Modern warfare is no longer constrained by the setting of the sun. The ability to dominate the battlespace under the cover of darkness has evolved from a tactical advantage into an absolute strategic necessity. As global defense forces prioritize 24/7 operational readiness and asymmetric warfare capabilities, the technologies that enable soldiers to see, target, and navigate in zero-light environments are experiencing unprecedented demand.

According to a comprehensive study by The Insight Partners, the global Military Night Vision System Market size is projected to reach US$ 14.73 billion by 2034 from US$ 9.57 billion in 2025. This steady growth is anticipated to register a compound annual growth rate (CAGR) of 5.54% during the forecast period from 2026 to 2034.

Primary Catalysts Driving Market Expansion

Several macroeconomic and geopolitical dynamics are converging to fuel the growth of the military night vision market. Chief among these is the escalating level of geopolitical tension worldwide. Border disputes, counter-terrorism operations, and the rise of gray-zone warfare have forced nations to modernize their infantry and specialized units. Defense departments are heavily investing in personal soldier equipment to maximize survivability and combat lethality.

Furthermore, night-time missions are statistically preferred for covert operations, reconnaissance, and surgical strikes. To execute these safely, defense forces require systems that offer maximum clarity, extended range, and minimal latency. This has shifted the market focus from basic image intensification to advanced digital and hybrid fusion systems.

Technological Shifts: From Intensification to Sensor Fusion

The military night vision landscape is undergoing a massive technological transition. Traditionally, systems relied purely on Image Intensification (I2) tubes, which amplify ambient light (like starlight or moonlight) to create a visible image. While newer Generation 3 and Generation 4 I2 systems are incredibly sensitive and power-efficient, they struggle in absolute darkness, such as deep caves or subterranean structures.

To mitigate this, the industry is rapidly adopting Sensor Fusion Technology. Fusion systems combine traditional image intensification with thermal imaging (infrared sensors that detect heat signatures). By overlaying a thermal outline onto a high-resolution ambient image, soldiers can spot a hidden enemy behind foliage or camouflage while maintaining clear environmental awareness.

Additionally, the integration of Augmented Reality (AR) overlays onto night vision goggles allows real-time tactical data such as navigation waypoints, blue-force tracking, and target markers to be projected directly into the operator's field of view.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00006030

Competitive Landscape and Key Players

The military night vision system market is highly competitive, characterized by established defense giants and specialized electro-optical component manufacturers. These entities focus on securing long-term government contracts, reducing the size, weight, and power (SWaP) metrics of devices, and improving digital resolution.

Prominent players driving innovation and holding significant market share include:

ATN Corp – Renowned for commercial and tactical smart digital night vision and thermal optics.

BAE Systems – A global defense leader providing advanced integrated helmet systems and digital night vision technologies.

Bharat Electronics Limited (BEL) – A premier Indian defense PSU supplying night vision goggles, weapon sights, and binoculars to domestic and international forces.

Collins Aerospace – Specializes in high-performance airborne and ground electro-optical systems.

Elbit Systems Ltd. – An international defense electronics company at the forefront of sophisticated helmet-mounted displays and fusion goggles.

FLIR Systems, Inc. (A Teledyne Technologies Company) – Global pioneer in thermal imaging sensors and infrared surveillance systems.

Intevac, Inc. – Renowned for its digital night vision sensors, particularly low-light CMOS technology utilized in military aviation.

L3Harris Technologies, Inc. – A dominant supplier of next-generation night vision goggles (such as the ENVG-B) featuring integrated thermal and AR capabilities for the US military.

Photonis Technologies SAS – A crucial manufacturer of high-performance image intensifier tubes used by various global device assemblers.

Thales Group – A European defense leader providing cutting-edge, lightweight optronics and night vision sights for dismounted soldiers.

Segmental and Regional Insights

Geographically, North America currently holds a dominant position in the market, primarily driven by the massive procurement budgets of the US Department of Defense and continuous soldier modernization programs. However, the Asia-Pacific region is poised to display the fastest growth rate over the forecast period. Countries like India, China, and South Korea are aggressively updating their military hardware to counter local security threats, creating a highly lucrative environment for domestic and foreign electro-optics manufacturers.

In terms of systems, helmet-mounted devices and weapon-mounted sights remain the highest-volume segments, though vehicular and airborne night-vision installations are seeing stable growth to support armored units and nighttime aviation logistics.

Future Outlook

The future of the military night vision system market lies in full digitalization and software-defined optics. As standard analog tubes gradually give way to digital low-light sensors, future systems will easily integrate into broader battlefield management networks. We can expect artificial intelligence (AI) to play a crucial role at the edge, offering automatic target recognition (ATR) and filtering out environmental noise like smoke, dust, or sudden flash blindness. As manufacturers successfully lower the cost of sensor fusion and digital components, these advanced capabilities will transition from elite special forces down to standard infantry, ensuring that tomorrow's military forces maintain unchallenged supremacy in the dark.

Related Reports-

Enhanced Flight Vision System Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global aviation landscape is undergoing an unprecedented evolution. As passenger volumes surge and commercial airlines expand their fleets, the complexity of managing global airspace has escalated dramatically. To keep pace with this demand, the global Air Traffic Management (ATM) industry is embracing sweeping structural and technological transformations.

According to a comprehensive industry report by The Insight Partners, the Air Traffic Management Market size is projected to reach US$ 9.85 Billion in 2025 and is expected to reach US$ 16.56 Billion by 2034. The market is expected to register a CAGR of 7.31% during the forecast period. This steady growth highlights an urgent, industry-wide push to modernize aging aviation infrastructure, optimize fuel consumption, and ensure the highest standards of safety across international borders.

Driving Forces Behind Modern Air Traffic Management

The growth of the ATM market is fueled by a combination of recovering passenger demand, regulatory mandates, and the emergence of new airborne technologies. Legacy radar-based control systems are gradually reaching their capacity limits. As a result, civil aviation authorities and airport operators worldwide are turning toward integrated digital platforms to maximize airspace efficiency.

Key drivers reshaping the ATM ecosystem include:

Airspace Congestion and Capacity Optimization: Major international hubs face daily bottlenecks that ripple across regional networks. Modern ATM systems utilize precise data analytics to sequence arrivals and departures closer together without compromising safety margins.

Decarbonization and Green Routing: Airlines are under immense pressure to lower carbon emissions. Advanced ATM software enables "Trajectory-Based Operations" (TBO), allowing aircraft to fly optimized, fuel-efficient paths rather than rigid, legacy airways.

Unmanned Traffic Integration: The rapid proliferation of commercial drones, logistics quadcopters, and Urban Air Mobility (UAM) concepts demands a unified infrastructure. Traditional ATM systems are evolving into Unmanned Traffic Management (UTM) ready ecosystems to manage low-altitude traffic.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00005933

Key Market Competitors

The global ATM landscape features a mix of aerospace giants, defense conglomerates, and specialized software developers providing hardware, communications networks, and surveillance systems. Prominent entities shaping the market include:

Advanced Navigation and Positioning Corporation

BAE Systems PLC

Harris Corporation

Honeywell International, Inc.

Intelcan Technosystems Inc.

Lockheed Martin Corporation

Raytheon Company

SAAB AB

Saipher ATC

Thales Group

These market participants focus heavily on collaborative partnerships with national Air Navigation Service Providers (ANSPs) to roll out next-generation software architectures, artificial intelligence diagnostic tools, and resilient cybersecurity frameworks.

Technical Innovations: Automation, Cloud, and AI

At the heart of the modern ATM transformation is the shift toward automation and digital twins. Traditional control towers are increasingly supplemented or replaced by Remote Digital Towers (RDTs). Using high-definition cameras, infrared sensors, and real-time telemetry, controllers can safely manage airport operations from hundreds of miles away—a breakthrough particularly beneficial for managing multiple low-volume regional airports from a centralized hub.

Furthermore, artificial intelligence is migrating from a theoretical tool to active operational support. AI algorithms analyze historical flight data, current weather conditions, and aerodynamic wake turbulence patterns to predict potential traffic conflicts up to an hour before they occur. This predictive capability shifts the air traffic controller's role from reactive management to proactive routing.

Regional Variations in Infrastructure Upgrades

The deployment of these systems varies significantly across geographic regions:

North America & Europe: Driven heavily by well-established modernization frameworks like NextGen (FAA) and SESAR (Single European Sky ATM Research). The focus in these regions centers on satellite-based navigation, digital data communications (Data Comm), and tight integration of cybersecurity layers to defend critical aviation networks.

Asia-Pacific & Middle East: Experiencing massive infrastructure investments due to new airport constructions and major fleet expansions by regional carriers. ANSPs in these markets are investing aggressively in high-capacity automation platforms and advanced surveillance tools to cope with some of the densest air corridors in the world.

Future Outlook

The future of the Air Traffic Management market points toward an interconnected, cloud-native aviation ecosystem. Over the coming decade, traditional siloed national architectures will give way to cross-border, cloud-based data sharing networks. This shift will allow for seamless regional flight handoffs and significantly reduced flight delays. Additionally, as machine learning algorithms assume greater responsibility for routine routing adjustments, human controllers will transition to strategic supervisors overseeing automated workflows. The integration of artificial intelligence, green flight paths, and low-altitude drone tracking will redefine global airspace, ensuring that the skies remain highly scalable, environmentally conscious, and safe for decades to come.

Related Reports-

Air Traffic Control Equipment Market

Commercial Air Traffic Management Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

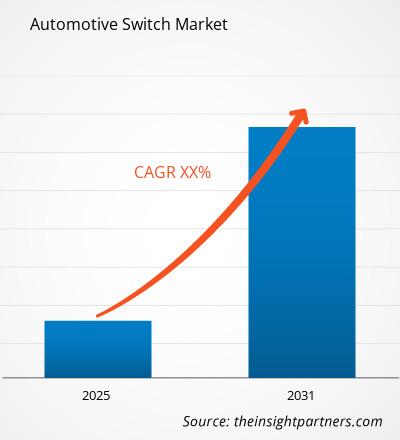

The automotive industry is undergoing a monumental shift, transitioning from traditional mechanical engineering to software-defined, highly connected vehicles. At the heart of this evolution lies the automotive switch a seemingly basic component that serves as the crucial interface between the vehicle's driver, passengers, and its electronic ecosystem. As modern vehicles adopt increasingly sophisticated electronic architectures, the automotive switch market is witnessing consistent and healthy growth.

The Automotive Switch Market is expected to register a CAGR of 4.08% from 2026 to 2034, with the market size expanding from US$ 55.33 Billion in 2025 to US$ 79.29 Billion by 2034. This growth is fueled by a combination of stricter automotive safety mandates, an increase in standard electronic comfort features, and the global adoption of electric vehicles (EVs).

Market Dynamics and Drivers

A key catalyst accelerating the automotive switch market is the massive influx of consumer electronic features into cars. Today’s consumers demand the same level of touchscreen responsiveness, ambient lighting control, and digital convenience in their vehicles that they experience with smartphones and tablets. Consequently, conventional toggle and rotary switches are rapidly making way for smart touchpads, haptic feedback buttons, and multi-functional steering wheel controls.

Furthermore, the electrification of vehicles plays an instrumental role. Electric vehicles utilize sophisticated electronic control units (ECUs) to manage everything from battery cooling systems to advanced driver-assistance systems (ADAS). This expansion of a vehicle's electrical framework naturally requires an increased quantity of high-voltage and low-voltage switches to reliably regulate power and signal transmission.

Safety regulations mandated by governments globally also serve as a vital market driver. Standards requiring standard inclusion of backup cameras, electronic stability control, and automated emergency braking systems necessitate a dense array of sensory and manual override switches inside the cabin and under the hood.

Segmentation Overview

The automotive switch market can be segmented based on switch type, application, vehicle type, and geography. By switch type, the market includes push-button switches, toggle switches, rotary switches, and multi-function steering switches. Among these, multi-function steering and haptic smart switches are gaining substantial market share due to their role in reducing driver distraction.

In terms of application, switches are widely classified into powertrain systems, chassis systems, body electronics, and infotainment systems. The body electronics and comfort systems segment accounts for a considerable share, driven by features like power windows, electronic seat adjustments, sunroof controls, and motorized mirrors. By vehicle type, the passenger car segment continues to lead the demand, though commercial vehicles are gradually catching up as logistics companies upgrade to telematics-equipped smart trucks.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00023840

Competitive Landscape: Key Market Players

The global automotive switch market is highly competitive and characterized by the presence of prominent tier-1 automotive suppliers and electronics manufacturers. These enterprises are actively focusing on strategic product launches, lightweight component designs, and smart switch technologies to sustain their market positions.

The key players dominating this market landscape include:

Alps Electric Co., Ltd.

Continental AG

Hella KGaA Hueck and Co.

Johnson and Johnson

Omron Corporation

Panasonic Corporation

Robert Bosch GmbH

Tokai Rika Co., Ltd.

Valeo

ZF Friedrichshafen AG

These industry leaders heavily invest in Research and Development (R&D) to engineer switches capable of handling harsh automotive conditions such as extreme temperatures, high vibration, and moisture while maintaining ergonomic and aesthetic appeal.

Regional Analysis

Geographically, Asia-Pacific remains the powerhouse of the automotive switch market. The region’s dominance is anchored by massive automotive production hubs in China, Japan, India, and South Korea. Increased consumer spending power, paired with a rising demand for premium passenger cars featuring advanced cabin comfort, further accelerates the regional market.

Europe and North America represent highly mature markets. In these regions, growth is heavily supported by rigid safety standards and a swift consumer transition toward premium luxury electric vehicles. Original Equipment Manufacturers (OEMs) in Europe and North America are focusing tightly on integrating intelligent touch-capacitive panels, forcing traditional switch manufacturers to modernize their current portfolios.

Future Outlook

The future of the automotive switch market is inextricably linked to the concepts of vehicle autonomy, intuitive human-machine interfaces (HMI), and premium cabin interior design. Moving forward, the distinction between a mechanical switch and a digital screen will continue to blur. We can expect to see a surge in "smart surfaces" where switches are seamlessly integrated into wooden dashboards, leather doors, or glass panels, becoming visible and operational only when a hand approaches. As autonomous driving technology matures and drivers transition into passengers, the interior vehicle cabin will transform into a mobile living space, generating a massive need for localized, highly sophisticated switches that prioritize luxury, gesture control, and personalized comfort. The ongoing expansion toward a US$ 79.29 Billion valuation by 2034 stands as a testament to the enduring, critical role that switches will play in the smarter, safer vehicles of tomorrow.

Related Reports-

Automotive Steering Wheel Switch Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

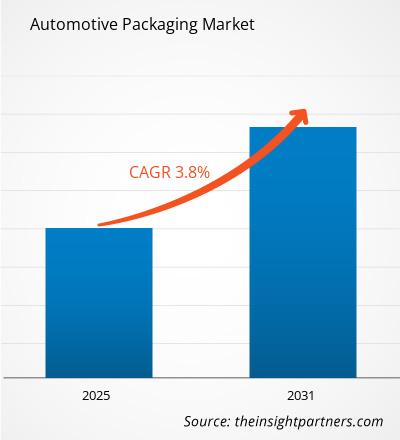

The automotive manufacturing sector relies on a highly complex, interconnected global supply chain where millions of components ranging from heavy steel engines to microscopic electronic sensors must be transported safely across continents. As vehicle designs shift toward advanced electronics and electrification, the protective systems handling these components are undergoing a parallel evolution.

The Automotive Packaging Market size is expected to reach US$ 13.18 Billion by 2034 from US$ 9.27 Billion in 2025. The market is estimated to record a CAGR of 4.50% from 2026 to 2034. This steady expansion underscores the crucial role that specialized logistics and packaging solutions play in modern automotive manufacturing and the aftermarket sector.

Key Drivers Shaping the Market

Several macroeconomic and industry-specific shifts are steering the development of the automotive packaging sector:

The Transition to Electric Vehicles (EVs): Unlike traditional internal combustion engines, electric vehicles depend on massive, highly sensitive lithium-ion battery packs, power electronics, and intricate wiring systems. These components require unique packaging solutions that offer thermal insulation, impact resistance, and compliance with stringent international regulations for hazardous materials.

Rising Electronic Complexity: The integration of Advanced Driver Assistance Systems (ADAS), autonomous driving technologies, and infotainment screens has turned modern cars into computers on wheels. Fragile semiconductor-based parts are highly vulnerable to electrostatic discharge (ESD), moisture, and physical vibrations during transit. Protective packaging using specialized anti-static films, custom molded foam, and robust cushioning is vital to prevent multi-million dollar supply chain losses.

The Push for Circular Economies: Automakers are facing heavy pressure from regulatory frameworks and internal corporate social responsibility (CSR) targets to reduce their carbon footprint. This has accelerated the transition from single-use, disposable packaging to returnable and reusable systems. Reusable plastic crates, steel racks, and bulk containers offer long-term cost efficiencies and minimize waste.

Just-In-Time (JIT) Manufacturing: To save on warehousing costs, original equipment manufacturers (OEMs) operate on tight JIT delivery schedules. Packaging must be standardized, modular, easily stackable, and collapsible when empty to maximize shipping container space and optimize inbound and outbound logistics.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00026590

Material and Segment Insights

The global market features a balanced blend of rigid, flexible, and corrugated solutions designed to handle specific component categories:

Rigid Packaging (Crates, Pallets, and Racks): Heavy components like engines, gearboxes, and suspension systems are transported via heavy-duty, reusable plastic and steel racks. These provide maximum structural protection and are built to handle multiple round trips across supply chain routes.

Corrugated Solutions: Corrugated cardboard boxes and die-cut custom packaging remain highly popular for medium and small-sized spare parts due to their lightweight properties and high recyclability. Advanced corrugated designs offer strong barrier properties and shock resistance at lower initial costs.

Flexible and Protective Packaging: Bubble wraps, expanded polypropylene (EPP) foam inserts, and protective pouches are critical layers within outer boxes. They shield sensitive surfaces from scratches and absorb transit vibrations, ensuring components arrive at the assembly line in pristine condition.

Competitive Landscape

The automotive packaging industry is highly competitive, with global and regional players continuously innovating to introduce lighter, stronger, and more sustainable materials. Companies focus on strategic partnerships with OEMs and invest heavily in localized fabrication to meet precise geometric requirements for vehicle parts.

Key players driving innovation and operational scale within the market include:

Nefab Group

New-Tech Packaging

Kronus

D S Smith

Victory Packaging

Schoeller Allibert

Orcon Industries

PRIMO

Robinson Industries

THIMM Group

Future Outlook

The future of the automotive packaging market will be defined by smart technology and deep sustainability integration. We can expect a significant increase in the adoption of "smart packaging" systems embedded with RFID tags, IoT sensors, and GPS trackers. These technologies will allow logistics managers to monitor the precise location, temperature, and shock exposure of high-value parts like EV batteries in real time. Furthermore, innovations in bio-based plastics and high-strength, lightweight paper composites will help manufacturers satisfy stringent global eco-regulations while driving down shipping weights. As global vehicle production volumes stabilize and move deeper into the electric era, packaging will cease to be treated as a mere transit cost and will instead become a core pillar of lean, digitalized, and green automotive logistics.

Related Reports-

Flexible Packaging Solutions Market

Temperature Controlled Packaging Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

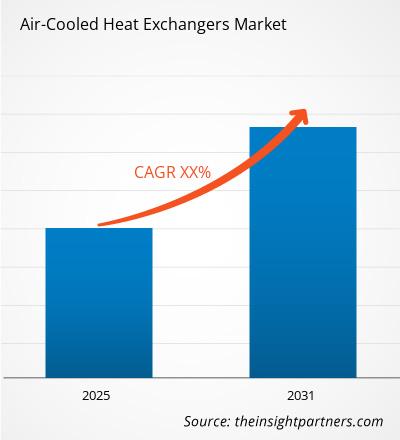

The global industrial landscape is experiencing a massive shift toward sustainability and operational optimization, placing a renewed focus on energy-efficient thermal management systems. Air-cooled heat exchangers (ACHEs) crucial systems used to reject heat from a process fluid directly into the ambient air have emerged as a vital technology across multiple heavy industries. According to a comprehensive research study by The Insight Partners, the global market for these systems is poised for exponential growth over the next decade.

The Air-Cooled Heat Exchangers Market size is expected to reach US$ 8.92 Billion by 2034 from US$ 4.68 Billion in 2025.The market is estimated to record a CAGR of 8.40% from 2026 to 2034. This robust growth trajectory is heavily driven by increasing water scarcity, stricter environmental regulations regarding thermal pollution, and a widespread industrial push toward lowering operational costs.

Market Dynamics and Primary Growth Drivers

Traditional cooling systems heavily rely on water, such as shell-and-tube heat exchangers coupled with cooling towers. However, massive industrial expansion in water-scarce regions has made water conservation a top priority for global enterprises. Air-cooled heat exchangers present an eco-friendly and highly practical alternative because they eliminate the need for an external water supply, thereby removing costs associated with water treatment, chemical conditioning, and disposal.

Furthermore, regulatory frameworks worldwide are tightening constraints on thermal water discharge, which can disrupt aquatic ecosystems when hot water is released back into natural bodies. By utilizing ambient air as the cooling medium, industries can seamlessly comply with strict environmental mandates. Technological advancements are also reshaping the market landscape.Manufacturers are leveraging innovative designs, specialized finned configurations, and eco-friendly materials to dramatically boost thermal efficiency, allowing ACHEs to perform exceptionally well even in high ambient temperature environments.

Segmentation Overview

To provide a detailed outlook of the marketplace, the air-cooled heat exchangers market is categorized into distinct segments based on configuration, material, and end-use industry:

By Configuration: The market is analyzed across Forced Draft, Induced Draft, Horizontal, Vertical, and A-frame designs. Forced draft configurations are highly favored for their ease of maintenance and structural stability, while induced draft units offer superior air distribution and reduced hot air recirculation.

By Material: Material selection is vital for ensuring corrosion resistance and thermal conductivity. The market is segmented into Stainless Steel, Carbon Steel, and Copper, with stainless steel witnessing significant demand in corrosive or highly hygienic industrial processes.

By Industry: ACHEs serve as critical infrastructure across a diverse array of sectors, including Cement, Chemical, Pharmaceutical, Power, Steel, and Oil and Gas. The oil and gas and power generation sectors remain dominant consumers due to the massive scale of cooling required in refineries and thermal power plants.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00025309

Competitive Landscape and Key Players

The global air-cooled heat exchangers market features a blend of established engineering conglomerates and specialized thermal management providers. These entities are consistently investing in research and development, strategic partnerships, and geographic expansions to secure a competitive edge.

The key players operating in the market include:

Alfa Laval

Boldrocchi

Chart Industries

Fbm Hudson Italiana

Howden Group

Kawasaki Heavy Industries, Ltd.

Paharpur Cooling Towers Ltd.

SPG Dry Cooling

SPX Cooling Technologies, Inc.

Thermax Limited

These industry leaders focus on delivering customized, highly reliable, and heavy-duty thermal systems tailored to survive harsh operational environments, ranging from sub-zero arctic oil fields to scorching desert chemical plants.

Regional Market Insights

Geographically, the market spans North America, Europe, Asia-Pacific, South & Central America, and the Middle East & Africa. The United States represents a pivotal hub within North America, heavily supported by a booming oil and gas sector, expanding chemical processing facilities, and a rapid adoption of green technology.

Meanwhile, the Asia-Pacific region is projected to experience the fastest growth rate through 2034. Massive industrialization, continuous infrastructure development in nations like China and India, and the rising demand for electricity are triggering substantial investments in new power and steel manufacturing plants, fueling the regional demand for industrial cooling solutions.

Future Outlook

The future of the air-cooled heat exchangers market points toward hyper-efficiency and digital integration.As industries embrace digital transformation and the Industrial Internet of Things (IIoT), smart monitoring systems are revolutionizing ACHE maintenance.Future designs will increasingly incorporate artificial intelligence (AI) and advanced sensors to predict mechanical failures, monitor fouling, and dynamically adjust fan speeds based on real-time ambient weather conditions. This evolution will dramatically lower energy consumption and mitigate unplanned downtime. Combined with the global transition toward green technologies such as hydrogen production and carbon capture systems, both of which require specialized thermal management the demand for advanced, eco-friendly air-cooled heat exchangers is set to remain exceptionally strong, ensuring a sustainable and profitable horizon for manufacturers worldwide.

Related Reports-

Automotive Heat Exchanger Market

Air Separation Equipment Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global industrial landscape is undergoing a massive transformation, driven by automation, infrastructure development, and the relentless demand for heavy-duty machinery. At the heart of this machinery lies fluid power technology. The mobile hydraulic equipment market is experiencing significant growth, fueled by advancements in construction, agriculture, material handling, and mining sectors worldwide. As industries seek more reliable, efficient, and powerful systems to operate heavy vehicles and machinery, mobile hydraulics have become indispensable.

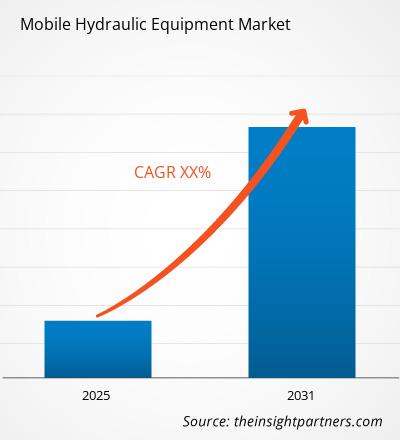

Market Size and Growth Trajectory

According to a comprehensive study by The Insight Partners, the market for mobile hydraulic equipment is on a strong upward trajectory. The Mobile Hydraulic Equipment Market size is expected to reach US$ 23.88 Billion by 2034 from US$ 15.64 Billion in 2025. The market is estimated to record a CAGR of 5.43% from 2026 to 2034. This steady compound annual growth rate reflects the sustained demand for modernized machinery that can withstand harsh operating environments while delivering high power-to-weight ratios.

Driving Factors behind Market Expansion

Several factors are propelling the growth of the mobile hydraulic equipment market. First and foremost is the rapid pace of urbanization and infrastructure development, particularly in emerging economies across the Asia-Pacific and Latin American regions. Governments are investing heavily in smart cities, roadways, bridges, and commercial complexes, all of which require robust construction equipment like excavators, loaders, and cranes equipped with advanced hydraulic systems.

Furthermore, the agricultural sector is adopting high-tech mechanization to increase yield and combat labor shortages. Modern tractors, harvesters, and forestry equipment rely heavily on mobile hydraulics for precise steering, lifting, and tool attachments. Similarly, the e-commerce boom has drastically increased the demand for material handling equipment, such as forklifts and automated guided vehicles (AGVs) in warehouses, further driving market volume.

Technological advancements are also rewriting the rules of the industry. The integration of electronics with fluid power commonly known as electro-hydraulics has allowed manufacturers to design systems with improved energy efficiency, reduced emissions, and superior control accuracy.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00023694

Key Industry Players

The mobile hydraulic equipment market is highly competitive, with several prominent players focusing on innovation, strategic partnerships, and geographical expansion to maintain their market dominance. The leading companies shaping the market include:

JWF Technologies: Known for designing and distributing customized fluid power and motion control systems.

Rheintacho Messtechnik GmbH: A specialist in rotational speed sensors and monitoring systems essential for hydraulic safety and efficiency.

HAWE Hydraulik SE: Highly regarded for its high-pressure hydraulic components and compact systems.

Bosch Rexroth Corporation: A global giant leading the wave of digital transformation and electro-hydraulic solutions.

Daikin Industries Ltd.: Recognized for combining advanced cooling systems with efficient hydraulic power units.

Eaton: A long-time leader in power management, providing durable hydraulic pumps, valves, and cylinders.

Emerson Electric Co.: Delivering smart pneumatic and fluid control technologies that complement mobile hydraulic applications.

Kawasaki Heavy Industries, Ltd.: A pioneer in high-capacity hydraulic pumps and motors used extensively in heavy construction equipment.

Parker Hannifin Corporation: A global leader in motion and control technologies, offering one of the broadest portfolios of hydraulic solutions.

WEBER-HYDRAULIK GmbH: Renowned for developing customized, high-quality hydraulic cylinders and lifting systems.

These organizations are continuously investing in research and development (R&D) to build lighter, more compact, and leak-free hydraulic solutions that meet stringent global environmental regulations.

Future Outlook

The future of the mobile hydraulic equipment market is deeply intertwined with sustainability and digitalization. Over the next decade, the industry is expected to witness an accelerating shift toward "smart hydraulics." By embedding IoT sensors and data analytics into hydraulic components, operators can perform predictive maintenance, thereby reducing costly equipment downtime and optimizing fuel consumption.

Additionally, the global push toward electrification poses both a challenge and an incredible opportunity for the market. While purely electric actuators are emerging, they often lack the sheer power density required for heavy lifting. Consequently, the industry is moving toward hybrid electro-hydraulic systems, which marry the high force capability of traditional hydraulics with the clean efficiency of electric powertrains. As eco-friendly bio-degradable hydraulic fluids gain mainstream traction alongside these hybrid systems, the mobile hydraulic equipment market is well-positioned to maintain its vital role in global industrial progress well into 2034 and beyond.

Related Reports-

Axial Piston Hydraulic Motors and Pumps Market

Hydraulic Torque Wrench Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

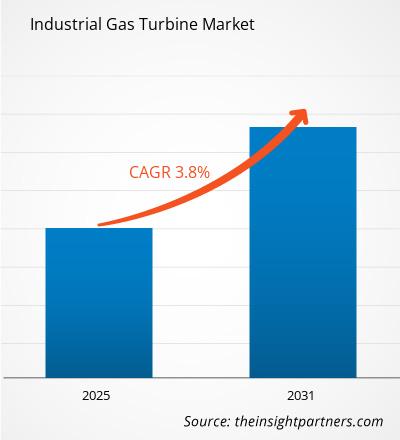

The global energy landscape is undergoing a massive transformation. As industries and governments work together to reduce carbon emissions while simultaneously meeting a soaring global demand for electricity, the underlying infrastructure must evolve. At the heart of this transition is the industrial gas turbine—a highly efficient internal combustion engine that converts natural gas or other liquid fuels into mechanical energy to drive electrical generators. Today, these systems are no longer just basic utilities; they are critical pillars supporting modern electrical grids, industrial operations, and decentralized energy hubs.

According to a comprehensive market study by The Insight Partners, the global Industrial Gas Turbine Market size is projected to reach US$ 13.54 billion by 2034 from US$ 9.96 billion in 2025. The market is anticipated to register a CAGR of 3.91% during the forecast period 2026-2034. This steady upward trajectory highlights a sustained reliance on gas-fired infrastructure as a primary bridging mechanism toward a more sustainable, low-carbon future.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

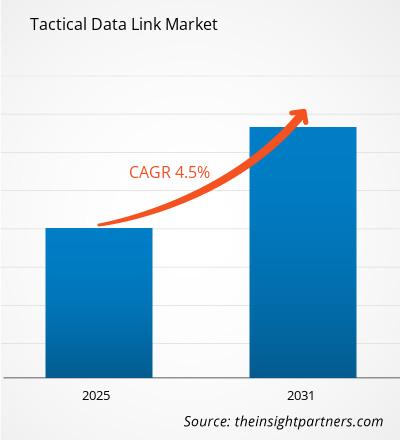

The modern defense landscape is rapidly shifting toward completely interconnected operations, where speed, precision, and information dominance determine mission success. At the very center of this evolution is the deployment of advanced communication systems capable of providing multi-domain situational awareness.

The global Tactical Data Link Market size is projected to reach US$ 13.76 billion by 2034 from US$ 9.26 billion in 2025. The market is anticipated to register a CAGR of 5.08% during the forecast period 2026-2034. This sustained financial growth reflects a systemic push by defense forces worldwide to replace legacy infrastructure with highly encrypted, jam-resistant, and high-speed data transmission networks.

Driving Factors Behind Market Expansion

The steady growth of the tactical data link (TDL) market is powered by several critical geopolitical and technological shifts. Chief among these is the widespread transition toward network-centric warfare (NCW). Rather than operating as isolated units, modern land, air, and sea assets are integrated into a singular unified digital environment. Tactical data links serve as the nervous system for this architecture, translating complex radar, sensor, and target data into real-time actionable insights for commanders on the ground and in the air.

Furthermore, escalating border disputes, rising regional conflicts, and geopolitical tensions across Europe, Asia-Pacific, and the Middle East have forced nations to rapidly scale up their defense expenditures. A significant portion of these updated budgets is funneling directly into electronic warfare (EW), command and control (C2) modernization, and Intelligence, Surveillance, and Reconnaissance (ISR) applications.

The rapid proliferation of unmanned platforms including Unmanned Aerial Vehicles (UAVs), autonomous marine vessels, and Unmanned Ground Vehicles (UGVs) has further amplified deployment needs. Because these platforms depend entirely on continuous, long-range communication lines for command, control, and sensory transmission, advanced links like Link 16 and Link 22 are becoming non-negotiable baselines for manufacturing procurement.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00006903

Market Segmentation and Technical Evolution

The market is generally broken down across three primary segments: component type, data link standard, and platform.

Components: While physical hardware like terminals, antennas, transceivers, and processors still commands a massive portion of historical revenue, the software segment is emerging as the fastest-growing area. Processing software allows disparate networks to talk to one another, driving better interoperability between distinct allied forces.

Data Link Standards: Link 16 remains the global military baseline, facilitating secure, high-speed jam-resistant communications across NATO and allied fleets. However, next-generation platforms are increasingly incorporating Link 22 to utilize superior Beyond Line-of-Sight (BLOS) communication channels over HF and UHF bands.

Platforms: Airborne systems continue to represent the largest operational market share due to the intense integration of TDLs in modern fighter jets, early warning aircraft, and military helicopters. Meanwhile, the land-based segment is experiencing a significant surge as individual soldier systems and mobile command centers undergo modernization overhauls.

Competitive Landscape

The global market features a highly competitive blend of tier-one defense contractors and specialized aerospace telecommunication firms. These market participants consistently target research and development (R&D) investments, multi-year government procurement programs, and strategic mergers to secure long-term contracts.

The following key players are driving technological innovation across the global tactical data link industry:

BAE Systems

Collins Aerospace

General Dynamics

Harris Corporation

L3 Technologies, Inc.

Leonardo DRS

Northrop Grumman

Raytheon Company

Saab AB

Viasat, Inc.

These players actively focus on engineering systems with strict Size, Weight, and Power (SWaP) constraints, ensuring that components can easily integrate into smaller platforms like compact drones or personal soldier communication packs without sacrificing security or range.

Future Outlook

Looking ahead, the future of the tactical data link market will be deeply intertwined with the deployment of cutting-edge civilian and military technologies. The integration of fifth-generation (5G) communication infrastructure into defense frameworks is expected to drastically lower network latency while substantially boosting overall bandwidth capacity. This allows massive sensor files, such as high-definition video feeds from aerial surveillance, to clear transmission barriers almost instantly.

Additionally, artificial intelligence (AI) and machine learning (ML) models are set to be integrated into processing software to automate data filtration, prioritizing critical threat notices over routine status transmissions to prevent cognitive overload for personnel. As cyber warfare capabilities grow more sophisticated globally, the market will naturally pivot toward zero-trust networking architectures and quantum-resistant encryption protocols. Over the next decade, tactical data links will evolve from basic message-relaying tools into completely cognitive, self-healing, multi-domain networks capable of securing information dominance in any combat zone.

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

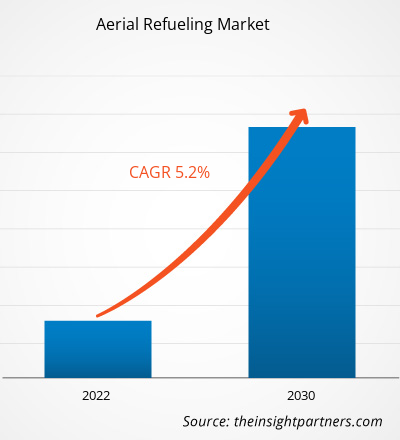

Core Drivers of the Aerial Refueling Market

The fundamental growth engine behind this market is the pressing need for extended combat endurance and non-stop global deployment capabilities. Aerial refueling, often referred to as in-flight refueling, removes the primary limitations of combat radius and payloadcapacity. Fighter jets, transport aircraft, and surveillance platforms can take off with lower fuel weights—allowing them to carry heavier payloads of munitions, specialized sensors, or personnel—and subsequently fuel up once airborne.

Geopolitical tensions across Western Europe, the Asia-Pacific region, and the Middle East have pushed defense ministries to transition from localized border protection models to highly integrated projection capabilities. Legacy tanker fleets built during the late Cold War era are facing severe fatigue, prompting massive military modernization initiatives. Nations are actively investing in new multi-role tanker transport (MRTT) systems that serve a dual purpose: acting as long-range tactical fuel supply points while retaining the internal capacity to handle cargo logistics and medical evacuations.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00006791

Technology Trends: Flying Boom vs. Probe and Drogue

The technological architecture of the market remains divided into two core deployment mechanisms, both of which are seeing substantial integration upgrades:

The Flying Boom System: This rigid, telescoping tube is controlled by an operator on the tanker aircraft and plugs into a receptacle on the receiver aircraft. It allows for exceptionally high fuel transfer rates, which is necessary for large bombers and heavy transport carriers.

The Probe and Drogue System: This flexible hose trailing a funnel-shaped basket requires the receiving pilot to fly a probe directly into the drogue. It is the preferred method for smaller tactical fighters, helicopters, and many naval aviation arms due to its simpler mechanical footprint and ability to refuel multiple aircraft simultaneously from wing-mounted pods.

The integration of advanced software, night-vision lighting, and automated boom control (ABC) is bridging the gap between these systems, reducing pilot workload and increasing safety margins during turbulent nighttime missions.

Key Industry Competitors

The complex engineering and stringent safety standards required for mid-air fuel transfers have concentrated the market among specialized aerospace and defense manufacturers. The prominent players driving innovation and scaling manufacturing capabilities across this landscape include:

Cobham Plc (Highly recognized for its specialized design and production of probe-and-drogue refueling buddy stores and wing-mounted pods)

Safran (A global leader providing critical high-end equipment, fuel systems management, and propulsion technologies)

Eaton (Supplies robust, highly engineered components including fuel valves, couplings, and sophisticated fluid management systems)

GE Aviation (Provides powerful propulsion systems and digital flight management avionics essential for heavy tanker stability)

Marshall Aerospace & Defense Group (Specializes in complex aircraft conversions, structural engineering, and fleet maintenance support)

Parker Hannifin Corporation (Delivers critical hydraulic and fluid conveyance solutions that ensure safe fuel distribution under immense pressure)

Israel Aerospace Industries Ltd (A pioneer in converting standard commercial airframes into capable multi-role military tanker platforms)

BAE Systems Plc (Integrates secure mission systems, electronic warfare protections, and advanced structures for military aviation)

Elbit Systems Ltd (Develops electro-optical pods, helmets, and training simulators designed to optimize refueling operator efficiency)

ARESIA (Engineers customized airborne mission equipment and refueling subsystem components tailored for modern tactical air forces)

Future Outlook

Looking down the runway, the future of the aerial refueling market will be shaped by autonomy and the integration of uncrewed aerial systems (UAS). As air forces invest heavily in collaborative combat aircraft (CCA) and stealth autonomous drones, the demand for unmanned-to-unmanned and manned-to-unmanned refueling systems will expand. Major defense contract competitions are already shifting focus toward developing autonomous "buddy refueling" capabilities, where an uncrewed carrier-based drone can refuel manned fighter wings, thereby preserving the life of large, high-value tanker assets by keeping them away from contested anti-access/area-denial (A2/AD) zones. Combined with artificial intelligence that predicts structural wear on refueling booms and automates precise alignment, the market is poised to evolve from a purely manual flight operation into an interconnected, software-defined node of modern tactical networks by 2030.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

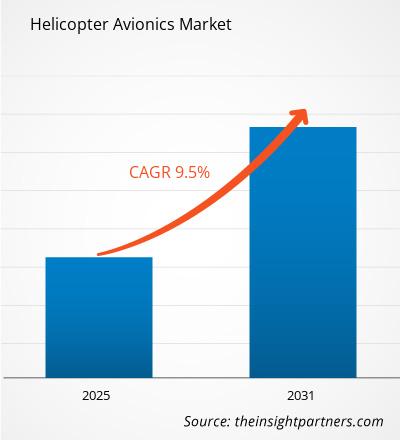

The aerospace industry is undergoing a profound digital transformation, and helicopter operations are at the forefront of this evolution. Modern mission profiles ranging from complex emergency medical services (EMS) and search and rescue (SAR) to offshore oil and gas transport and urban air mobility demand unprecedented levels of situational awareness, safety, and operational efficiency. At the heart of this capability is the helicopter avionics suite, an intricate network of electronic systems encompassing communication, navigation, flight control, and monitoring technologies.

According to a comprehensive market study by The Insight Partners, the global Helicopter Avionics Market size is projected to reach US$ 6.48 billion by 2034 from US$ 3.82 billion in 2025. This robust growth trajectory represents a steady Compound Annual Growth Rate (CAGR) of 6.04% during the forecast period from 2026 to 2034. This expansion is fueled by a combination of factors, including the modernization of aging military fleets, stringent safety regulations mandates by aviation authorities, and the rapid integration of commercial off-the-shelf (COTS) digital technologies into modern cockpits.

Key Market Drivers and Technological Dynamics

The sustained growth of the helicopter avionics sector is primarily driven by the urgent need to enhance pilot situational awareness, especially during low-visibility operations, adverse weather conditions, and low-altitude flights. Traditional analog instrument panels are rapidly being replaced by integrated glass cockpits featuring large-format multi-function displays (MFDs). These modern displays synthesize complex data from various sensors into intuitive visual formats, significantly reducing pilot workload and minimizing human error.

Furthermore, regulatory bodies worldwide such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) are continuously updating mandates regarding flight safety equipment. Requirements for advanced terrain awareness and warning systems (TAWS), automatic dependent surveillance-broadcast (ADS-B) transponders, and flight data monitoring systems are forcing fleet operators to opt for extensive retrofit programs. The commercial sector, particularly emergency medical and law enforcement aviation, is aggressively investing in these upgrades to ensure compliance and maximize operational safety.

In the military segment, geopolitical tensions are prompting defense forces to upgrade their rotary-wing assets. Modern military helicopter avionics must not only provide superior navigation and flight control but also integrate seamlessly with tactical data links, electronic warfare (EW) self-protection suites, and advanced weapon management systems. The demand for modular open systems architecture (MOSA) is growing rapidly in this space, allowing defense forces to swap and upgrade software components without overhauling entire hardware architectures.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00018715

Competitive Landscape and Industry Titan Innovations

The global market features a blend of established aerospace conglomerates and specialized software and hardware providers driving continuous innovation. The key players shaping the trajectory of the helicopter avionics market include:

Aspen Avionics, Inc. – Known for innovative, evolutionary cockpit upgrades, specializing in affordable, easy-to-install digital displays for general aviation and light helicopters.

Avidyne Corporation – A leader in integrated flight decks and multi-function displays, pushing boundaries in intuitive pilot-interface designs and navigation systems.

Collins Aerospace – A heavyweight in aviation technology, delivering highly reliable flight control, communication, and integrated mission systems for both commercial and military rotary-wing platforms.

Elbit Systems Ltd. – An international defense electronics provider renowned for cutting-edge helmet-mounted displays (HMDs) and enhanced vision systems (EVS) tailored for military operations.

ForeFlight LLC – A Boeing company that has revolutionized flight planning, mapping, and electronic flight bag (EFB) software, becoming an indispensable asset for modern digital cockpits.

Garmin Ltd. – A dominant force in flight deck retrofits and forward-fit solutions, continuously advancing safety features like helicopter electronic stability and protection (H-ESP) and terrain alerting.

Honeywell International Inc. – Provides highly sophisticated flight management systems, weather radars, and safety suites, driving the push toward autonomy and connected aircraft technologies.

L3Harris Technologies, Inc. – Specializes in mission-critical communications, night vision technologies, and flight data recorders built to survive rigorous mission parameters.

Leonardo S.p.A. – An aerospace giant that uniquely integrates custom, proprietary avionics architectures directly into its world-class manufacturing line of commercial and military helicopters.

Thales Group – A global leader in flight electronics, offering advanced flight management systems (FMS) and head-up displays (HUDs) designed to maximize safety in the most demanding environmental conditions.

Future Outlook

Looking ahead, the future of the helicopter avionics market will be defined by the convergence of artificial intelligence (AI), edge computing, and enhanced connectivity. As the industry transitions toward increasingly autonomous operations and prepares for the rise of eVTOL (electric vertical takeoff and landing) platforms, avionics suites will evolve from passive monitoring tools into proactive decision-support systems. AI-driven predictive maintenance systems will monitor component health in real time, dramatically reducing fleet downtime and operational costs. Moreover, the integration of 5G satellite connectivity and advanced data links will turn helicopters into highly connected nodes within a broader internet-of-military-things (IoMT) or commercial air traffic management ecosystem. Over the next decade, these software-defined architectures will enable seamless over-the-air updates, ensuring that helicopter fleets remain technologically relevant, safe, and efficient far into the future.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876