The global defense, commercial, and consumer technology landscapes are witnessing a massive paradigm shift, driven by the rapid miniaturization of unmanned aerial vehicles (UAVs). At the forefront of this evolution is the nano drones market. These ultra-compact, lightweight aerial systems often small enough to fit in the palm of a hand are rapidly transitioning from novelty gadgets to indispensable tools for tactical reconnaissance, industrial inspection, and precision monitoring.

According to market research, the Nano Drones Market size is expected to reach US$ 10.17 Billion by 2034 from US$ 3.31 Billion in 2025. This rapid expansion highlights a significant surge in demand across multiple sectors, with the market estimated to record a Compound Annual Growth Rate (CAGR) of 15.06% from 2026 to 2034.

Several key factors are driving this remarkable 15.06% compound annual growth. Primarily, the defense and military sectors are heavily investing in nano UAVs to equip individual soldiers with immediate, organic surveillance capabilities. Unlike larger drone systems that require dedicated transport and launch infrastructure, nano drones can be deployed in seconds by a single operator to scout around corners, peer over walls, or inspect hostile environments without exposing personnel to danger.

Simultaneously, the commercial sector is unlocking new use cases for these miniature devices. In agriculture, nano drones are being deployed to monitor crop health in tight or heavily forested areas. In construction and infrastructure, they offer a safe and highly efficient means to inspect confined spaces, such as pipeline interiors, storage tanks, and structural beams, where traditional drones are too large to safely navigate. Furthermore, continuous advancements in battery density, micro-sensor technology, and lightweight materials are allowing these tiny aircraft to fly longer, capture higher-resolution imagery, and operate reliably even in challenging weather conditions.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022352

The nano drones market features a mix of established defense giants, aerospace pioneers, and specialized tech startups. These companies are actively investing in research and development to enhance payload capabilities, improve autonomous flight controls, and secure long-term government and commercial contracts.

Key players shaping the future of the nano drones industry include:

AeroVironment, Inc. – A dominant force in tactical UAS, known for pioneering micro and nano-aerial solutions for defense and security forces.

Drona Aviation Pvt Ltd – An innovative developer focusing on educational and compact drone technology, making micro-UAVs more accessible.

Elbit Systems Ltd. – An international defense electronics provider integrating advanced intelligence and autonomous capabilities into miniature flight systems.

Hubsan Technology Company Ltd – A prominent name in the consumer and commercial drone space, recognized for producing highly agile, compact aerial platforms.

Lockheed Martin Corporation – An aerospace and defense titan delivering state-of-the-art, ruggedized nano UAVs built for complex military operations.

MICRODRONES – A leader in commercial mapping and aerial surveying, adapting heavy-duty sensor technology into highly precise, smaller form factors.

Parrot Drone SAS – A well-known European drone manufacturer focusing heavily on secure, lightweight, and high-resolution aerial imaging solutions.

Saab AB – A defense and security company providing cutting-edge aviation and tactical support technology, including micro-surveillance assets.

Thales Group – A global technology leader in aerospace and defense, specializing in secure communication systems and autonomous flight integration for small UAVs.

TRNDlabs – A tech brand focused on developing stylish, ultra-compact, and highly maneuverable consumer and hobbyist mini-drones.

Future Outlook

Looking ahead, the future of the nano drones market will be fundamentally defined by the integration of artificial intelligence (AI) and edge computing. As microchips become more powerful and energy-efficient, future nano drones will no longer rely solely on constant pilot intervention; instead, they will possess the onboard intelligence to navigate complex GPS-denied environments, avoid obstacles autonomously, and recognize specific objects or targets in real-time. We can also expect the rise of "swarm intelligence," where fleets of nano drones communicate and coordinate with one another to map out large disaster zones or secure vast perimeters with unmatched speed. Supported by a robust projected valuation of US$ 10.17 billion by 2034, the nano drone industry is poised to evolve from a specialized niche into a pervasive, everyday technological standard across the global commercial and military domains.

Related Reports-

Autonomous BVLOS Drones Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The landscape of modern warfare and military aviation is undergoing a massive transformation. As surface-to-air and air-to-air missiles become increasingly sophisticated, protecting military aircraft from heat-seeking threats has become a paramount priority for defense forces worldwide. Infrared (IR) guided missiles pose a severe threat because they track the thermal signatures emitted by aircraft engines. To mitigate this risk, defense manufacturers have developed advanced Airborne IR Countermeasures, a critical segment of electronic warfare designed to blind, deflect, or deceive incoming heat-seeking threats. Driven by escalating geopolitical tensions and heavy investments in next-generation defense systems, this market is poised for substantial expansion over the next decade.

Market Dynamics and Projections

The Airborne IR Countermeasures Market is expected to register a CAGR of 5.99% from 2026 to 2034, with the market size expanding from US$ 4.69 Billion in 2025 to US$ 7.92 Billion by 2034.

Several prominent factors are fueling this steady compound annual growth rate (CAGR). Primarily, the rise of asymmetric warfare and regional conflicts has heightened the threat of Man-Portable Air Defense Systems (MANPADS) in hands of non-state actors and insurgent groups. These portable, shoulder-fired missiles are cost-effective but highly lethal to low-flying aircraft, helicopters, and transport planes.

To counter this, modern military strategies demand the integration of automated countermeasure systems across both legacy fleets and newly manufactured aircraft. Additionally, procurement cycles in major defense spending nations such as the United States, China, India, and various NATO members increasingly focus on upgrading electronic warfare (EW) suites, directly injecting capital into the development of sophisticated infrared countermeasure technologies.

Technological Advancements Shaping the Market

Traditionally, aircraft relied heavily on passive countermeasures, such as flares, to distract incoming heat-seeking missiles by creating a secondary, more intense thermal signature. While flares remain a vital, cost-effective layer of defense, modern multi-spectral and imaging infrared (IIR) seekers can often differentiate between a burning flare and an aircraft engine.

This has shifted the industry's focus toward active countermeasures, most notably Directed Infrared Countermeasures (DIRCM) systems. DIRCM technology tracks an incoming missile using missile warning sensors and fires a low-power, modulated laser beam directly into the missile's seeker head. This laser blinds the missile's guidance system, causing it to veer harmlessly off course. The shift toward laser-based systems, which offer unlimited "ammunition" compared to finite flare dispensers, represents the high-tech vanguard of the airborne IR countermeasures market.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022341

Key Industry Players

The competitive landscape of the Airborne IR Countermeasures market is defined by a blend of aerospace giants and specialized defense electronic manufacturers. These entities heavily invest in research and development to deliver lighter, more efficient, and multi-band laser systems capable of protecting a wide array of aerial platforms.

The key players driving innovation and holding significant market share include:

BAE Systems

Elbit Systems Ltd.

HENSOLDT AG

Indra

Leonardo S.p.A.

Northrop Grumman Corporation

Saab AB

Safran

Raytheon Technologies

Thales Group

These companies frequently collaborate with international defense departments, securing multi-year procurement and maintenance contracts that guarantee sustained revenue streams while continuously advancing sovereign electronic warfare capabilities.

Future Outlook

Looking ahead, the future of the Airborne IR Countermeasures market lies in the miniaturization of components and the integration of artificial intelligence (AI). Historically, DIRCM systems were bulky and heavy, limiting their installation primarily to large transport aircraft and heavy-lift helicopters. Moving forward, the industry is successfully scaling down these systems to fit smaller platforms, including fast jets, tactical unmanned aerial vehicles (UAVs), and commercial airliners operating in high-risk zones. Furthermore, the incorporation of AI and machine learning algorithms will allow missile warning systems to detect, classify, and neutralize incoming threats at unprecedented speeds, completely automating the defense cycle. As aerial threat environments grow more hostile, the evolution toward smarter, lighter, and universally compatible laser countermeasure systems will remain the cornerstone of military pilot and aircraft survival.

Related Reports-

Airborne Weapons Carriage and Release Systems Market

Airborne Persistent Surveillance System Market

Airborne Weapon Delivery Systems Market

Airborne ISR as a Service Market

Airborne Collision Avoidance System Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global pallet forks market is experiencing a significant growth trajectory, driven by the expansion of the logistics, warehousing, construction, and agricultural sectors. Pallet forks essential attachments used with forklifts, skid steers, telehandlers, and loaders are crucial for the efficient lifting, moving, and stacking of palletized goods. As industries worldwide prioritize operational efficiency, safety, and automation, the demand for high-quality, durable, and versatile pallet forks continues to climb.

The Pallet Forks Market size is expected to reach US$ 3.1 Billion by 2034 from US$ 2.04 Billion in 2025. The market is estimated to record a CAGR of 5.37% from 2026 to 2034. This steady expansion highlights the indispensable nature of material handling equipment in modern industrial supply chains.

Market Dynamics and Growth Drivers

A primary catalyst for the pallet forks market is the rapid expansion of the e-commerce sector and global logistics networks. Modern fulfillment centers and warehouses require rapid throughput, forcing operators to invest in reliable attachments that minimize downtime. Pallet forks are engineered to handle varying load capacities, and the shift toward heavy-duty, high-tensile steel designs ensures they can withstand the rigorous demands of 24/7 operations.

In addition to logistics, the booming construction and infrastructure sectors globally are fueling market growth. On construction sites, pallet forks attached to telehandlers or skid steers are frequently used to transport heavy building materials like bricks, cement blocks, and timber. Furthermore, the agricultural sector heavily relies on these attachments for moving feed, hay bales, and bulk produce crates, reinforcing the market’s diversified revenue streams across multiple industries.

Technological advancements are also reshaping the manufacturing of pallet forks. Leading vendors are focusing on introducing specialized forks, such as hydraulic reach forks, weighing forks, and anti-slip coated forks. These innovations not only improve workplace safety by preventing load slippage but also maximize productivity by allowing operators to adjust fork spacing or length directly from the operator's cabin.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022041

Key Market Players

The global market features a blend of established heavy machinery manufacturers and specialized attachment providers. These companies focus on product innovation, strategic partnerships, and geographic expansion to strengthen their market presence. Key players operating in the global pallet forks market include:

Avant

Certex

Caterpillar Inc

EDGE

Gehl

Heiden

KINSHOFER GmbH

Koyker

Meijer Handling Solutions

Probst Handling Equipment

These manufacturers are increasingly incorporating smart technologies and advanced metallurgy to offer lightweight yet ultra-strong fork options that optimize the lifting capacity of the host vehicles.

Regional Insights

Geographically, North America and Europe hold substantial shares of the market, owing to highly automated warehousing infrastructures, stringent workplace safety regulations, and widespread adoption of advanced construction machinery. Meanwhile, the Asia-Pacific region is projected to register the fastest growth rate during the forecast period. Rapid urbanization, massive investments in infrastructure projects in countries like India and China, and the expansion of domestic manufacturing hubs are accelerating the deployment of material handling equipment across the region.

Future Outlook

The future of the pallet forks market looks highly promising as industries transition toward greener and smarter operations. The ongoing electrification of forklifts and material handling fleets will require manufacturers to design optimized, lightweight attachments that reduce energy consumption without compromising lifting capacity. Additionally, as automated guided vehicles (AGVs) and autonomous mobile robots (AMRs) become standard in smart warehouses, the integration of intelligent, sensor-equipped pallet forks capable of digital load sensing and automated alignment will emerge as a key trend. Over the next decade, continuous industrial automation and the globalization of supply chains ensure that the pallet forks market will remain a vital and growing segment of the global industrial equipment landscape.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global industrial landscape relies heavily on the integrity of structural connections and heavy machinery. As infrastructure expands and industrial operations scale up, the need for precise, high-capacity fastening tools has become more critical than ever. Central to these operations is the hydraulic torque wrench, a specialized tool engineered to apply precise torque to large bolted joints. According to a comprehensive market study by The Insight Partners, the global hydraulic torque wrench market is on a robust growth trajectory, driven by increasing automation, stringent safety regulations, and expanding heavy industries worldwide.

The industrial sector’s shift toward optimized efficiency and advanced mechanical tools is reflected in the market's financial projections. The global Hydraulic Torque Wrench Market size is projected to reach US$ 838.11 Million by 2034 from US$ 503.44 Million in 2025. This steady expansion represents a calculated compound annual growth rate (CAGR) of 5.7% during the forecast period from 2026 to 2034.

This growth is primarily fueled by the accelerating demands of sectors such as oil and gas, power generation (including wind, thermal, and nuclear energy), manufacturing, and mining. In these environments, standard manual tightening tools are inadequate for the large-diameter bolts used in pipeline construction, pressure vessels, and wind turbine towers. The precision offered by hydraulic models minimizes the risk of joint failure, which is crucial for operational safety and preventing costly downtime.

Several key factors are propelling the expansion of the hydraulic torque wrench market. First, the global boom in renewable energy particularly wind energy requires the assembly and maintenance of massive structures that depend on precise tensioning. Hydraulic torque wrenches provide the repeatability and high-powered output necessary to secure wind turbine tower bolts securely.

Second, industrial safety regulations have tightened significantly. Regulatory bodies now enforce strict guidelines regarding joint integrity to prevent catastrophic leaks or structural collapses. Because hydraulic wrenches allow operators to pre-set torque limits with extreme precision, they ensure compliance with these rigid safety mandates. Furthermore, ergonomics play a vital role. These tools reduce human error and minimize the physical strain placed on operators compared to traditional manual heavy impact tools, driving widespread adoption across modern workshops and field construction sites.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022033

The hydraulic torque wrench market features a competitive landscape populated by several major players and specialized engineering firms. These manufacturers continually innovate to develop lighter, more compact, and digitally integrated tools that provide real-time torque data logging. Some of the prominent key players operating in this marketplace include:

ENERPAC – A global leader in high-pressure hydraulic tools, known for robust engineering and heavy-duty industrial solutions.

HTL Group Ltd. – A specialist in controlled bolting and joint integrity solutions, heavily serving the oil and gas sector.

Hydratight Limited – Renowned for providing world-class joint integrity services and specialized industrial bolting equipment.

HYTORC – A pioneer in the industrial bolting industry, famous for introducing innovative, calibration-free, and spark-free hydraulic systems.

ITH GmbH and Co. KG – A leading system provider for fastening technology, offering high-capacity bolting tools and tensioners.

Maschinenfabrik Wagner GmbH and Co. KG – Creators of Plarad bolting systems, focusing on precision, safety, and torque accuracy.

NORWOLF TOOLS – An innovator in unique mechanical and hydraulic bolting tools designed for confined spaces.

Powermaster Engineers Pvt. Ltd. – A major manufacturer and exporter of heavy-duty industrial bolting and maintenance equipment.

TorcUP Inc. – Celebrated for its heavy-duty industrial torque wrenches featuring sleek, highly durable aluminum-titanium alloy designs.

Torq/Lite – A dedicated manufacturer specializing exclusively in the design and production of advanced hydraulic bolting tools.

Future Outlook

Looking ahead, the future of the hydraulic torque wrench market is deeply intertwined with the "Industry 4.0" revolution. The next generation of hydraulic wrenches is shifting toward intelligent systems equipped with Bluetooth connectivity, digital displays, and IoT capabilities. These smart tools allow field technicians to log and store torque data automatically, providing a digital audit trail for critical joint assemblies. Furthermore, the market will likely see a surge in the development of lightweight, ultra-compact profile tools designed to access highly restricted geometries in modern machinery. As infrastructure projects accelerate across emerging economies in Asia-Pacific and Latin America, and the global transition to clean energy intensifies, the reliance on high-performance hydraulic torque wrenches will expand, ensuring steady market progression well into the next decade.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

Driven by a strong emphasis on fuel diversification and long-haul fleet modernization, the North American hybrid train market is experiencing substantial growth momentum. Because a vast portion of the continent's extensive freight rail network relies heavily on conventional traction over non-electrified routes, full electrification is often financially and structurally impractical. As a result, major rail operators in the United States and Canada are actively investing in electro-diesel and battery-hybrid locomotives to bridge the gap. This shift is highly accelerated by stringent environmental mandates from federal bodies, along with dedicated financial incentives aimed at reducing idle fuel consumption and minimizing carbon footprints in dense urban corridors.

The global transportation sector is undergoing a profound paradigm shift as industries and governments align to combat climate change, reduce greenhouse gas emissions, and transition away from traditional fossil fuels. At the forefront of this evolution is the rail industry, where hybrid locomotives are rapidly emerging as a viable solution for sustainable, high-efficiency transport. According to a comprehensive study by The Insight Partners, the global Hybrid Train Market size is expected to reach US$ 41.75 Billion by 2034 from US$ 24.09 Billion in 2025. The market is anticipated to register a CAGR of 6.3% during the forecast period 2026–2034. This steady growth reflects a worldwide commitment to modernizing transit infrastructure, optimizing operational expenditures, and meeting stringent environmental targets.

Key Market Drivers and Dynamics

The continuous expansion of the hybrid train market is primarily propelled by escalating regulatory pressures and evolving economic variables:

Environmental Regulations and Sustainability: Governments across Europe, North America, and Asia-Pacific are enforcing rigid carbon emission standards. Hybrid trains—which combine traditional internal combustion engines with advanced electric propulsion and energy storage systems—drastically cut emissions and fuel consumption, making them incredibly attractive to eco-conscious rail operators.

Fluctuating Fuel Costs: Volatile global diesel prices impose a heavy financial burden on rail networks. Hybrid locomotives offer a dual-source energy fallback, relying on battery power or overhead electricity during low-speed urban transits and utilizing alternative fuels or diesel engines for long-haul routes. This flexibility protects operators from energy price shocks.

Technological Innovations: Rapid breakthroughs in high-energy-density lithium-ion batteries and regenerative braking systems have revolutionized transit efficiency. Energy normally lost during deceleration is recaptured and stored, extending the operational range of trains running exclusively on electric energy.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00004333

Market Segmentation and Infrastructure Opportunities

The hybrid train ecosystem spans various operational structures tailored to modern transit needs. Segmented by operating speeds, the market caters to lines below 100 km/h, 100–200 km/h, and high-speed corridors exceeding 200 km/h. Its applications are split between passenger services—where reducing city noise and air pollution is vital—and freight shipping, which demands high tractive effort balanced with fuel-saving capabilities.

Furthermore, rapid global urbanization is pushing public transit networks to their limits. Rapidly expanding cities require mass transit solutions that do not contribute to local smog. This urban sprawl opens massive commercial avenues for light rail and commuter hybrid trains. Concurrently, governments are funneling heavy investments into upgrading rail infrastructure, presenting rolling stock manufacturers with historic opportunities to establish charging grids, localized maintenance hubs, and modernized rail networks through lucrative public-private partnerships.

Key Industry Players

The competitive landscape features a blend of veteran rolling stock manufacturers, automotive giants, and industrial engineering conglomerates driving technological innovation.

The key players spearheading the market include:

Alstom

Bombardier

Construcciones y Auxiliar de Ferrocarriles (CAF)

Cummins Inc.

GENERAL ELECTRIC (GE)

HYUNDAI ROTEM COMPANY

Kawasaki Heavy Industries, Ltd.

Siemens

Toshiba India Pvt. Ltd.

Toyota Kirloskar Motor

These companies are heavily investing in research and development to scale up diverse propulsion systems, including electro-diesel, battery-powered, liquefied natural gas (LNG), compressed natural gas (CNG), and hydrogen fuel cell technologies.

Future Outlook

The future of the hybrid train market points toward total systems intelligence and cross-industry technical convergence. Over the next decade, the industry will transition beyond basic fuel efficiency to focus heavily on the integration of digital technologies, such as IoT-enabled predictive maintenance, real-time battery degradation tracking, and automated energy management algorithms that dynamically switch propulsion modes based on topography. Furthermore, collaborative innovation will take center stage as traditional rail manufacturers form strategic joint ventures with specialized automotive battery producers and hydrogen infrastructure developers. As alternative fuels like hydrogen and solar integration mature alongside next-generation solid-state batteries, hybrid trains will solidify their position as the structural backbone of green, long-distance intercity transportation and sustainable urban logistics.

Related Reports-

Automatic Train Wash System Market

Autonomous Train Technology Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The North America region commands a dominant position in the global traction control system market, primarily accelerated by early and strict vehicle safety mandates implemented by agencies like the National Highway Traffic Safety Administration (NHTSA). The market across the United States and Canada is heavily driven by a strong consumer preference for large passenger vehicles, particularly Sport Utility Vehicles (SUVs) and light-duty commercial trucks, which require highly sophisticated traction management hardware to handle their elevated centers of gravity and diverse weather conditions

The automotive industry is undergoing a monumental shift driven by technological innovations, stringent safety regulations, and an increasing consumer preference for intelligent vehicle systems. At the forefront of active vehicle safety is the Traction Control System (TCS). Designed to prevent wheel slip and maintain optimal traction between the vehicle's tires and the road surface especially during acceleration on slippery, wet, or uneven terrains TCS has evolved from a premium luxury feature into a standard automotive requirement.

According to comprehensive research by The Insight Partners, the global Traction Control System Market size is expected to reach US$ 10.56 billion by 2031. The market is anticipated to register a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2025 to 2031. This steady and robust growth is primarily fueled by the escalating production of passenger vehicles, commercial trucks, and electric vehicles (EVs) globally, alongside a rising awareness of road safety.

Government mandates across major regions including North America, the European Union, and parts of Asia-Pacific requiring Electronic Stability Control (ESC) and Anti-lock Braking Systems (ABS), which natively integrate TCS, act as a primary catalyst for market expansion. Furthermore, the integration of these systems into entry-level and mid-tier vehicles in emerging economies is broadening the market's geographic footprint.

The primary objective of a Traction Control System is to maximize longitudinal tire force while maintaining lateral stability. When the system detects a wheel spinning faster than the others, it automatically applies braking pressure to that specific wheel or reduces engine power to regain grip. This capability significantly reduces the risk of hydroplaning and loss of control during sharp cornering or sudden acceleration.

The rapid electrification of the automotive sector is another massive driver for the TCS market. Electric vehicles deliver instant torque, making them highly susceptible to wheel spin during initial acceleration. Consequently, manufacturers are developing advanced, faster-responding electronic TCS architectures tailored specifically for electric and hybrid powertrains. Additionally, the growing consumer demand for Advanced Driver Assistance Systems (ADAS) and autonomous driving features is cementing the importance of next-generation traction management systems, as self-driving platforms require ultra-reliable, real-time chassis and wheel control.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00004321

The global market is characterized by intense competition, with leading automotive component manufacturers continuously investing in research and development to introduce lightweight, cost-effective, and highly responsive safety systems. The prominent industry participants driving innovation in this market include:

ADVICS Co., Ltd

Autoliv Inc

Continental AG

Denso Corporation

Hitachi Automotive Systems Americas Inc

Hyundai Mobis Co., Ltd

Nissin Kogyo Co., Ltd

Robert Bosch GmbH

WABCO Holdings Inc

ZF Friedrichshafen AG

These key players are focusing on strategic collaborations, mergers, acquisitions, and technological expansions to consolidate their market presence. Innovations such as integrated braking systems, which consolidate the ABS, ESC, and TCS software into a single hardware control unit, are becoming the standard offering among these industry giants to reduce overall vehicle weight and manufacturing complexity.

Future Outlook

The future of the Traction Control System market points toward complete software integration and predictive vehicle dynamics. As the automotive industry transitions from traditional mechanical hardware to software-defined vehicles (SDVs), traction control logic will increasingly rely on cloud-connected telemetry, artificial intelligence, and machine learning algorithms. Future TCS architectures will not merely react to wheel slip after it occurs; instead, they will utilize predictive analytics by analyzing real-time weather forecasts, GPS terrain data, and sensor inputs to adjust torque distribution proactively before a tire ever loses grip. Furthermore, the expansion of high-performance multi-motor electric vehicles, which utilize independent torque vectoring at each wheel, will revolutionize the traditional concept of traction control. This technological leap will ensure that the TCS market remains an indispensable, high-value segment of the global automotive ecosystem for decades to come.

Related Reports-

Railway Traction Motors Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The North America inspection drone market leads the global industry due to early automation adoption and strict infrastructure safety regulations. The region’s growth is heavily propelled by the rapid modernization of aging utility grids, expansive oil and gas networks, and massive commercial construction projects. Furthermore, supportive regulatory frameworks established by the Federal Aviation Administration (FAA) are accelerating complex Beyond Visual Line of Sight (BVLOS) operations. Key regional players continually integrate advanced artificial intelligence and sensor payloads to lower asset downtime and eliminate human risk in hazardous industrial environments.

The global industrial landscape is undergoing a massive transformation, driven by automation, digital twins, and advanced robotics. At the forefront of this evolution is the commercial Unmanned Aerial Vehicle (UAV) sector. According to a comprehensive research report by The Insight Partners, the global inspection drone market size is expected to reach US$ 34.4 billion by 2031 from US$ 11.6 billion in 2024. This rapid expansion represents a robust market development, with the industry anticipated to register a compound annual growth rate (CAGR) of 16.8% during the forecast period of 2025–2031.

Historically, asset monitoring across heavy industries such as oil and gas refineries, major power grids, expansive transportation networks, and construction sites depended entirely on manual labor. Workers regularly climbed tall scaffolding, rappelled down wind turbines, or entered hazardous, oxygen-depleted confined spaces to verify structural integrity. These methods are inherently slow, financially draining, and present substantial safety risks. Inspection drones mitigate these challenges by offering automated, high-resolution aerial imaging and advanced data collection tools. They deliver significant cost savings and actionable insights while completely removing human operators from dangerous environments.

Core Market Dynamics and Technological Drivers

The surge in market demand is heavily driven by aging utility infrastructure globally, alongside stricter corporate safety regulations. Modern inspection drones are no longer simple flying cameras; they have evolved into highly specialized flying data-collection platforms. Outfitted with cutting-edge payloads like Light Detection and Ranging (LiDAR), advanced thermal sensors, and multispectral imaging systems, these aerial systems capture precise structural data points that are invisible to the naked human eye.

Structurally, rotary-wing designs currently lead the market due to their capacity to hover stably, take off vertically in tight environments, and closely monitor complex equipment geometries. Simultaneously, the market is seeing a major shift toward automated operations. This shift allows drones to navigate GPS-denied environments such as deep underground mines or heavy metallic indoor boilers completely independently.

Regionally, North America and Europe retain a major portion of global revenue due to their early adoption of predictive maintenance frameworks and stringent infrastructure safety mandates. However, the Asia-Pacific region is emerging as the fastest-growing geographical market. Rapid urbanization, massive smart city initiatives, and expanding energy grids in developing economies like India and China are fueling massive procurement of commercial drone technology.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00014697

Competitive Landscape and Strategic Key Players

The global inspection drone market features an incredibly intense competitive field. Leading manufacturers and software developers continuously innovate to improve flight endurance, strengthen airframe durability, and design industry-specific sensor packages.

The prominent organizations shaping the trajectory of this industry include:

Terra Drone Corp.

ScoutDI AS

Flyability SA

Flybotix SA

Voliro AG

Skydio, Inc.

SZ DJI Technology Co Ltd

AeroVironment Inc

Parrot SA

Delair SAS

Acecore Technologies

These market participants actively focus on strategic expansions, venture capital investments, and collaborative partnerships with global energy and construction conglomerates. By introducing resilient systems such as collision-tolerant indoor cages and omnidirectional aerial platforms these companies successfully lower asset downtime for corporate clients.

Future Outlook

Looking ahead, the future of the inspection drone market will be defined by the deeper convergence of artificial intelligence (AI), machine learning (ML), and cloud analytics. Rather than requiring human operators to manually scrub through hours of raw flight video, next-generation drone ecosystems will deploy AI algorithms directly at the edge to identify structural micro-cracks, corrosion patterns, and thermal anomalies in real-time. Additionally, as global aviation authorities establish standardized regulatory frameworks for Beyond Visual Line of Sight (BVLOS) flights, operations will shift toward decentralized, automated docking stations. These "drone-in-a-box" systems will automatically execute scheduled inspections across hundreds of miles of remote pipelines or electrical grids without a physical pilot on site. Ultimately, this paradigm shift from reactive troubleshooting to autonomous predictive maintenance will solidify drones as indispensable infrastructure assets across the global industrial economy.

Related Reports-

Inspection Drone for Confined Space Market

Drone Inspection and Monitoring Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global industrial landscape is placing a profound emphasis on occupational safety, environmental sustainability, and operational efficiency. Central to this evolution is the deployment of industrial dust collectors essential systems engineered to filter out harmful particulate matter, gases, and airborne contaminants generated during manufacturing processes. According to a comprehensive research report by The Insight Partners, the Industrial Dust Collector Market size is expected to reach US$ 16.18 Billion by 2034 from US$ 10.2 Billion in 2025. The market is estimated to record a CAGR of 5.26% from 2026 to 2034.

Key Market Drivers and Trends

The expansion of the industrial dust collector market is fueled by a combination of strict regulatory frameworks and a growing awareness of health hazards in the workplace. Regulatory bodies globally have established rigorous permissible exposure limits (PELs) to guard against long-term respiratory ailments like silicosis, which are common in mining, construction, and manufacturing environments.

Beyond protecting human health, industrial dust collectors safeguard heavy machinery.Uncontrolled particulate accumulation can settle onto moving machine elements, accelerating equipment degradation, increasing mechanical failure rates, and driving up routine maintenance costs.Furthermore, managing combustible dust is paramount across sectors like woodworking, chemical processing, and food production, where excessive atmospheric dust significantly elevates the risks of catastrophic workplace explosions.

Technological evolution is also altering the market landscape. Modern manufacturing plants are shifting away from traditional systems that operate uniformly at maximum capacity, which strains electrical grids and increases facility costs. Instead, current design paradigms focus heavily on energy optimization, integrating advanced pulse-jet cleaning systems with automated pulse intervals and intelligent variable speed drives. These intelligent systems alter power usage dynamically depending on real-time operational loads, promoting eco-friendly, energy-efficient manufacturing.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00009160

Industry Key Players

The global industrial dust collector marketplace features a mixture of established multinational engineering corporations and specialized filtration technology providers. These players are focused on continuous product development, strategic partnerships, and regional expansions to meet evolving clean-air standards.

Key players operating in the industrial dust collector market include:

3M

Aerotech Inc.

Alstom SA, Ltd

American Air Filter Company, Inc.

Atlas Copco

Beltran Technologies, Inc

Camfil APC

CECO Environmental

Donaldson Company, Inc

Nederman Holding AB

These organizations are progressively engineering modular, highly adaptable filtration configurations. These systems help diverse industrial end-users minimize their ecological footprint while maintaining compliance with local workplace regulations.

Market Segmentation and Insights

The market is analyzed across various parameters, including technology types, product categories, and end-user industries. By technology, the market includes:

Baghouse Dust Collectors: Widely preferred for heavy-duty industrial processing because of their ability to handle immense volumes of gas and highly diverse, coarse particulate streams.

Cartridge Collectors: Highly valued in facilities with limited space where high-efficiency filtration of fine, sub-micron airborne dust is necessary.

Cyclone Dust Collectors: Utilizing centrifugal forces to isolate larger, abrasive particles before they can reach secondary filters, lowering overall equipment wear.

Electrostatic Precipitators (ESPs): Utilizing electrical charging fields to trap ultra-fine particulates from exhaust gases with very little resistance to industrial airflow.

From an end-user standpoint, key sectors such as cement production, pharmaceutical manufacturing, metallurgy, chemicals, and food processing remain the primary consumers. The continuous mechanization and automation within these spaces demand consistent, high-capacity air filtration to sustain peak manufacturing uptime.

Future Outlook

Looking ahead, the future of the industrial dust collector market will be defined by the integration of Industry 4.0 technologies and the push toward net-zero industrial emissions. The deployment of Internet of Things (IoT) sensors within dust collection systems is moving the market from reactive maintenance to predictive servicing. Real-time tracking of filter pressure drops, airflow velocities, and particulate emissions will allow operations teams to address system inefficiencies before component failures occur.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global infrastructure landscape is undergoing a massive transformation, driven by rapid urbanization, aging municipal systems, and a heightened public focus on hygiene and sanitation. At the heart of this transformation is the maintenance of vital underground utilities. The Sewer and Drain Cleaning Services Market size is expected to reach US$ 8,415.25 million by 2031 from US$ 5,565.87 million in 2024. The market is estimated to register a CAGR of 6.0% during 2025–2031. This steady trajectory reflects the indispensable nature of specialized plumbing, maintenance, and wastewater management infrastructure in both residential and industrial sectors worldwide.

Market Drivers and Changing Infrastructure Demands

Several macro-economic and technical factors are propelling the sewer and drain cleaning services sector forward. In many developed regions, municipal pipeline networks have been operational for decades, making them highly susceptible to structural deterioration, root intrusion, and severe blockages. Concurrently, expanding urban centers in developing economies are putting an unprecedented load on existing wastewater frameworks.

Environmental regulations have also become considerably stricter. Regulatory authorities are increasingly penalizing commercial entities and municipalities for sewage overflows or untreated wastewater leaks, prompting a shift from reactive emergency repairs to proactive, scheduled maintenance protocols. Furthermore, extreme weather events caused by shifting global climates have resulted in frequent flooding, placing immense pressure on storm drains and demanding immediate, high-capacity cleaning interventions.

Technological Advancements Reshaping the Market

The industry is moving away from purely mechanical, invasive rod-and-cable methods toward sophisticated, technology-driven diagnostic and cleaning procedures. High-definition closed-circuit television (CCTV) camera inspections have become standard practice, allowing technicians to locate structural defects or blockages with pin-point accuracy without digging.

For clearance, hydro-jetting technology which utilizes ultra-high-pressure water streams to blast away grease, scale, and debris is heavily favored for its efficiency and eco-friendliness, as it eliminates the need for harsh chemical cleaners. Additionally, trenchless pipe rehabilitation techniques like Cured-in-Place Pipe (CIPP) lining are gaining popularity, enabling service providers to repair internal pipe structures from within existing access points, saving clients both time and significant excavation costs.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00040907

Key Industry Players

The competitive arena of the sewer and drain cleaning services market features a mix of massive, franchised commercial networks and highly specialized regional industrial contractors.

Key players operating in this space include:

Clean-Co Systems

Len The Plumber

Rooter Hero Plumbing

Benjamin Franklin Franchising SPE LLC.

Roto-Rooter Group Inc

Modern Plumbing Industries, Inc.

Mr. Rooter

Bob Oates

Haller Enterprises

Neptune Plumbing

Augusta Industrial Services

Frank’s Repair Plumbing, Inc.

These organizations are actively sustaining their market dominance by investing in advanced fleet vehicles, expanding their geographic service footprints through franchise networks, and implementing digital scheduling and dispatch platforms to enhance customer experience.

Future Outlook

Looking ahead, the sewer and drain cleaning services market is poised to become smarter and more integrated. The future of the industry lies in the adoption of Internet of Things (IoT) sensors within municipal and commercial plumbing networks, allowing for real-time monitoring of flow rates and sediment accumulation. This shift will enable service providers to transition completely into predictive maintenance models, clearing structural vulnerabilities before a physical backup even occurs. Additionally, as water scarcity escalates globally, technologies that recycle hydro-jetting water directly inside service trucks are expected to gain widespread adoption. Backed by expanding smart city initiatives and an unyielding global demand for sanitary living conditions, the market will remain a resilient and highly lucrative sector of the broader utility infrastructure industry through 2031 and beyond.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

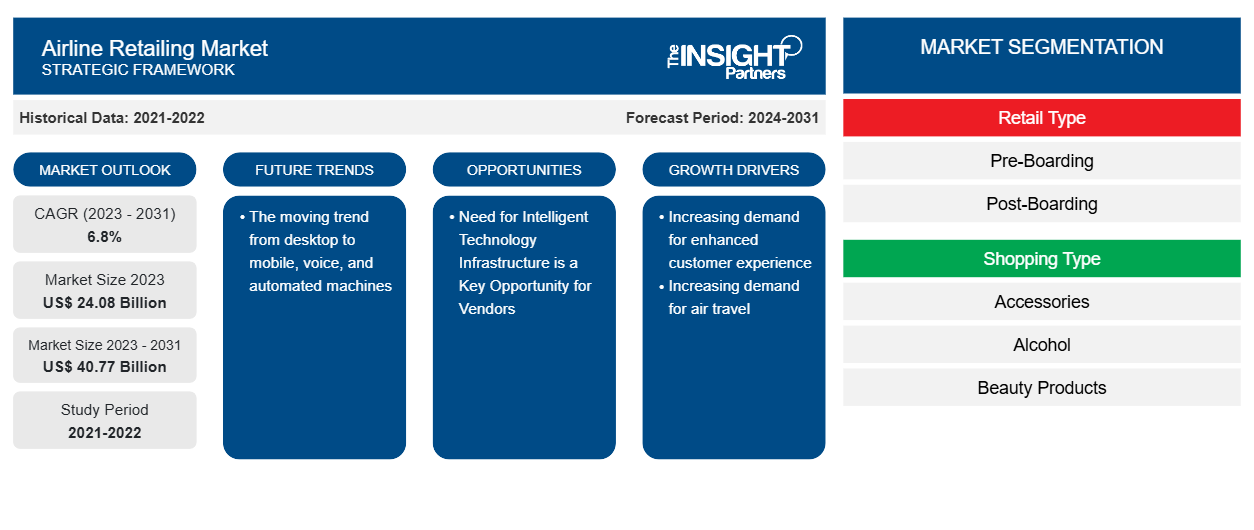

Driven by early technology adoption and a mature aviation ecosystem, the North America airline retailing market is experiencing substantial modernization. The United States, in particular, acts as a primary hub for this transition, as major carriers aggressively integrate IATA’s New Distribution Capability (NDC) standards to bypass legacy distribution bottlenecks. North American airlines are heavily prioritizing hyper-personalization, utilizing cloud infrastructure and artificial intelligence to offer tailored ancillary options such as customized baggage pricing, premium lounge access, and co-branded credit card loyalty rewards directly through mobile applications. Furthermore, the presence of major travel technology providers in the region guarantees continuous software innovation, ensuring that North American passenger experiences remain highly frictionless and retail-centric throughout the travel journey.

The commercial aviation landscape is undergoing a massive paradigm shift. Driven by a transition from traditional ticketing to dynamic, customer-centric commerce, the global aviation industry has embraced advanced digital strategies. Today, airlines no longer view themselves as mere transport providers; they operate as modern digital retailers.

According to a comprehensive study by The Insight Partners, the global Airline Retailing Market size is projected to reach US$ 40.77 billion by 2031 from US$ 24.08 billion in 2023. The market is expected to register a CAGR of 6.8% during the forecast period of 2023–2031. This steady growth highlights the rapid adoption of digital storefronts, personalized ancillary services, and artificial intelligence-driven dynamic pricing models designed to elevate the traveler experience.