market size is expected to reach US$ 1,741.57 Million by 2034 from US$ 918.92 Million in 2025. This long-term expansion highlights a stable market trajectory, with the industry estimated to record a CAGR of 7.36% from 2026 to 2034.

This sustained growth is heavily supported by the increasing global demand for single-aisle commercial aircraft, alongside a massive push to replace aging fleets with fuel-efficient, next-generation variants. Because engine mounts must endure extreme thermal conditions and intense kinetic forces, they are subject to regular, stringent maintenance and replacement schedules. This routine maintenance establishes a highly profitable aftermarket segment that complements original equipment manufacturer (OEM) demands.

Market Growth Drivers and Technical Shifts

Modern aviation demands quieter, lighter, and more aerodynamically efficient aircraft. To fulfill these design requirements, engine manufacturers have introduced high-bypass and ultra-high-bypass turbofan engines. While these propulsion systems offer superior fuel economy, they feature larger fan diameters and significantly increased weight. Consequently, aircraft structures must adapt, leading to the development of advanced engine mounts capable of distributing immense thrust loads without altering the aircraft's center of gravity or exceeding strict weight budgets.

Material science acts as another primary catalyst driving market growth. Traditional engine mounts constructed from standard steel alloys are steadily being replaced by high-performance materials. Advanced titanium alloys, nickel-based superalloys, and carbon fiber composite integrations are increasingly favored by modern aerospace designers. These advanced materials provide exceptional strength-to-weight ratios and superior resistance to corrosion and thermal fatigue, directly expanding product lifecycles and lowering long-term maintenance overhead for global commercial operators.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00029696

Competitive Landscape and Key Industry Players

The global aircraft engine mount market is characterized by a mix of established tier-1 aerospace component manufacturers, specialized engineering firms, and comprehensive aviation technology companies. These organizations focus on collaborative design cycles with major airframe and engine OEMs, expanding their domestic production capabilities, and dedicating capital to advanced metallurgy and elastomeric dampening research.

Prominent market participants steering the technical development and distribution of aircraft engine mounts include:

Acorn Welding

Cadence Aerospace

Continental Aerospace Technologies

EPI Inc.

Honda Aircraft Company

Parker Hannifin Corporation

SAM Suzhou

The Wag Aero Group

VAN'S AIRCRAFT, INC.

Strategic partnerships, long-term procurement contracts with defensive bodies, and precision additive manufacturing (3D printing) represent the core methodologies utilized by these key entities to secure market share and meet evolving custom engineering specifications.

Future Outlook

Looking ahead, the aircraft engine mount market will transform in parallel with the foundational evolution of modern aviation design. Over the next decade, the industry will pivot toward supporting advanced aerial mobility, electric vertical takeoff and landing (eVTOL) aircraft, and hybrid-electric propulsion systems. These emerging electric configurations present entirely unique engineering challenges, demanding engine mounts optimized for high-frequency electrical isolation and minimal acoustic profiles rather than traditional high-thrust dampening. Furthermore, the increasing integration of smart sensors into component structures will enable real-time health monitoring and predictive maintenance. By allowing structural flaws to be diagnosed before component failure occurs, these advanced technologies will enhance international flight safety and cement the engine mount sector's role in the future of automated, highly efficient aerospace ecosystems.

Related Reports-

Aircraft Engine Forging Market

Aircraft Engine Compressor Market

Aircraft Engine Fuel Systems Market

Aircraft Engine Component Market

North America Aircraft Engine Forging Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global automotive landscape is undergoing a monumental paradigm shift, transitioning rapidly from traditional internal combustion engines (ICE) to electric and hybrid vehicles. At the heart of this transformation is the lithium-ion battery pack, a component that demands precise environmental conditions to operate safely, efficiently, and durably. Consequently, the reliance on advanced cooling and heating infrastructure within vehicles has intensified, turning battery thermal management into a cornerstone of modern automotive engineering.

The Automotive Battery Thermal Management System Market size is expected to reach US$ 10.53 billion by 2031. The market is anticipated to register a CAGR of 15.2% during 2025-2031. This robust growth trajectory underscores the escalating production of electric vehicles (EVs), breakthroughs in battery chemistry, and stringent regulatory mandates worldwide aimed at curbing vehicular emissions.

Batteries are highly sensitive to temperature fluctuations. Operational environments that are too hot accelerate degradation, reduce driving range, and in extreme scenarios trigger thermal runaway, a catastrophic chain reaction leading to fires. Conversely, extremely cold temperatures severely restrict a battery's ability to accept or deliver a charge, diminishing performance and slowing down fast-charging capabilities.

Automotive battery thermal management systems (BTMS) resolve these issues by utilizing technologies such as liquid cooling, air cooling, phase change materials (PCM), and thermoelectric modules. By maintaining the battery pack within its optimal temperature window (typically between 20°C and 40°C), these systems optimize energy efficiency, ensure passenger safety, and extend the overall lifespan of the vehicle's powertrain.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00006121

Several critical factors are propelling the expansion of the BTMS market. First, the consumer demand for driving range autonomy has pushed automakers to deploy larger battery capacities and higher voltage architectures (such as 800V systems). Higher voltage architectures enable ultra-fast charging, but they also generate massive amounts of heat during the charging cycle, necessitating highly sophisticated liquid-cooling circuits.

Furthermore, governments globally are introducing strict fuel economy standards and offering lucrative incentives for EV adoption. This regulatory tailwind is forcing original equipment manufacturers (OEMs) to invest heavily in next-generation thermal management architectures. Integration is another key trend; modern systems do not just cool the battery in isolation but manage the thermal needs of the electric motor, power electronics, and passenger cabin holistically to conserve every watt of energy.

The global marketplace is characterized by intense competition, featuring a mix of established automotive tier-1 suppliers and specialized technology providers investing aggressively in research and development. Key players shaping the competitive landscape include:

Calsonic Kansei Corporation

Continental AG

Dana Incorporated

Gentherm Incorporated

Hanon Systems

LG Chem Ltd.

MAHLE GmbH

Robert Bosch GmbH

SAMSUNG SDI CO., LTD.

Valeo

These industry leaders are focused on scaling production, forming strategic partnerships with OEMs, and pioneering lightweight, compact thermal components to reduce the overall weight of electric vehicles.

Future Outlook

The future of the Automotive Battery Thermal Management System market points toward a highly integrated and intelligent ecosystem. As solid-state batteries edge closer to commercialization, thermal requirements will evolve, demanding systems capable of managing unique pressure and high-temperature operating thresholds. Additionally, the integration of artificial intelligence and predictive software into vehicle energy management will allow future BTMS to anticipate thermal loads based on driving habits, GPS terrain data, and weather forecasts. This shift from reactive cooling to proactive, intelligent thermal orchestration will significantly enhance EV range and charging speeds, securing BTMS as an indispensable technology in the next generation of autonomous and electrified transportation.

Related Reports-

Electric Vehicle Battery Swapping Market

Battery Production Machine Market

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global aviation ecosystem relies heavily on the efficiency and reliability of its ground operations. Among these, line maintenance stands as the frontline defense against mechanical delays, technical disruptions, and safety compromises. Executed primarily on the tarmac during routine turnarounds or transit periods, line maintenance ensures that aircraft are strictly airworthy before every takeoff. As global passenger traffic rebounds sharply and airline fleets expand across the globe, the strategic importance of this sector has reached unprecedented heights.

Market Valuation and Growth Dynamics

According to the latest comprehensive intelligence by The Insight Partners, the financial trajectory of this industry points toward robust long-term expansion. The Aircraft Line Maintenance Market is projected to reach US$ 39.49 billion by 2034 from US$ 24.68 billion in 2025. This steady climb represents an anticipated Compound Annual Growth Rate (CAGR) of 5.36% during the forecast period from 2026 to 2034.

This sustained growth is driven by several macroeconomic factors. The influx of next-generation aircraft models, the establishment of fresh regional flight corridors, and increasingly stringent global aviation safety regulations are compelling operators to ramp up their routine maintenance schedules. Furthermore, as commercial airlines strive to maximize the operational utilization of their active fleets, minimizing ground time while ensuring flawless mechanical compliance has become a core commercial imperative.

Market Drivers

Line maintenance encompasses a variety of light, pre-flight, and overnight checks that do not require the aircraft to be removed to a dedicated hangar environment. Key services include daily or weekly checks, fluid top-ups, wheel and brake replacements, and minor structural repairs.

One of the prominent trends steering the market is the outsourcing model. Due to the immense capital expenditure required to establish and staff dedicated line stations at every destination airport, many airlines are opting to partner with specialized Third-Party Maintenance, Repair, and Overhaul (MRO) providers. This enables carriers to cut fixed overhead costs, leverage localized expertise, and maintain flexible operational networks across international hubs.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPTE100001325

Competitive Landscape and Key Players

The global landscape is highly competitive, characterized by a mix of specialized independent MRO facilities, joint ventures, and the technical divisions of major commercial airlines. These organizations are continually expanding their line station footprints to secure lucrative long-term servicing contracts with international airlines.

The prominent and influential market participants shaping the industry include:

British Airways

Delta TechOps

FL Technics

Hong Kong Aircraft Engineering Company Limited (HAECO)

Lufthansa Technik AG

SAMCO Aircraft Maintenance B.V.

SIA Engineering Company Ltd.

SR Technics Switzerland AG

Turkish Technic

United Airlines, Inc.

These key players are actively investing in technician training programs, geographic facility expansion, and advanced diagnostic tooling to maintain their market dominance and cater to the evolving needs of modern aircraft fleets.

Future Outlook

Looking ahead, the future of the aircraft line maintenance market will be fundamentally defined by automation, digital transformation, and the integration of predictive maintenance capabilities. The traditional "run-to-failure" or strictly reactive maintenance approaches are rapidly giving way to data-driven ecosystem networks. Modern aircraft equipped with advanced IoT sensors generate massive volumes of real-time telemetry data while in flight. Forward-thinking line maintenance providers are leveraging this data alongside AI-driven diagnostic platforms to predict mechanical faults before the plane even lands. This allows line crews to pre-stage parts, tools, and certified technicians directly at the arrival gate, virtually eliminating unexpected structural delays. Additionally, the adoption of augmented reality (AR) smart glasses for remote tech support and digital logbooks will streamline workflow efficiencies. Over the 2026–2034 forecast horizon, this digital shift will not only optimize operational turn times for airlines but also reshape the baseline capabilities required by MRO providers to remain competitive in a highly dynamic global airspace.

Related Reports-

Military Equipment Maintenance Repair and Overhauling Services Market

Aircraft Engine Forging Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global oilfield auxiliary rental equipment market is undergoing a significant transformation, driven by shifting dynamics in the oil and gas sector, technological advancements, and a growing emphasis on operational efficiency. As exploration and production (E&P) activities venture into more challenging environments, such as deepwater and unconventional shale plays, the demand for specialized support equipment has surged. Navigating this landscape requires robust infrastructure, which is why market players increasingly rely on equipment rental models to manage capital expenditure (CAPEX) while optimizing production capabilities.

Market Size and Growth Trajectory

The global Oilfield Auxiliary Rental Equipment Market size is projected to reach US$ 50.74 Billion by 2034 from US$ 34.03 Billion in 2025. The market is anticipated to register a CAGR of 4.4% during the forecast period 2026–2034.

This steady growth highlights a fundamental shift in how oilfield operators approach asset management. Instead of outright purchasing auxiliary machinery—such as specialized drilling tools, pressure control equipment, power generation units, and waste management systems—companies are turning to rental services. The rental model provides operators with the agility to scale operations up or down based on market volatility and regional project demands, mitigating the financial risks associated with underutilized or depreciating physical assets.

Market Drivers and Dynamics

Several macro-economic and industry-specific factors are fueling the expansion of the oilfield auxiliary rental equipment market. First, the recovery and stabilization of global crude prices have revitalized drilling activities across mature basins and new frontiers alike. However, despite increased budgets, operators remain cautious about capital allocation. By prioritizing operating expenditure (OPEX) through rental equipment over CAPEX, oil and gas companies maintain healthier balance sheets.

Furthermore, stringency in environmental regulations is playing a massive role. Auxiliary equipment related to waste management, spill containment, and emissions control must now meet strict compliance standards. Rental companies specialize in providing the latest, legally compliant technology, saving operators the hassle and cost of constantly upgrading their proprietary fleets. Technological innovation, including the integration of IoT-based monitoring and predictive maintenance in rental fleets, has also increased the reliability of these outsourced assets, reducing costly non-productive time (NPD) on site.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00021336

Key Players in the Global Landscape

The ecosystem of the oilfield auxiliary rental equipment market comprises a mix of leading exploration and production companies, integrated oilfield service giants, and specialized equipment providers. The prominent entities shaping the market include:

BP

CNPC (China National Petroleum Corporation)

Key Energy Services

Occidental Petroleum

Oil States International

Schlumberger (SLB)

Shell

Superior Energy Services

Total (TotalEnergies)

Weatherford

These major players are driving market evolution through strategic mergers and acquisitions, geographic expansions, and heavy investments in digitalizing their rental asset portfolios to offer more value-driven services to end-users.

Future Outlook

The future of the oilfield auxiliary rental equipment market looks promising, characterized by a dual focus on digital transformation and sustainable operations. Moving forward, the industry will likely see widespread adoption of "smart" rental equipment equipped with advanced sensors that feedback real-time data to operators, maximizing efficiency and safety during complex drilling operations. Additionally, as the global energy transition accelerates, rental companies that adapt their fleets to include low-carbon auxiliary equipment, solar-powered generators, and highly efficient eco-friendly machinery will capture a competitive edge. Despite the cyclical nature of the oil and gas sector, the intrinsic cost benefits and operational flexibility offered by auxiliary rentals guarantee that this market will remain an indispensable pillar of global upstream operations through 2034 and beyond.

Related Reports-

Oilfield Equipment Rental Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global industrial landscape is experiencing a significant paradigm shift, with a heightened focus on thermal efficiency, process optimization, and sustainability. At the heart of this transition is the insulated storage vessels market, which plays a critical role in preserving the integrity of temperature-sensitive liquids, gases, and chemicals across diverse sectors. These highly engineered containment systems prevent heat transfer, ensuring that materials remain at precise thermal thresholds during processing, transit, and long-term storage. From food and beverage processing to oil and gas, pharmaceuticals, and chemical manufacturing, the demand for high-performance insulation technologies is escalating rapidly.

Market Valuation and Growth Trajectory

Reflecting this broad-based industrial demand, the market is poised for robust expansion over the next decade. The Insulated Storage Vessels Market size is expected to reach US$ 7.34 Billion by 2034 from US$ 4.90 Billion in 2025. The market is anticipated to register a CAGR of 4.59% during the forecast period 2026–2034.

This steady growth trajectory is primarily propelled by strict environmental and safety regulations mandating energy conservation. Industries are increasingly replacing outdated, uninsulated tanks with modern, double-walled, or vacuum-insulated solutions to minimize product boil-off, prevent emissions, and reduce energy consumption. Additionally, the rapid expansion of the global liquefied natural gas (LNG) network and the emerging hydrogen economy are acting as major catalysts, fueling the adoption of specialized cryogenic insulated vessels.

Key Drivers and Market Dynamics

Several macroeconomic and technological factors are shaping the expansion of the insulated storage vessels market. In the food and beverage industry, maintaining strict temperature controls is vital for hygiene, product quality, and extending shelf life. Breweries, dairy processing plants, and juice manufacturers heavily rely on stainless steel insulated vessels to manage fermentation and storage temperatures.

In the chemical and pharmaceutical industries, precise thermal stabilization prevents volatile substances from degrading or posing safety hazards. Furthermore, urbanization and industrialization in developing regions particularly across Asia-Pacific and Latin America are leading to substantial investments in wastewater treatment facilities and chemical processing plants. These infrastructure developments naturally drive the bulk procurement of durable, corrosion-resistant, and thermally insulated containment units.

Innovation in insulation materials is another pivotal factor. Manufacturers are shifting from traditional fiberglass or polyurethane foam toward advanced materials like vacuum insulation panels (VIPs) and multi-layer insulation (MLI). These innovations offer superior thermal resistance with thinner profiles, maximizing the internal storage capacity of the vessels while drastically reducing structural weight.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00021330

Prominent Industry Participants

The global marketplace features a mix of established multinational corporations and specialized engineering firms focusing on localized custom solutions. The key players steering innovation and market penetration include:

Comap S.r.l. – Renowned for high-quality industrial processing and thermal containment systems.

Della Toffola SpA – A major global provider of advanced storage and processing vessels, particularly for the beverage and winemaking industries.

Fletcher European – Specializes in heavy-duty, hygienic material handling and insulated storage containers for food logistics.

Indian Oil Corporation Ltd. – A dominant energy enterprise driving large-scale infrastructure deployment for petroleum and chemical insulated storage.

Kingspan Group – A global leader in high-performance insulation and building envelope solutions, contributing significantly to thermal containment technology.

Müller Group – Widely recognized for precision-crafted stainless steel handling and storage systems tailored for pharmaceuticals and fine chemicals.

Pneumatech MGS – Specialized in gas generation and industrial air equipment, providing robust pressurized containment systems.

Toro Equipment – A leading manufacturer of wastewater treatment equipment, offering specialized tanks for wastewater and sludge storage.

Wärtsilä – A global leader in innovative technologies and lifecycle solutions for the marine and energy markets, heavily involved in LNG storage and cryogenic vessel engineering.

Werner Sölken – Renowned for engineered tank systems and industrial components focusing on fluid storage and environmental safety.

Future Outlook

The future of the insulated storage vessels market remains highly optimistic, deeply intertwined with the global transition toward a low-carbon economy. As nations accelerate their investments in clean energy, the demand for highly sophisticated cryogenic insulated vessels will skyrocket to support the storage and distribution of liquid hydrogen and ammonia. Furthermore, the integration of IoT-enabled smart sensors into storage vessels will redefine inventory and thermal management. These digital solutions will allow plant operators to monitor real-time temperature fluctuations, structural integrity, and pressure levels remotely, ensuring maximum safety and operational efficiency. Moving forward, continuous breakthroughs in sustainable insulation materials and automated manufacturing techniques will unlock new growth horizons, solidifying insulated storage vessels as indispensable assets in the modern industrial infrastructure.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The automotive industry is undergoing a profound transformation driven by rapid technological innovations, stricter safety regulations, and shifting consumer preferences. At the forefront of this evolution is the automotive lighting sector, particularly rear lighting systems. Beyond their foundational role in ensuring vehicle safety and visibility, rear lights have morphed into vital design elements that define a vehicle’s aesthetic identity and enhance communication with other road users.

According to a comprehensive study by The Insight Partners, the Automotive Rear Lights Market size is expected to reach US$ 28.35 Billion by 2034 from US$ 14.69 Billion in 2025. The market is anticipated to register a CAGR of 7.58% during the forecast period 2026–2034. This robust growth reflects the increasing integration of advanced lighting technologies and the global surge in automobile production.

Driving Factors and Technological Evolution

The steady growth of the automotive rear lights market is fueled by multiple compounding factors. Foremost among these is the global escalation of stringent safety regulations. Governments and international automotive safety bodies are continuously mandating advanced lighting features to reduce rear-end collisions and improve night-time visibility. Features such as dynamic turn signals, adaptive rear lighting systems, and emergency stop signals are shifting from premium luxuries to standard requirements.

Simultaneously, the technology powering rear lights has transitioned significantly. Traditional halogen bulbs are rapidly being replaced by Light Emitting Diodes (LEDs) and Organic Light Emitting Diodes (OLEDs). LEDs offer superior energy efficiency, longer lifespans, faster response times, and exceptional design flexibility. This flexibility allows automakers to craft signature lighting designs such as continuous light strips across the tailgate which serve as a major selling point in modern passenger vehicles, especially electric vehicles (EVs).

Furthermore, the rise of electric and autonomous vehicles is fundamentally changing rear light architectures. Because EVs prioritize energy efficiency to maximize driving range, the low power consumption of LED and OLED systems makes them the industry standard.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00014496

Competitive Landscape and Key Players

The global automotive rear lights market is highly competitive, characterized by the presence of established tier-1 suppliers and innovative technology providers. These companies focus on continuous research and development to introduce lightweight, energy-efficient, and intelligent lighting solutions. Key players operating in the global market include:

HELLA GmbH and Co. KGaA

Koito Manufacturing Co., Ltd

Koninklijke Philips N.V.

Minda Industries Ltd.

OSRAM GmbH

Peterson Manufacturing Co.

Phoenix Lamps Ltd. (Suprajit Group)

Robert Bosch GmbH

STANLEY ELECTRIC CO., LTD.

Valeo

These industry leaders are actively engaging in strategic partnerships, mergers, acquisitions, and product launches to strengthen their market footprint and cater to the changing demands of global original equipment manufacturers (OEMs).

Future Outlook

The future of the automotive rear lights market points toward unprecedented levels of intelligence and digitalization. Looking ahead, rear lighting will transcend its traditional role of passive illumination to become an interactive communication interface. The integration of digital OLEDs and matrix LED technologies will enable rear lights to display customizable graphics, text symbols, and animations. This capability will be crucial for communicating intent or hazard warnings to pedestrians and autonomous vehicles sharing the road. Moreover, as the automotive ecosystem moves toward software-defined vehicles, rear lighting systems will be seamlessly tied into advanced driver assistance systems (ADAS) and vehicle-to-everything (V2X) communication networks. Consequently, the market is poised to experience sustained, high-value growth, transitioning from a commoditized safety component into a sophisticated, software-controlled tech hub.

Related Reports-

Automotive Rear End Module Market

Electric Light Commercial Vehicle Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The industrial manufacturing landscape is experiencing a massive paradigm shift, heavily driven by the principles of Industry 4.0, smart automation, and precise quality control. At the heart of this manufacturing evolution is the digital servo press an advanced technology combining the brute strength of traditional pressing mechanisms with the extreme accuracy and programmability of digital servo motors. A comprehensive analysis by The Insight Partners highlights how the global demand for energy-efficient, customizable, and data-driven assembly solutions is propelling this industry forward, drastically changing production baselines across multiple industrial domains.

Projections and Market Size

The fiscal valuation of this market outlines a trajectory of highly resilient growth over the next decade. According to the data analysis from The Insight Partners:

The Digital Servo Press Market size is expected to reach US$ 359.45 Million by 2034 from US$ 240.89 Million in 2025. The market is estimated to record a CAGR of 4.55% from 2026 to 2034.

This steady compound annual growth rate indicates that industries are consistently phasing out legacy equipment in favor of precision-engineered, digitalized alternatives. The automotive, electronics, aerospace, and medical device manufacturing sectors are expected to be the prominent volume consumers fueling this long-term demand.

Dynamics and Driving Forces of the Market

Traditional mechanical and hydraulic press technologies have historically served industries well; however, they are increasingly falling short under modern standards. Traditional lines suffer from higher energy footprints, lower situational flexibility, and an inability to track granular, stroke-by-stroke process data.

In contrast, digital servo presses operate utilizing clean electric power driven by servo motors. This grants manufacturers unparalleled control over driving parameters, such as stroke speed, depth, and applied force profiles. Because these parameters are fully programmable, manufacturing facilities can drastically cut down on tooling setup times and debugging costs during product changeover scenarios. Additionally, integrated software solutions facilitate real-time monitoring and data collection. By capturing force-versus-distance metrics, companies can identify structural defects instantly during production rather than relying on delayed post-production quality assurance testing.

The global push toward modern sustainability also serves as a strong market catalyst. Digital servo presses consume energy primarily during the active pressing stroke, whereas hydraulic variants require constant energy consumption to maintain oil pressure. By cutting down electricity consumption and eliminating hazardous hydraulic fluids, digital servo presses represent a cleaner, safer choice for eco-conscious assembly lines.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00021322

Prominent Industry Key Players

The expansion of the digital servo press market and its associated ecosystem relies heavily on pioneering automation, instrumentation, and technology enterprises. The following key players are driving technical standards, hardware reliability, and software interoperability within the broader industrial market framework:

ABB Ltd

Badger Meter, Inc

Emerson Electric Co

Endress+Hauser AG

General Electric Co

Honeywell International Inc

Krohne Messtechnik GmbH

McCrometer, Inc

Omega Engineering Inc

Siemens AG

These enterprises continue to innovate by providing advanced programmable logic controllers (PLCs), high-performance digital sensors, telemetry options, and integrated control architectures that allow servo systems to communicate seamlessly across factory networks.

Sectoral Applications Across Industries

The growth of the digital servo press market is deeply tied to the evolution of the automotive sector, particularly the rapid scaling of Electric Vehicle (EV) production. EV manufacturing demands exact repeatability and tight tolerances when stamping battery packs, assembling delicate powertrain components, and pressing bearings.

Similarly, the consumer electronics sector relies on the micron-level precision of digital presses to bend internal shields, crimp wire connections, and assemble small micro-components without damaging fragile circuit boards. The medical device industry additionally depends on these systems to maintain cleanroom integrity free from hydraulic oil mist while ensuring that serialized devices conform identically to rigid health and safety metrics.

Future Outlook

Looking ahead, the future of the digital servo press market lies in deep AI-driven predictive analytics and the expanding utilization of industrial Digital Twins. Future iterations of servo systems will move beyond simple data logging; instead, they will utilize edge computing to self-adjust driving parameters mid-stroke based on localized material resistance variations. As wireless 5G communication and Internet of Things (IoT) technologies cement their place on factory floors, digital servo presses will function as fully connected node devices, feeding real-time digital threads across product lifecycles. This continued innovation ensures that digital servo presses will remain an indispensable cornerstone of resilient, highly sustainable, and intelligent manufacturing for decades to come.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global aviation landscape is undergoing a profound structural shift. While aeronautical revenues derived directly from aircraft landings, passenger fees, and security charges historically formed the financial backbone of airports, the modern economic model heavily relies on commercial, non-aeronautical streams. As airports transform from traditional transit hubs into multi-functional commercial ecosystems and smart cities, optimizing non-aeronautical revenue has become a critical strategic imperative for operators worldwide.

According to a comprehensive market analysis by The Insight Partners, the Airport Non-Aeronautical Revenue Market is expected to register a CAGR of 5.41% from 2026 to 2034, with the market size expanding from US$ 99.05 Billion in 2025 to US$ 159.15 Billion by 2034. This steady growth reflects a broader industry push toward financial diversification, shielding airport operators from the cyclical volatility of airline ticket sales and fluctuating flight frequencies.

Market Dynamics and Growth Catalysts

The impressive growth trajectory of the non-aeronautical sector is fueled by several converging trends. First and foremost is the global resurgence and evolution of passenger traffic. Modern travelers frequently arrive at airports hours before their flights due to streamlined digital check-ins and baggage drops, resulting in extended "dwell time." Airport operators are successfully capitalising on this idle time by curating highly engaging environments that blend high-end retail, experiential dining, and local cultural exhibits.

Furthermore, digital transformation acts as a massive multiplier for this market. The deployment of advanced data analytics, artificial intelligence, and location-based mobile applications allows airports to send personalized retail offers, restaurant pre-ordering options, and duty-free discounts directly to passengers' smartphones. By integrating digital marketplaces into the physical layout, airports are expanding their retail reach far beyond the traditional storefront.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00021216

Strategic Revenue Streams

The non-aeronautical sector comprises a diverse portfolio of revenue-generating activities that cater to different passenger demographics and operational needs:

Duty-Free and Luxury Retail: Often the largest contributor, featuring international luxury brands, cosmetics, electronics, and regionally curated souvenirs.

Food and Beverages (F&B): Shifting away from standard fast food toward premium dining experiences, microbreweries, and collaborations with celebrity chefs to create a destination-like appeal.

Car Parking and Ground Transportation: Smart parking solutions, premium valet services, and integrated ride-sharing hubs remain highly lucrative revenue pillars.

Real Estate and Property Management: Leasing airport land for premium lounges, hotels, logistics facilities, and commercial office spaces.

Key Market Players

The global market is characterized by prominent airport authorities and privatized operators managing world-class facilities and driving innovative commercial strategies. Key players operating in the global Airport Non-Aeronautical Revenue market include:

Aena

Aeroports de Paris

Airport Authority Hong Kong

Airports of Thailand Public Co., Ltd.

Fraport AG Frankfurt Airport Services Worldwide

Heathrow SP Ltd.

Japan Airport Terminal Co., Ltd.

Kobenhavns Lufthavne A/S

Korea Airports Corporation

VINCI

These entities are continuously investing in terminal expansions, infrastructure upgrades, and smart retail technologies to elevate the passenger experience and maximize commercial yields per square meter.

Future Outlook

Looking ahead, the future of the airport non-aeronautical revenue market lies at the intersection of hyper-personalization and sustainable commercial practices. As consumer preferences tilt toward eco-conscious travel, green retail spaces, locally sourced dining options, and carbon-neutral airport lounges will become standard offerings rather than premium novelties. Additionally, the integration of advanced biometric systems and autonomous retail stores will drastically reduce security and transaction frictions, leaving passengers with more stress-free dwell time to explore commercial zones. Over the next decade, airports will fully transition from mere infrastructure nodes into standalone lifestyle and entertainment destinations, solidifying their non-aeronautical streams as the primary engines of long-term economic resilience.

Related Reports-

High Altitude Aeronautical Platform Station (HAAPS) Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The aviation industry is witnessing a massive resurgence, fueled by an unprecedented rise in global passenger traffic and the continuous expansion of commercial and military aircraft fleets. At the heart of this complex ecosystem lies the aircraft engine the most critical, high-value component of any flying vessel. Ensuring the optimal performance, safety, and fuel efficiency of these propulsion systems requires highly specialized care, creating a robust demand for the global Aircraft Engine MRO (Maintenance, Repair, and Overhaul) sector.

According to an extensive market study, the Aircraft Engine MRO Market is expected to reach US$ 26.61 billion in 2025 and is expected to reach US$ 41.21 billion by 2034; it is estimated to record a CAGR of 5.0% during 2026–2034. This steady compound annual growth rate reflects a broader industry transition toward more advanced, digitalized, and sustainable maintenance ecosystems.

Engine maintenance is historically the largest expense category within the overarching aircraft MRO budget, often accounting for nearly 40% to 45% of total operator maintenance costs.

Several pivotal factors are driving the substantial growth projected through 2034:

Aging Fleets and Extended Engine Lifespans: While airlines are actively acquiring newer aircraft models, a substantial portion of the global fleet consists of mid-life or legacy aircraft. As these engines accumulate flight hours and cycles, they require more frequent and extensive overhauls such as performance restoration shop visits and life-limited parts (LLP) replacements to remain airworthy.

Technological Advancements in Modern Engines: Next-generation turbofans, such as the CFM LEAP and Pratt & Whitney GTF series, are designed with highly complex geometries, advanced composite materials, and specialized thermal barrier coatings. While these innovations deliver exceptional fuel efficiency, their maintenance demands highly specialized diagnostic tooling, cleaner workspaces, and pristine engineering precision, driving up the average value per shop visit.

Rigorous Aviation Safety Regulations: Regulatory authorities worldwide, including the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), strictly mandate routine inspections and preventative overhauls. These non-negotiable safety standards ensure a constant, predictable baseline of demand for certified MRO facilities.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00025489

The Competitive Landscape: Key Market Players

The global aircraft engine MRO ecosystem relies on a mix of Original Equipment Manufacturers (OEMs), independent service providers, and airline-affiliated MRO shops. The leading organizations spearheading technological innovation and market share include:

Delta Air Lines Inc: Operating through its prominent Delta TechOps division, this airline-backed giant offers comprehensive MRO solutions globally.

GE Aerospace: A premier engine OEM that dominates the aftermarket services space, providing extensive engine care and specialized overhaul networks.

CFM International: A highly successful joint venture between GE Aerospace and Safran, supporting the world’s most widely used narrowbody engine lines.

Lufthansa Technik: A world-renowned independent provider delivering elite-level component maintenance and engine overhaul support.

Safran SA: A global aerospace powerhouse supplying critical propulsion technologies and reliable maintenance solutions.

SIA Engineering Company: Based in Singapore, this vital Asian hub provider services massive international fleets across the Asia-Pacific region.

Sigma Aerospace: A highly agile independent operator specializing in regional and turboprop engine maintenance.

Rolls-Royce Holdings Plc: Renowned for their "TotalCare" service packages, maintaining large-cabin widebody commercial and corporate jet engines.

RTX CORPORATION: Powering global aviation via Pratt & Whitney, delivering advanced technological MRO services across military and commercial sectors.

MTU Aero Engines AG: Germany’s leading engine manufacturer and a globally recognized force in independent engine maintenance.

Future Outlook

Looking ahead toward 2034, the future of the Aircraft Engine MRO market will be deeply intertwined with digital transformation and environmental sustainability. Predictive maintenance powered by Artificial Intelligence (AI) and big data analytics is fundamentally shifting the industry from a reactive model to a proactive one. Real-time engine health monitoring allows operators to detect component degradation before a failure occurs, optimizing shop visit schedules and drastically reducing unplanned aircraft-on-ground (AOG) events. Furthermore, the rising integration of Sustainable Aviation Fuels (SAF) and the early-stage engineering of hybrid-electric engines will require MRO providers to adapt their testing cells, clean rooms, and technician skill sets. Companies that actively invest in advanced automated tooling, drone-assisted borescope inspections, and green overhaul practices will find themselves uniquely positioned to capture the lions share of this projected US$ 41.21 billion market.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876