The global aviation industry relies heavily on intricate technological architectures to ensure the safety, efficiency, and unwavering reliability of commercial, military, and general aviation aircraft. At the very heart of this operational framework lies the aircraft engine fuel system. Responsible for storing, managing, regulating, and delivering fuel to the engine at precise pressures and flow rates, these systems are fundamentally critical to flight performance. As the aerospace sector rebounds from past global disruptions and scales up to meet unprecedented modern travel demand, the aircraft engine fuel systems sector is experiencing strategic and steady growth. This evolution is shaped by an intersection of rising passenger traffic, stringent environmental regulations, and the relentless pursuit of fuel efficiency by airline operators worldwide.

Market Size and Growth Trajectory

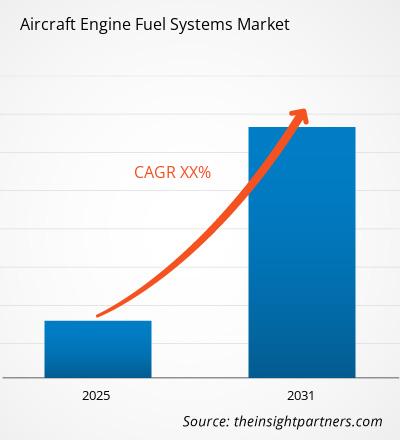

The Aircraft Engine Fuel Systems Market size is expected to reach US$ 77.05 Million by 2034 from US$ 51.42 Million in 2025. The market is estimated to record a CAGR of 4.60% from 2026 to 2034.

While the absolute dollar value of this specific component market may appear niche when compared to broader aerospace valuations, it represents a highly specialized, highly regulated, and vital segment of aerospace engineering. This steady compound annual growth rate is largely driven by the natural replacement cycle of aging aircraft fleets, the aggressive procurement of next-generation commercial jetliners, and increased defense spending across major global economies. Commercial airlines operate on notoriously thin profit margins, and aviation fuel historically represents one of their largest continuous operating expenses. Consequently, airlines are heavily invested in acquiring advanced fuel systems that ensure optimal combustion, prevent fuel starvation, and minimize systemic waste.

Key Market Drivers and Dynamics

Several interconnected factors are fueling the steady expansion of this market. First, the surging demand for commercial air travel in emerging economies particularly across the Asia-Pacific and Middle Eastern regions has necessitated substantial fleet expansions. Aircraft manufacturers are working diligently to ramp up production rates to deliver on immense backlogs of both narrow-body and wide-body aircraft. Every single new jet engine off the assembly line requires a sophisticated, fully integrated fuel delivery and management system.

Second, the global military aerospace sector is currently undergoing a profound modernization phase. Advanced fifth-generation fighter jets, heavy transport aircraft, and complex unmanned aerial vehicles (UAVs) require highly robust, fault-tolerant fuel delivery systems capable of functioning seamlessly under extreme G-forces, high altitudes, and drastically fluctuating temperatures.

Furthermore, international regulatory bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) are implementing ever-stricter environmental and noise protocols. This regulatory pressure forces original equipment manufacturers (OEMs) to design systems that maximize fuel economy and reduce overall carbon footprints, thereby accelerating the market demand for sophisticated upgrades and retrofits to existing aircraft.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00015296

Technological Advancements Reshaping the Industry

Innovation remains the cornerstone of the aircraft engine fuel systems sector. Modern fuel systems are far removed from their purely mechanical predecessors of the mid-20th century. Today, they are deeply integrated with Full Authority Digital Engine Control (FADEC) computing systems. These electronic brains constantly monitor flight conditions, throttle positions, air density, and atmospheric variables to meter the exact micro-amount of fuel required, second by second.

Additionally, there is a prominent industry-wide shift toward "lightweighting." Manufacturers are increasingly utilizing advanced composite materials and additive manufacturing (3D printing) to produce complex fuel system components like pumps, intricate valves, and precision metering units. Lighter parts reduce the overall dry weight of the aircraft, which inherently means the aircraft burns less fuel to stay aloft. Furthermore, the rising integration of smart sensors within the fuel lines allows for predictive maintenance. This technology enables ground crews to monitor system health in real-time and identify wearing fuel system components before they fail in transit, significantly reducing costly aircraft downtime.

Key Players in the Market

The competitive landscape of the Aircraft Engine Fuel Systems Market is characterized by intense research and development initiatives, rigorous safety testing, and long-term supply contracts with major aircraft manufacturers like Boeing, Airbus, Lockheed Martin, and Embraer. The industry is highly consolidated, with a select group of legacy aerospace engineering giants dominating the space due to the high barrier to entry and strict certification requirements.

The prominent key players operating in this dynamic market include:

Honeywell International Inc.

Parker Hannifin Corporation

Woodward, Inc.

Eaton

Triumph Group

Collins Aerospace, a Raytheon Technologies company

Andair LTD

Secondo Mona S.p.A.

Crane Aerospace and Electronics

Meggitt PLC

Future Outlook

Looking ahead to 2034 and beyond, the Aircraft Engine Fuel Systems Market is poised for transformative technological shifts, primarily dictated by the global aerospace industry’s ambitious commitment to achieving net-zero carbon emissions by 2050. A major focal point for manufacturers will be the widespread adoption of Sustainable Aviation Fuels (SAF) and, eventually, liquid hydrogen propulsion. Future fuel systems will need to be fundamentally re-engineered to handle the unique chemical properties, lower lubricity, and complex thermal dynamics of these alternative power sources. Moreover, as the industry begins actively testing hybrid-electric aircraft architectures, traditional fuel management systems will evolve to bridge the gap between conventional combustion and auxiliary electric power generation. Ultimately, the companies that can successfully adapt their fuel system technologies to align with a greener, smarter, and highly digital aviation ecosystem will be the ones that dominate the skies of tomorrow.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The management of municipal and industrial waste is undergoing a massive transformation worldwide. Rapid urbanization, population growth, and a heightened global focus on sustainability have placed tremendous pressure on traditional waste management workflows. At the center of this transformation is the humble trash truck now evolving from a purely mechanical vehicle into a highly sophisticated, technology-enabled asset. As cities look to optimize their sanitation logistics and reduce environmental impacts, the infrastructure supporting waste collection is expanding rapidly.

According to a comprehensive market analysis, the global Trash Truck Market size is projected to reach US$ 21.97 billion by 2034 from US$ 16.16 billion in 2025. The market is anticipated to register a CAGR of 3.47% during the forecast period 2026-2034. This steady economic growth reflects a deeper systemic shift toward automated collection systems, fleet electrification, and strict regulatory mandates regarding carbon emissions.

Key Drivers Fueling Market Growth

Several interconnected factors are steering the steady expansion of the trash truck market over the next decade. First and foremost is the exponential rise in global municipal solid waste generation. As emerging economies develop and urban clusters grow denser, the absolute volume of refuse requiring collection grows with them. Traditional collection methods are proving insufficient to meet this demand safely and efficiently.

Furthermore, municipal authorities face stringent regulatory pressures to decrease the environmental footprints of their service fleets. Heavy-duty diesel trucks have historically been a significant source of local particulate matter and greenhouse gas emissions. This challenge has sparked substantial investment in alternative powertrains, specifically compressed natural gas (CNG) and fully electric configurations. Electric trash trucks are highly suited for urban collection routines, which feature predictable, short routes with frequent stop-and-start cycles that allow for effective regenerative braking.

Operational efficiency is another dominant driver. Modern fleet operators are increasingly opting for automated side loaders (ASLs) over traditional rear loaders. Automated arms allow a single operator to complete entire routes without stepping out of the cabin, significantly reducing labor shortages, lowering injury rates, and speeding up collection times per household.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022491

Industry Ecosystem and Prominent Leaders

The market is characterized by a mix of specialized waste management equipment manufacturers, automotive giants, and industrial machinery innovators. These companies are actively forming strategic partnerships, launching low-emission product lines, and integrating telematics systems to maintain their competitive edge.

Key players operating in the global trash truck market include:

AB Volvo: A leader in commercial transport solutions, pioneering heavy-duty electric chassis tailored specifically for urban refuse collection.

BAS Mining Trucks: Known for heavy-duty payload engineering, providing rugged infrastructure vehicles capable of handling high-capacity industrial waste.

Cummins Inc.: A critical power-solutions provider advancing natural gas, hybrid, and hydrogen-fuel-cell propulsion systems for vocational truck fleets.

Combilift Material Handling Solutions: Specializing in innovative material handling and customized logistics machinery that interfaces with industrial waste processing.

Caterpillar: A global leader in heavy machinery, providing heavy-duty infrastructure, earthmoving, and foundational handling assets vital to landfill management and large-scale refuse sorting.

Doosan Corporation: Contributing robust industrial powertrains and heavy construction equipment utilized in solid waste distribution.

Deutz AG: Focusing on highly efficient eco-friendly diesel and alternative fuel engines designed to comply with strict global emission standards.

ETF HOLDING B.V.: Engineering innovative transport concepts and heavy-axle configurations suitable for specialized, high-capacity industrial haulage.

Liebherr: Delivering highly advanced material handlers, wheel loaders, and specialized machines engineered specifically for the rigorous environments of recycling yards and waste management centers.

Labrie Enviroquip Group: A premier manufacturer of top-tier waste collection bodies, renowned for their advanced side-loading, front-loading, and rear-loading technology.

Technological Horizons and Regional Dynamics

Regionally, North America and Europe continue to hold substantial market shares due to early adoption of strict environmental regulations, high labor costs that incentivize automation, and robust municipal budgets. However, the Asia-Pacific region is poised to display the fastest growth rate. Government initiatives like smart city developments, structured waste-segregation mandates, and large-scale modernization of municipal fleets in countries like China and India are transforming regional market dynamics.

On the technological front, IoT (Internet of Things) integration is changing how these vehicles function. Telematics platforms now track real-time fuel efficiency, hydraulic health, and automated container counts. When paired with smart, sensor-equipped waste bins, trash trucks can dynamic-route through cities skipping empty bins and prioritizing overflowing ones to minimize wear and tear, fuel burn, and traffic congestion.

Future Outlook

The future of the trash truck market lies at the intersection of total automation and net-zero emissions. Over the next decade, expect the industry to pivot entirely away from conventional diesel, making fully electric and hydrogen-fueled fleets the standard for municipal contracts. As autonomous driving technology matures, we will likely see highly controlled, low-speed autonomous or semi-autonomous collection vehicles operating during off-peak night hours to further alleviate daytime urban congestion. The integration of advanced computer vision on robotic arms will also enable trucks to identify contamination in recycling bins right at the curb. Ultimately, trash trucks will transition from mere transport vehicles into data-gathering hubs crucial to the circular economy.

Related Reports-

Connected Truck Telematics Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global construction industry is undergoing a significant transformation, driven by an urgent demand for speed, precision, and structural longevity. At the heart of this evolution is the concrete finishing sector, where achieving a perfectly flat, durable surface is paramount for warehouses, industrial complexes, and commercial buildings. As a result, the ride-on trowel market has emerged as a critical segment within construction equipment manufacturing. These powerful machines allow operators to sit comfortably while managing large-scale concrete smoothing, offering unmatched efficiency compared to traditional walk-behind models.

Market Size and Growth Projections

According to comprehensive data provided by The Insight Partners, the market is positioned for steady, long-term expansion. The Ride-on Trowel Market size is expected to reach US$ 316.9 Million by 2034 from US$ 267.61 Million in 2025. This growth reflects a steady rise in industrial floor specifications and massive infrastructure projects worldwide. The market is estimated to record a CAGR of 2.14% from 2026 to 2034.

While a Compound Annual Growth Rate (CAGR) of 2.14% represents a mature and stable growth trajectory, it underscores a highly resilient sector. The steady rise indicates consistent replacement cycles of aging machinery and a continuous shift toward mechanized concrete finishing in developing economies.

Key Drivers of Market Expansion

Several macroeconomic and industry-specific factors are fueling the demand for ride-on trowels:

Booming Logistics and Warehousing Sectors: The continuous rise of e-commerce has led to a massive construction wave of fulfillment hubs and mega-warehouses. These modern facilities require "superflat" floors to ensure that high-reach forklifts and automated guided vehicles (AGVs) can operate safely and without disruption. Ride-on trowels are indispensable for achieving these stringent floor flatness tolerances.

Labor Shortages and Cost Management: The construction sector globally faces a persistent shortage of skilled masonry labor. Ride-on trowels mitigate this issue by allowing a single operator to finish thousands of square feet of concrete in a fraction of the time it would take a manual crew, drastically lowering labor costs and shortening project timelines.

Urbanization and Infrastructure Investments: Emerging economies across Asia-Pacific and Latin America are investing heavily in urban infrastructure, high-rise developments, and transport hubs, widening the geographical playground for machinery manufacturers.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00023408

Understanding the Technology: Hydrostatic vs. Mechanical

Ride-on trowels are broadly classified by their drive systems, with the market divided between mechanical and hydrostatic models.

Mechanical Drive Trowels: Utilizing heavy-duty clutches and belts, these models are traditionally favored for their lower upfront cost and relative ease of maintenance on standard job sites.

Hydrostatic Drive Trowels: Representing the premium segment of the market, hydrostatic models use hydraulic pumps and motors to turn the rotors. This system offers smoother power delivery, variable speed control, and eliminates the wear items like belts and clutches, making them increasingly popular for high-demand, heavy-duty applications.

Weight distribution, pitch control systems (both manual and hydraulic), and steering responsiveness are other key competitive frontiers where manufacturers continuously innovate to enhance operator comfort and floor quality.

Competitive Landscape: Key Market Players

The ride-on trowel market features a mix of established global heavy-equipment giants and highly specialized construction machinery manufacturers. These companies focus on expanding their distribution networks, refining hydraulic controls, and introducing low-emission powerplants to comply with strict global environmental regulations.

The prominent players steering the market forward include:

Multiquip Inc.

ALLEN ENGINEERING CORPORATION

Bartell Machinery Systems

Atlas Copco

Masterpac

MBW Incorporated

Parchem Construction Supplies

Wacker Neuson SE

BetonTrowel

Jamshedji Constro Equip Private Limited

These manufacturers are increasingly integrating advanced LED lighting packages for night operations and ergonomically redesigned seating positions to reduce operator fatigue during long concrete pours.

Future Outlook

Looking toward the horizon, the ride-on trowel market is on the cusp of an environmental and technological paradigm shift. As global emissions regulations tighten, the industry is witnessing a strong push toward alternative powertrains, notably battery-electric and hybrid ride-on trowels. Electric models not only reduce a contractor's carbon footprint but also solve a major industry headache: operating inside enclosed spaces where exhaust fumes from traditional gasoline or diesel engines present severe safety hazards. Furthermore, the long-term integration of smart sensors capable of monitoring concrete dryness and floor flatness in real-time will turn these finishing machines into data-gathering hubs. This ensures that the ride-on trowel market will remain an adaptive, vital pillar of global industrial development well up to 2034 and beyond.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The quality of fresh water around the world has become a critical topic of discussion for governments, municipal corporations, and individual homeowners alike. Industrialization, agricultural runoff, and aging municipal pipeline infrastructure have increasingly contributed to water contamination. In response, residential and commercial consumers are turning toward robust, comprehensive water filtration solutions. Among these, Point of Entry (POE) water treatment systems have gained substantial traction. Unlike Point of Use (POU) systems, which filter water at a single faucet or showerhead, POE systems are installed directly at the main water line where water enters a building, ensuring that every drop flowing through the property from kitchens to bathrooms and laundry rooms is thoroughly purified.

Market Dynamics and Valuation

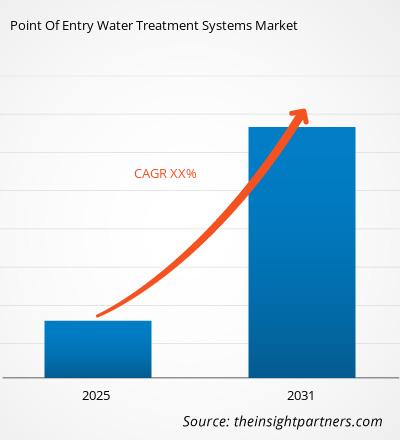

The global demand for clean water is translating into robust financial growth for manufacturers in this sector. The Point Of Entry Water Treatment Systems Market size is expected to reach US$ 15.59 Billion by 2034 from US$ 10.6 Billion in 2025. The market is estimated to record a CAGR of 4.94% from 2026 to 2034.

This steady growth trajectory is fueled by several macroeconomic and environmental factors. Urbanization across emerging economies in Asia-Pacific and Latin America is leading to a construction boom, where new residential complexes and commercial buildings are pre-installing POE systems as a value-added feature. Additionally, growing awareness regarding waterborne diseases, heavy metal contamination (such as lead and arsenic), and the negative impacts of hard water on household appliances and plumbing systems is urging consumers to invest in long-term, high-capacity water treatment infrastructure.

Technological advancements have also made these systems much more appealing. Modern POE systems are no longer just basic sediment filters; they integrate multi-stage purification technologies including carbon filtration, reverse osmosis, ultraviolet (UV) disinfection, and automated water softening. The incorporation of smart monitoring systems, which alert users via smartphone applications when filters need replacing or when water quality fluctuates, has further boosted consumer adoption rates.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022496

Prominent Industry Participants

The POE water treatment market is characterized by a mix of established multinational corporations and specialized water technology firms. These players are continuously investing in research and development to launch energy-efficient, eco-friendly, and cost-effective filtration solutions to maintain their market dominance.

The key players operating in the global Point of Entry water treatment systems market include:

3M Company – Renowned for its advanced membrane technology and high-flow filtration systems designed for both residential and commercial applications.

Honeywell International Inc – Provides smart water filtration solutions, incorporating automation and robust sediment filtration systems.

General Electric – Offers a widely trusted portfolio of whole-house filtration and water softening systems known for reliability and scale reduction.

Best Water Technology (BWT) AG – A European leader focusing on innovative ecological water treatment technologies, including magnesium-enriched water systems.

Calgon Carbon Corporation – Specializes in activated carbon technologies that effectively remove organic compounds, chlorine, and odor from primary water sources.

Pentair plc – A major global player delivering comprehensive sustainable water solutions, ranging from heavy-duty residential POE systems to commercial water management.

The Dow Chemical Company – Supplies cutting-edge ion exchange resins and filtration component technologies utilized globally in high-end water treatment systems.

Danaher Corporation – Operates through its specialized environmental and applied solutions platforms, delivering advanced water quality testing and purification systems.

Watts Water Technologies Inc – Focuses on water quality, water safety, and flow control solutions, providing robust whole-house filtration and scale-prevention systems.

Culligan International – A highly recognized brand offering fully customized residential and commercial POE water softening and filtration services.

Market Segmentation and Regional Insights

To understand the widespread adoption of these systems, it is essential to look at how the market is segmented. By product type, the market includes water softeners, filtration systems (such as carbon and sediment filters), disinfection systems, and reverse osmosis systems. Water softeners hold a significant market share due to the widespread issue of hard water, which damages expensive plumbing and reduces the lifespan of water-based appliances like washing machines and water heaters.

Geographically, North America and Europe hold a dominant position in the global market. This is primarily attributed to strict environmental regulations, high consumer awareness regarding health and wellness, and the presence of leading market players. However, the Asia-Pacific region is projected to register the fastest growth rate during the forecast period. Rapid industrial development, deteriorating natural water quality due to industrial effluents, and a growing middle-class population with increasing disposable income are pushing countries like China, India, and countries in Southeast Asia to adopt whole-house water filtration units rapidly.

Future Outlook

The future of the Point of Entry water treatment systems market looks exceptionally promising, driven by a paradigm shift toward sustainability and intelligent home automation. As global water scarcity intensifies, the emphasis will increasingly transition from mere filtration to intelligent water conservation and recycling. Future POE systems are expected to feature enhanced zero-waste reverse osmosis technologies and chemical-free disinfection methods, aligning with global green building standards. Furthermore, the integration of Artificial Intelligence (AI) and the Internet of Things (IoT) will become standard, enabling predictive maintenance, real-time contaminant tracking, and synchronized communication with municipal smart grids. As public awareness regarding microplastics, PFAS (forever chemicals), and pharmaceutical residues in tap water escalates, the reliance on comprehensive POE systems will evolve from a luxury household upgrade into an indispensable health and infrastructure necessity worldwide.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The automotive industry is undergoing a monumental shift driven by electrification, autonomous driving technology, and a relentless focus on passenger safety and comfort. At the heart of a vehicle's handling mechanism lies the steering column a critical component that translates the driver’s input into mechanical action. As vehicles become smarter and increasingly automated, the demands placed on steering column systems are evolving rapidly. According to a comprehensive research report by The Insight Partners, the steering column market is positioned for exponential growth over the next decade, fueled by technological breakthroughs and rising vehicle production worldwide.

Market Size and Growth Trajectory

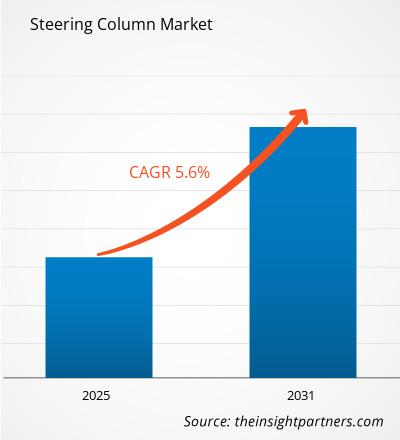

The Steering Column Market size is expected to reach US$ 22.34 Billion by 2034 from US$ 6.62 Billion in 2025. The market is estimated to record a CAGR of 16.42% from 2026 to 2034. This highly impressive compound annual growth rate highlights a period of intense modernization and infrastructure changes within the global automotive supply chain.

Historically viewed as a rigid mechanical link, the steering column is being completely reimagined. The remarkable growth trajectory is heavily supported by the increasing adoption of Electric Power Steering (EPS) and Electronic Hydraulically Assisted Power Steering (E-HPS) systems, particularly across commercial and passenger vehicle segments. These modern systems not only optimize fuel efficiency and lower carbon emissions by reducing parasitic engine load, but they also offer superior vehicle handling capabilities that appeal to safety-conscious consumers worldwide.

Market Drivers and Technological Dynamics

Several key dynamics are pushing the steering column market into a new era of expansion:

Rise of Steer-by-Wire (SbW) Systems: One of the most disruptive trends in automotive engineering is the shift toward steer-by-wire technologies. By eliminating the physical, mechanical connection between the steering wheel and the road wheels, SbW relies entirely on electronic signals. This revolution fundamentally changes the role of the steering column, requiring advanced sensors, actuators, and electronic control units (ECUs) to simulate road feedback and manage wheel angles.

Enhanced Safety Standards and Crashworthiness: Regulatory bodies across the globe continue to mandate stringent safety guidelines for automotive manufacturing. Modern steering columns must feature energy-absorbing mechanisms that collapse safely during a frontal collision, protecting the driver from severe impact injuries. The development of advanced telescopic and tiltable columns provides both custom ergonomic comfort and optimized safety configurations.

Autonomous and Semi-Autonomous Vehicles: As Advanced Driver Assistance Systems (ADAS) and Level 3+ autonomous driving become mainstream, the design requirements for steering columns are changing. In fully autonomous modes, retractable steering columns are increasingly desired to maximize cabin space and provide a lounge-like environment for passengers.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022722

Key Industry Players

The global steering column landscape features a mix of well-established automotive component manufacturers and specialized engineering firms that drive localized and international supply chains. Prominent entities operating within this marketplace include:

Anhui Finetech Machinery Co., Ltd.

BNL (UK) Limited

Coram Europe S.r.l.

Hangzhou Feiyue Automobile Parts Co., Ltd.

HYUNDAIGLOVIS co.,ltd

M.S. Group

Ningbo CIE Corporation

Nakanishi Metal Works Co Ltd

Pailton Engineering Ltd.

Technymon LTD

These key players are actively investing in robust research and development initiatives, focusing on lightweight materials such as aluminum alloys and magnesium to decrease overall vehicle weight without compromising structural integrity. Strategic partnerships, mergers, and geographic expansions remain common tactics used by these companies to secure long-term contracts with original equipment manufacturers (OEMs).

Segmental Insights

The steering column market can be categorized by vehicle type, column type, and geography. By vehicle type, passenger cars continue to command a massive share of the market due to high production volumes and consumer demand for premium features like electric adjustment and memory settings. Concurrently, the commercial vehicle sector is showing robust growth as logistics networks expand globally, necessitating heavy-duty steering columns that reduce driver fatigue during long-haul transit.

Geographically, the Asia-Pacific region stands out as a manufacturing powerhouse and a primary revenue generator. Rapid urbanization, increasing disposable income, and massive automotive production hubs in China, Japan, India, and South Korea propel regional demand. Meanwhile, Europe and North America remain critical hubs for high-tech innovations, where stricter emission norms and early adoption of autonomous technologies drive the market toward premium, electronically advanced steering solutions.

Future Outlook

The future of the steering column market is intrinsically tied to the total digitization of the vehicle cockpit. As the industry moves closer to fully autonomous transport, the traditional steering column will transition from a purely mechanical driver-interface tool into an intelligent, modular component capable of seamless integration with vehicle AI. We will likely see a surge in adaptive steering technologies that adjust steering ratios on the fly based on vehicle speeds and road conditions. Furthermore, the push for sustainability will compel manufacturers to adopt circular economy practices, utilizing recycled metals and eco-friendly manufacturing processes.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global aviation industry is experiencing a profound transformation, propelled by the resurgence of global passenger traffic, modernization of commercial fleets, and a relentless push toward environmental sustainability. At the heart of aircraft design and operational efficiency are flight control systems, particularly aerodynamic surfaces that manage lift and drag during critical phases of flight. Among these, aircraft slat systems play a vital role. Positioned on the leading edge of airplane wings, slats are deployable aerodynamic surfaces that alter the wing's shape to increase lift during low-speed operations, such as takeoff and landing.

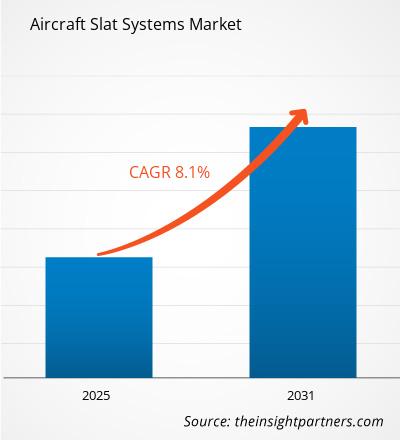

According to a comprehensive market study, the global Aircraft Slat Systems Market size is projected to reach US$ 3.1 Billion by 2034 from US$ 1.76 Billion in 2025. The market is anticipated to register a CAGR of 6.6% during the forecast period 2026–2034. This robust growth reflects the critical necessity of advanced aerodynamic components in modern aviation, driven by the expanding order books of major aircraft manufacturers and the ongoing development of military and commercial aerospace platforms.

Dynamics Driving the Aircraft Slat Systems Market

The primary catalyst for the aircraft slat systems market is the exponential increase in commercial aircraft deliveries. As airlines globally look to replace aging, less fuel-efficient fleets with next-generation narrow-body and wide-body aircraft, the demand for sophisticated slat systems has escalated. Leading edge slats allow aircraft to fly at higher angles of attack and lower speeds without stalling, which is crucial for safety and short-runway performance.

Moreover, structural advancements in aerospace engineering are heavily influencing market dynamics. Traditional mechanical slat systems are progressively being augmented or replaced by smarter, lightweight actuation mechanisms. The integration of advanced materials, such as carbon-fiber-reinforced polymers (CFRP) and lightweight titanium alloys, has allowed manufacturers to reduce the overall weight of the wing assembly. A lighter slat system directly correlates to reduced fuel consumption and lower carbon emissions—two metrics that are vital for airlines navigating strict global environmental regulations.

Additionally, military modernization programs across North America, Europe, and the Asia-Pacific region are providing substantial momentum. Governments are investing heavily in tactical transport aircraft, fighter jets, and maritime patrol planes, all of which require highly specialized, durable slat systems capable of enduring extreme operational stress and harsh environments.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00026537

Key Players in the Global Market

The aircraft slat systems market is characterized by a mix of established tier-1 aerospace component manufacturers, structural assembly specialists, and precision tooling providers. These companies are actively investing in research and development to introduce automated manufacturing techniques and additive manufacturing (3D printing) to optimize production.

The prominent players operating in the global aircraft slat systems market include:

Sonaca Group: A global leader in aerostructures, specialized in the development, manufacturing, and assembly of advanced wing leading edges.

Spirit Aerosystems, Inc.: One of the world’s largest independent designers and manufacturers of aerostructures, providing critical wing components for major commercial programs.

Triumph Group Inc.: A key supplier of aerospace systems and structures, offering comprehensive capabilities across the lifecycle of aircraft flight control mechanisms.

Korea Aerospace Industries Limited (KAI): A premier aerospace and defense company contributing significantly to structural assemblies and international commercial wing programs.

Hexagon AB: A global leader in digital reality solutions, providing precision metrology and manufacturing software vital for ensuring the strict tolerances required in slat production.

Sandvik Coromant: A world-renowned supplier of cutting tools and tooling solutions, driving efficiency in machining complex aerospace materials used in wing systems.

GKN Aerospace (a Melrose company): A pioneer in advanced aerostructures and wing technologies, focusing heavily on integrating lightweight materials into leading-edge architectures.

Kawasaki Heavy Industries: A major contributor to global aerospace manufacturing, providing high-quality structural components and sub-assemblies for commercial aircraft wings.

Premium Aerotech: A leading tier-1 supplier focused on the structures of commercial and military aircraft, utilizing cutting-edge automated carbon-fiber manufacturing.

S.S. White Technologies, Inc.: A specialist in flexible shaft technology, providing highly reliable rotary power transmission solutions used in flight control and actuation systems.

Technological Trends Shaping Production

The manufacturing of aircraft slat systems is transitioning rapidly toward Automation 4.0. Given the safety-critical nature of these components, precision is paramount. Companies like Hexagon AB and Sandvik Coromant supply the metrology and high-performance tooling necessary to machine complex aerodynamic curves out of tough alloys. Meanwhile, structural integrators like Spirit Aerosystems and Sonaca Group are incorporating advanced automated fiber placement (AFP) to produce lightweight composite slats.

Furthermore, there is a distinct technological shift toward electro-mechanical actuation (EMA) systems over traditional hydraulic systems. Electro-mechanical systems remove the heavy fluid lines associated with hydraulics, reducing maintenance overhead, removing potential leak risks, and enhancing the overall responsiveness of the flight control surfaces.

Future Outlook

The future of the aircraft slat systems market looks exceptionally promising, anchored by continuous innovation and structural changes in aircraft architecture. Over the next decade, the industry is expected to witness an accelerated transition toward "smart wings" and adaptive aerodynamic technologies. Manufacturers are exploring morphing wing concepts where slats and flaps seamlessly adjust shape rather than deploying on mechanical tracks, optimizing aerodynamics across all flight phases. As urban air mobility (UAM) and electric vertical takeoff and landing (eVTOL) aircraft progress from concepts to commercial realities, the demand for compact, highly integrated, and lightweight lift-enhancement systems will expand into entirely new market segments. Driven by these engineering breakthroughs and a projected backlog of thousands of commercial airliners, the aircraft slat systems market is well-positioned for sustained capital investment, ensuring its steady upward trajectory through 2034 and beyond.

Related Reports-

Aircraft Engine Forging Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global automotive landscape is undergoing a monumental paradigm shift, transitioning rapidly from mechanical reliability to digital sophistication. At the heart of this transformation lies the humble yet increasingly complex component: the automotive switch. Functioning as the vital user interface between vehicle occupants and the machine's intricate electrical networks, automotive switches regulate everything from primary ignition systems and windows to advanced luxury electronics and advanced driver-assistance systems (ADAS). As vehicular electronics evolve, the market for these components is expanding exponentially.

The Automotive Switch Market is expected to register a CAGR of 4.08% from 2026 to 2034, with the market size expanding from US$ 55.33 Billion in 2025 to US$ 79.29 Billion by 2034. This steady economic trajectory underscores the indispensable nature of control mechanisms within contemporary commercial and passenger vehicles, particularly amid a global wave of electrification and a surging consumer appetite for premium, high-tech cabins.

Market Dynamics and Growth Drivers

The expansion of the automotive switch market is heavily driven by the profound trend toward vehicle electrification.The rapid proliferation of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) requires sophisticated power electronics and specialized high-voltage control systems.Unlike conventional internal combustion engine (ICE) vehicles that rely on simpler mechanical linkages, EVs require advanced power distribution, localized thermal-management switches, and intelligent battery regulation interfaces.

Concurrently, safety mandates and consumer demands for enhanced luxury features have drastically increased the number of switches integrated per vehicle. Advanced driver-assistance systems require a multitude of physical or capacitive controls right at the driver’s fingertips, traditionally localized on multi-function steering wheels. Furthermore, features such as multi-zone climate control, power-adjustable seats with memory retention, electronic parking brakes, and panoramic sunroofs are transitioning from luxury exclusives to standard entry-level packages. Each of these conveniences introduces multiple specialized switches, amplifying the absolute volume of switch architectures built by original equipment manufacturers (OEMs).

Additionally, the integration of Human-Machine Interfaces (HMIs) has modernized the composition of automotive switches.Rather than standard plastic toggles, modern vehicle cockpits incorporate smart tactile panels, illuminated switches, and capacitive sensors with integrated haptic feedback, balancing aesthetic minimalism with functional safety requirements.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00023840

Key Market Players

The global automotive switch industry features a highly competitive and semi-consolidated landscape, led by prominent multinational electronic and Tier-1 automotive component suppliers. These entities consistently invest in robust research and development to align their product portfolios with stringent electronic safety standards (such as ISO 26262) and emerging EV architectures.

The major players dominating the global automotive switch market ecosystem include:

Alps Electric Co., Ltd.

Continental AG

Hella KGaA Hueck and Co.

Johnson and Johnson

Omron Corporation

Panasonic Corporation

Robert Bosch GmbH

Tokai Rika Co., Ltd.

Valeo

ZF Friedrichshafen AG

These market leaders are increasingly executing strategic collaborative ventures, mergers, and product innovations to secure their market footprints. By leveraging micro-electromechanical systems (MEMS) and durable touch-sensitive technologies, these companies cater directly to prominent global OEMs seeking to redefine modern cockpit aesthetics.

Segmentation and Regional Analysis

To comprehend the micro-dynamics of the market, the automotive switch industry can be analyzed by switch type, vehicle type, application, and distribution channel.By switch type, the market includes pushbutton switches, rotary switches, toggle/rocker switches, and increasingly, capacitive touchpads.Applications span lighting systems, engine start/stop setups, HVAC controls, steering assemblies, window/door locks, and infotainment overrides.

Geographically, the market is characterized by prominent manufacturing hubs and soaring vehicle production volumes across the Asia-Pacific region, spearheaded by China, India, and Japan.The rapid localization of EV supply chains in Asia-Pacific positions it as the dominant consumer of automotive electronics. Meanwhile, North America and Europe continue to showcase high market value, primarily driven by strict regulatory mandates regarding active safety controls, high adoption of connected luxury platforms, and a resilient consumer aftermarket industry as global fleet ages increase.

Future Outlook

Looking toward the horizon, the future of the automotive switch market lies in the deep integration of tactile components with smart, touchless, and smart cabin ecosystems. While touchscreens and voice-activation software continue to redefine vehicle interiors, physical and tactile backup switches will remain fundamentally critical due to global automotive safety and emergency override protocols. We anticipate a prominent shift toward hybrid interior designs, where seamless smart-surface switches injected into premium wood, leather, or glass accents remain hidden until illuminated. Furthermore, the incorporation of artificial intelligence and Internet-of-Things (IoT) enabled switch networks will foster highly predictive, energy-efficient cabin systems that adjust intuitively to individual driver behaviors. As next-generation autonomous and autonomous-ready platforms emerge over the next decade, manufacturers who balance absolute hardware reliability with sleek, touch-sensitive design aesthetics will position themselves at the peak of the global automotive marketplace.

Related Reports-

Automotive Steering Wheel Switch Market

Automotive Engine Fastener Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The automotive engineering landscape has shifted profoundly over the last few decades, with electronic fuel injection (EFI) systems taking center stage in modern passenger vehicles. However, the legacy and specialized application of the mechanical carburetor remain deeply embedded in various global automotive sectors. A comprehensive study by The Insight Partners reveals that the demand for automobile carburetors continues to adapt and flourish across specific geographical regions, aftermarket spaces, and niche two-wheeler and classic car ecosystems.

The Automobile Carburetor Market is expected to register a CAGR of 5.32% from 2026 to 2034, with the market size expanding from US$ 2.94 Billion in 2025 to US$ 4.69 Billion by 2034. This steady economic expansion proves that despite stringent emission regulations worldwide, the utility, cost-efficiency, and simplicity of carburetor systems retain immense value for global manufacturers and vehicle owners alike.

A carburetor’s fundamental role is to blend air and fuel in the exact ratios required for an internal combustion engine to run cleanly and efficiently. While modern premium cars rely heavily on computerized sensors and multi-point fuel injection systems, carburetors are incredibly resilient components. They require minimal electronic architecture, making them highly attractive for budget-conscious vehicle manufacturing, vintage restorations, small engines, and high-performance racing platforms where analog customization is preferred.

A primary driver for the sustained growth of this market is the skyrocketing demand for two-wheelers, particularly in developing economies across the Asia-Pacific region, Latin America, and parts of Africa. In these areas, motorcycles, scooters, and mopeds serve as the primary mode of personal and commercial transport. Manufacturers frequently opt for carbureted engines in lower-displacement two-wheelers because they keep the initial purchase cost of the vehicle low and make maintenance affordable for everyday consumers who may not have access to highly specialized diagnostic tools.

Furthermore, the automotive aftermarket sector provides a massive cushion for the industry. Millions of legacy vehicles and classic cars around the world rely on routine replacement parts to stay roadworthy. Enthusiasts who rebuild classic American muscle cars, historical European sports models, or older utility trucks frequently seek out brand-new, high-fidelity reproduction carburetors or upgrade to high-performance aftermarket variants that can handle higher horsepower and customized airflows.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00026049

Key Market Competitors Shaping the Landscape

The competitive environment of the automobile carburetor market is defined by a blend of specialized high-performance brands, massive original equipment manufacturers (OEMs), and regional industrial manufacturing giants. These organizations focus heavily on material durability, tight manufacturing tolerances, and optimizing airflow to satisfy both performance metrics and strict regional environmental standards.

The prominent entities steering the progression of this sector include:

Holley Performance Products, Inc: Renowned worldwide in the high-performance aftermarket and racing spheres, Holley sets the benchmark for high-displacement and custom-tuned carburetors.

Dellorto S.p.a.: An iconic Italian brand with deep roots in European motorcycle racing and passenger vehicle fuel systems, recognized for high-precision engineering.

EControls: Innovators in fuel management systems, offering specialized carburetor architectures that bridge traditional mechanical designs with alternative fuel and low-emission requirements.

Edelbrock, LLC.: A massive staple in the American automotive culture, specialized in aftermarket performance parts and premium replacement carburetors for muscle cars and hot rods.

Keihin FIE: A major powerhouse in the two-wheeler industry, known for supplying high-reliability fuel management components to leading motorcycle manufacturers.

Kunfu Group: A major Chinese manufacturing entity producing high-volume fuel system components for global export and diverse engine applications.

Mikuni American Corp.: Highly regarded for its exceptional Japanese engineering, Mikuni carburetors are widely used in performance motorcycles, powersports, and marine vehicles.

Ruixing Carburetor Manufacturing Co., Ltd.: A major supplier focused on scaling high-quality, cost-efficient carburetor systems for a wide array of small engines and automotive setups.

Youall Industry and Trade, Inc.: A growing industrial competitor utilizing advanced production lines to manufacture carburetors tailored to changing global small-engine demands.

Zama: A prominent global producer specializing primarily in small engine carburetion, critical for small utility vehicles and specialized power tools.

Future Outlook

The long-term horizon for the global automobile carburetor market from 2026 out to 2034 highlights a landscape defined by strategic adaptation rather than generic stagnation. As urban centers continue to enforce tighter regulatory frameworks on greenhouse gas emissions, carburetor manufacturers are heavily investing in research and development to engineer eco-friendly solutions. This includes developing hybrid-carburetion systems, electronic carburetors (e-carburetors) that utilize rudimentary electronic control units to precisely monitor air-fuel ratios, and using lighter, more robust alloy materials that resist corrosion from ethanol-blended fuels. While electric drivetrains take over the high-end passenger vehicle segments, the reliability, simplicity, and low capital cost of carbureted systems will secure their relevance across international powersports, vintage collections, and industrial and agricultural equipment frameworks for years to come.

Related Reports-

Automotive Engine Management Systems Market

Automotive Engine Fastener Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The automotive sector is undergoing a massive transformation, driven by technological breakthroughs, tightening emission norms, and changing consumer preferences. At the heart of internal combustion engine (ICE) reliability is the camshaft drive system. The automotive cam chain, or timing chain, plays a critical role in synchronizing the rotation of the crankshaft and the camshaft. This precise synchronization ensures that the engine's valves open and close at the exact correct time during each cylinder's intake and exhaust strokes. As engines become more compact and power-dense, the demand for highly durable, low-friction, and noise-optimized cam chains has skyrocketed.

According to an industry report by The Insight Partners, the Automotive Cam Chain Market is expected to register a CAGR of 4.13% from 2026 to 2034, with the market size expanding from US$ 2.79 Billion in 2025 to US$ 4.02 Billion by 2034. This steady economic growth emphasizes the continued relevance of advanced internal combustion engine components, even during a broader industry shift toward electrification.

Key Market Drivers and Technological Developments

Several core factors are fueling the expansion of the global automotive cam chain market:

Downsizing and Turbocharging of Engines: Modern automotive engineering heavily favors downsized, turbocharged engines. These setups generate higher pressures and thermal loads within the engine block. Compared to traditional rubber timing belts, cam chains offer superior tensile strength, durability, and a longer lifecycle—frequently lasting the entire lifetime of the vehicle. This makes them the preferred choice for auto manufacturers looking to maintain reliability under harsher operating environments.

Strict Emission Regulations: Regulatory bodies worldwide are enforcing incredibly stringent carbon emission targets. To comply, manufacturers are designing high-efficiency engines that require micro-precise valve timing. Advanced cam chains with optimized link profiles reduce friction and mechanical energy losses, directly contributing to better fuel economy and reduced carbon footprints.

Rising Vehicle Production in Emerging Economies: Rapid urbanization, rising disposable incomes, and industrial expansion in regions like Asia-Pacific and Latin America have caused localized automotive production numbers to climb. The high volume of passenger cars and commercial vehicles manufactured in these areas creates a strong foundation for the cam chain market.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00021958

Market Segmentation and Insights

The automotive cam chain market can be broadly segmented by vehicle type, chain type, and sales channel.

By Vehicle Type: Passenger cars hold a dominant market share due to high production volumes globally. However, light commercial vehicles (LCVs) and heavy commercial vehicles (HCVs) represent a crucial steady segment, as heavy-duty fleet operations rely heavily on the long-term reliability of steel cam chains to avoid costly maintenance downtime.

By Chain Type: Roller chains and silent chains are the two primary product variants. Silent chains are rapidly gaining market share in premium and mid-range passenger vehicles because they reduce noise and operate smoothly at high engine revolutions. Roller chains remain popular in motorcycles and heavy-duty commercial applications due to their exceptional ruggedness.

By Sales Channel: The market is divided into Original Equipment Manufacturers (OEMs) and the aftermarket. OEMs drive the majority of market value as cam chains are installed during initial vehicle assembly. However, the aftermarket retains steady value from older vehicles requiring high-mileage replacements or tensioner system overhauls.

Competitive Landscape & Key Players

The global automotive cam chain market features a mix of well-established multinational component manufacturers and specialized regional players. These companies focus on materials science innovations, applying specialized heat treatments and surface coatings (such as vanadium or chromium carbo-nitriding) to improve wear resistance.

The prominent key players operating in this marketplace include:

Tsubakimoto

BorgWarner

Schaeffler

DAIDO KOGYO

Iwis

LGB

Qingdao Choho

TIDC

Rockman Industries

Ferdinand Bilstein GmbH + Co. KG

These industry leaders frequently collaborate directly with automotive OEMs to design custom timing systems tailored to next-generation engine platforms, securing their market footprint through long-term supply agreements.

Future Outlook

Looking ahead, the future of the automotive cam chain market will be heavily shaped by hybrid vehicle architectures and regional variations in energy transitions. While pure battery electric vehicles (BEVs) do not utilize internal combustion engines, full hybrids (HEVs) and plug-in hybrid electric vehicles (PHEVs) rely on highly optimized internal combustion engines that cycle on and off frequently. This operational cycle puts unique, sudden stresses on the timing system, creating a specialized niche for high-durability cam chains. Furthermore, the rising integration of smart manufacturing processes, lightweight steel alloys, and advanced low-viscosity engine oils will force cam chain designs to become lighter and slicker than ever before. While the market faces headwinds from rapid EV adoption in certain regions, the massive volume of hybrid and traditional ICE vehicles across developing territories ensures a resilient, profitable trajectory toward its US$ 4.02 Billion valuation by 2034.

Related Reports-

Marine Engine Monitoring System Market

Automotive Engine Management Systems Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The automotive industry is in the midst of a historic paradigm shift, transitioning from rigid mechanical designs to intelligent, responsive ecosystems. At the forefront of this evolution is the development of active body panels exterior automotive components that dynamically alter their shape, position, or functionality in real-time based on driving conditions, vehicle speed, and environmental changes. These systems, which include adaptive grille shutters, deployable spoilers, smart air dams, and energy-storing body panels, are vital tools for modern automakers aiming to optimize vehicle performance and meet rigid environmental standards.

Market Valuation and Growth Trajectory

According to a comprehensive market study by The Insight Partners, the financial and technological footprints of this industry are expanding rapidly. The Automotive Active Body Panels Market size is expected to reach US$ 1.91 Billion by 2034 from US$ 1.41 Billion in 2025. The market is estimated to record a CAGR of 3.87% from 2026 to 2034.

This steady growth highlights a broader industry trend: active aerodynamics and smart exterior integration are no longer exclusive privileges reserved for elite supercars. Instead, they are rapidly flowing down into premium sedans, high-volume sport utility vehicles (SUVs), and mass-market hybrid and electric vehicles (EVs).

Core Market Drivers

The steady expansion of the automotive active body panels market is propelled by a combination of regulatory pressures, the global shift toward vehicle electrification, and advancements in materials science.

1. Stringent Emission Norms and Aerodynamic Optimization

Governments worldwide continue to enforce rigid limits on carbon emissions while mandating aggressive targets for fuel economy. To meet these requirements, original equipment manufacturers (OEMs) cannot rely solely on internal engine refinements; they must minimize aerodynamic drag. Active body panels address this need by dynamically adjusting to airflow. For instance, active grille shutters close at highway speeds to minimize drag, lowering energy consumption and reducing a vehicle's carbon footprint.

2. Eliminating Range Anxiety in Electric Vehicles

As the global fleet shifts toward electrification, aerodynamic efficiency directly influences consumer purchasing decisions. In electric vehicles, every decimal point reduction in the coefficient of drag (Cd) translates to extended battery range. Active spoilers, side skirts, and air curtains deploy automatically at high speeds to keep the airflow smooth, optimizing battery conservation and directly alleviating "range anxiety" for EV drivers.

3. Materials Science and Structural Evolution

Historically, the weight of the motors, sensors, and linkages required to actuate body panels threatened to offset the efficiency gains they provided. However, the modern market is utilizing lightweight, high-strength materials like aluminum, carbon fiber-reinforced polymers, and engineered thermoplastics. These advanced materials deliver the necessary structural integrity without adding unnecessary bulk to the vehicle's frame.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00021953

Key Market Competitors

The active body panels landscape features a mix of traditional automotive manufacturing giants and specialized component engineering firms. These entities are investing heavily in research and development to integrate complex electronics, sensors, and actuators directly into exterior body panels.

Key players shaping the global marketplace include:

General Motors

Daimler AG

Ford Motor Company

Toyota Motor Corporation

Porsche AG

Honda Motor Company, Ltd.

Volkswagen Group

Tata Motors

Voestalpine Metal Forming GmbH

Nissan Motor Company Ltd.

These companies are establishing strategic partnerships with technology providers to seamlessly merge physical automotive structures with artificial intelligence (AI)-driven control software. This ensures that panels respond instantly and reliably to real-time data inputs.

Market Challenges

Despite a highly positive growth outlook, the industry must navigate distinct challenges before achieving absolute mass-market adoption. The primary obstacle is the high initial cost associated with complex electronic actuators, precise sensor networks, and advanced composite materials. In highly price-sensitive vehicle segments, the cost of installing these systems can sometimes outweigh the perceived efficiency benefits.

Additionally, long-term mechanical reliability remains a critical talking point. Exterior moving parts are continuously exposed to harsh weather conditions, road debris, and minor impacts, requiring strict engineering validation to minimize lifetime maintenance issues for consumers.

Future Outlook

The future of the automotive active body panels market points toward absolute integration, where the boundary between mechanical hardware and digital intelligence completely disappears. Over the next decade, look for the market to move beyond basic aerodynamic adjustments and embrace multifunctional, energy-storing body panels. These advanced systems will incorporate thin-film solar cells to actively charge vehicle batteries while parked, alongside integrated thermal management skins that adapt to regulate internal battery and cabin temperatures. Furthermore, as autonomous driving systems and Advanced Driver Assistance Systems (ADAS) become standard, active body panels will evolve to shield fragile radar and LiDAR sensors from environmental hazards, securing their place as a foundational technology for next-generation mobility.

Related Reports-

Automotive Security System Market

Electric Light Commercial Vehicle Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876