Blogs

In the vast and wonderful world of online games, there's a particular gem that has captured the hearts of music lovers everywhere: Heardle. If you’re a fan of a good challenge and enjoy testing your musical knowledge, Heardle is definitely a game you should explore. It’s simple, addictive, and a fantastic way to discover new tunes or rekindle old favorites.

What is Heardle?

At its core, Heardle is a musical guessing game. Each day, a new song is presented, and your task is to identify it based on short audio snippets. You get a series of attempts, with each attempt revealing a slightly longer segment of the song. The fewer attempts it takes you to guess correctly, the better your score! It's a delightful blend of trivia and memory, making it accessible to both casual listeners and seasoned music aficionados. If you haven't played before, you can jump right in and experience Heardle.

Gameplay: Your Daily Dose of Musical Mystery

Playing Heardle is incredibly straightforward. When you open the game, you'll see a play button and a search bar.

- Listen to the Snippet: Click the play button to hear the initial, very short, segment of the song. It might just be a single drum beat, a fleeting chord, or a snippet of an intro.

- Make Your Guess (or Skip): Based on what you hear, you can type your guess into the search bar. As you type, suggestions will appear, making it easier to find the correct artist and title. If you have absolutely no idea, don't worry! You can skip your turn by clicking the "Skip" button.

- Reveal More: Each incorrect guess or skip will reveal a slightly longer portion of the song. You'll get up to six attempts in total.

- The Big Reveal: Once you guess correctly or run out of attempts, the game will show you the full song title and artist. You can then listen to the entire track, which is a lovely touch.

Tips for Mastering Heardle

While the game is easy to pick up, a few strategies can help you improve your guessing game:

- Focus on the Intro: Often, the very first few notes or sounds of a song are its most distinctive. Pay close attention to these initial snippets.

- Think Genre and Era: If you can identify the genre or the approximate decade the song is from, it can significantly narrow down your search.

- Utilize the Search Bar: Don't be afraid to type in just an artist's name if you suspect you know who it is. The autofill feature is your friend!

- Don't Be Afraid to Skip: Sometimes, it’s better to skip an attempt if you’re completely stumped. That extra second or two of audio can make all the difference.

- Play Regularly: Like any skill, musical recognition improves with practice. The more you play Heardle, the better you’ll become at identifying songs quickly.

- Explore the Archives: Many Heardle sites allow you to play past days' songs. This is a great way to practice and expand your musical knowledge. For a free and accessible version, check out Heardle.

Conclusion

Heardle offers a daily dose of musical fun and a delightful challenge for anyone who enjoys music. It's a simple yet engaging game that can brighten your day and even introduce you to some fantastic new tunes. So, why not give it a try? Tune in, listen closely, and enjoy the thrill of the guess!

Did you know that nearly eighty percent of the links on the deep web become inactive within just a few months of their creation? Because the area of anonymous networking shifts so rapidly, static directories often lead users to dead ends. For those who rely on specific tools to navigate these layers, the speed at which a database updates is the difference between finding information and hitting a 404 error page. You might wonder if these systems work like the clear web engines you use daily or if they lag behind because of technical constraints.

Excavator functions as a specialized tool designed to crawl the Tor network. Compared to traditional engines that have massive server farms to constantly ping websites, onion based crawlers face unique challenges. The layers of encryption that protect user identity also slow down the process of verifying if a site is still online. When you enter a query, you are tapping into a stored index that represents a snapshot of the network at a specific point in time.

How Search Crawlers Explore Hidden Networks

The way an engine finds new content is through a process called crawling. It follows links from one page to another, cataloging the text and images it finds along the way. On the dark web, this is difficult because there is no central registry for domains. Many site owners prefer to stay hidden - they do not link to other platforms - this creates "dark islands" of content that are hard for even the best tools to find without a direct tip or a submission from the creator.

Many modern systems utilize a "spider" program that visits known addresses to see if they are active. If a site is offline for multiple consecutive checks, the system usually removes it from the visible results - this pruning is essential because of how often servers move or shut down. Users who want to understand the mechanics of the platforms often look at an overview of Tor network systems to see how indexing software manages such a volatile environment.

Effective crawling requires a balance of three main factors

- The speed of the server hosting the engine.

- The number of concurrent connections the spider can handle.

- The sensitivity of the dead link detection algorithm.

The Frequency of Database Refreshes

You will find that Excavator does not update every second like a global clear web engine might. It typically refreshes its core database in cycles. For high traffic areas, this might happen every twenty four to forty eight hours. For obscure corners of the network, a link might remain in the index for a week even if the source has disappeared - this delay is a trade off for the privacy and anonymity that the network provides.

Real-time updates are expensive in terms of bandwidth - Because Tor routes traffic through three different volunteer nodes, every "check" the search engine performs takes significantly longer than a standard internet request. If the engine tried to update everything at once, it would likely crash or face blocks from the network for behaving like a bot. The updates are staggered to keep the service stable for you and other users.

Manual Directories versus Automated Indexing

There are two primary ways you can find addresses - through automated engines or curated lists. Automated engines are great for finding specific keywords but they often include "junk" results or duplicate pages. Curated lists, on the other hand, are checked by humans. While they have fewer entries, the quality of the links is usually higher because a person has verified the content. Many people find a dark web directory helpful when they want categorized, reliable entry points rather than a massive list of unverified search hits.

Reliability varies between these two methods.

- Automated Engines

Best for wide reaching research and finding niche forums. - Manual Directories

Best for security, as editors often filter out malicious or broken mirrors. - Hybrid Systems

These use automation to check for "uptime" but allow users to report dead links.

If you are looking for specific types of adult content or entertainment, manual lists are often safer. As an example, finding a secure internet navigation guide for sensitive categories ensures you aren't clicking on "phishing" links that look like legitimate search results but are actually designed to steal your data.

Maintaining Safety During Your Search

Whenever you use a search tool on an anonymous network, you are responsible for your own security. The search engine can tell you a site exists but it cannot guarantee that the site is safe to visit to this day. Because updates are not instantaneous, a site that was "clean" yesterday could be compromised by the time you click it. Always use a dedicated, updated browser and keep your security settings on the highest level.

Check the URL carefully before entering any personal information. Many fake sites use "typosquatting" where they change one letter in a long onion address to trick you. If a search result seems suspicious or the description does not match the page content, it is better to skip it. Using a trusted privacy-focused browsing guide can help you learn the signs of a fake domain before you put your computer at risk.

Safety is a habit, not a single setting.

- Never download files from unverified search results.

- Disable JavaScript if you are visiting unknown domains.

- Use a secondary operating system if you are performing deep research.

FAQ

How can I tell if a search result is dead?

If the page takes more than thirty seconds to load or returns a "General SOCKS server failure" the site is likely offline. Because these sites run on private hardware, the owners might simply have their computers turned off at the moment.

Why do some links appear multiple times?

Many sites use "mirrors" which are exact copies of the same website hosted on different addresses - this helps the site stay online if one address is attacked or blocked. Engines often pick up all the different versions.

Can I submit my own link to be indexed?

Yes, most engines have a "Submit" or "Add URL" page - Once you submit a link, the spider will usually visit it within a few days to verify the content and add it to the public database.

Is the search history private?

Many reputable engines on the Tor network do not log your IP address or your search queries. You should always check the "About" or "Privacy" section of the specific tool you are using to be sure of their policy.

Introduction

The digital marketplace has transformed how businesses connect with customers. Whether operating in retail, healthcare, hospitality, real estate, or professional services, companies must establish a strong online presence to remain competitive. Consumers increasingly rely on search engines to discover products, compare services, and make purchasing decisions.

In such a competitive environment, working with a professional SEO company Dubai can provide businesses with the expertise and strategic direction needed to achieve sustainable growth. While many organizations recognize the importance of digital marketing, successful optimization requires specialized knowledge, consistent effort, and a deep understanding of search engine best practices.

By investing in professional SEO Dubai services, businesses can improve visibility, attract qualified visitors, and create a foundation for long-term success.

The Digital Shift in Consumer Behavior

Customers Begin Their Journey Online

Modern consumers rarely make purchasing decisions without conducting online research first. Search engines serve as the starting point for most buying journeys, allowing users to compare options and gather information before taking action.

Businesses that fail to appear in relevant search results risk losing valuable opportunities to competitors with stronger online visibility.

Online Visibility Influences Trust

Consumers often associate high-ranking websites with credibility and reliability. Appearing prominently in search results can positively influence customer perceptions and encourage engagement.

A strong digital presence helps businesses build trust before direct interactions even occur.

The Complexity of Search Optimization

More Than Just Keywords

Many business owners assume optimization revolves solely around adding keywords to website content. In reality, successful strategies involve multiple components working together.

These elements include:

- Technical website performance

- User experience

- Mobile responsiveness

- Content quality

- Internal linking

- Authority building

- Local optimization

Managing all these areas effectively requires specialized expertise.

Constant Algorithm Changes

Search engines frequently update their algorithms to improve user experiences and deliver more relevant results.

Businesses attempting to manage optimization independently often struggle to keep pace with these changes. Professional specialists monitor industry developments and adjust strategies accordingly.

Access to Industry Expertise

Knowledge Built Through Experience

A professional team brings years of practical experience working across various industries and market conditions.

This expertise allows them to:

- Identify opportunities quickly

- Avoid common mistakes

- Implement proven strategies

- Adapt to changing trends

Experience often translates into faster and more effective results.

Strategic Planning

Professional optimization involves much more than isolated tactics. It requires a comprehensive strategy aligned with business goals.

Experts develop customized plans based on:

- Industry competition

- Target audience behavior

- Market opportunities

- Business objectives

This strategic approach helps maximize return on investment.

Improved Search Visibility

Reaching the Right Audience

Visibility alone is not enough. Businesses need to attract visitors who are genuinely interested in their products or services.

Professional optimization focuses on connecting companies with users actively searching for relevant solutions.

Expanding Market Reach

Higher rankings increase exposure to potential customers across various stages of the purchasing journey.

As visibility grows, businesses gain more opportunities to generate inquiries, leads, and sales.

Enhanced Website Performance

Faster Loading Times

Website speed directly affects both user satisfaction and search rankings. Slow-loading websites can frustrate visitors and lead to higher abandonment rates.

Optimization specialists identify performance issues and implement solutions that improve speed and usability.

Mobile-Friendly Experiences

A large percentage of internet users access websites through smartphones and tablets.

Ensuring a seamless mobile experience helps businesses engage users effectively while meeting search engine requirements for mobile-first indexing.

High-Quality Content Development

Creating Valuable Resources

Content remains one of the most influential factors in online success. Businesses need content that informs, engages, and addresses customer needs.

Professional teams help create content that:

- Answers common questions

- Demonstrates expertise

- Supports customer decision-making

- Encourages engagement

Valuable content strengthens relationships with both users and search engines.

Building Topical Authority

Consistently publishing relevant content helps businesses establish authority within their industries.

When search engines recognize a website as a trusted source of information, rankings often improve across multiple related topics.

Better User Experience

Simplified Navigation

Visitors should be able to find information quickly and easily.

Professional optimization includes improving navigation structures, page layouts, and content organization to create intuitive user experiences.

Increased Engagement

A positive user experience encourages visitors to explore additional pages and spend more time interacting with content.

Higher engagement signals can contribute to stronger search performance over time.

Competitive Advantage

Standing Out in Crowded Markets

Competition continues to increase across nearly every industry. Businesses that neglect online optimization risk falling behind competitors that actively invest in their digital presence.

Professional support helps organizations maintain visibility and remain competitive.

Identifying Growth Opportunities

Experienced specialists conduct detailed competitor analyses to uncover opportunities for improvement.

These insights can reveal:

- Content gaps

- Keyword opportunities

- Audience interests

- Market trends

Leveraging these opportunities helps businesses strengthen their market position.

Stronger Local Presence

Connecting With Nearby Customers

For businesses serving specific geographic areas, local visibility plays a critical role in attracting customers.

Local optimization strategies improve visibility among users searching for nearby services and solutions.

Managing Business Listings

Accurate business information across online directories helps improve credibility and local search performance.

Professionals ensure consistency across platforms, reducing confusion and enhancing trust.

Data-Driven Decision Making

Measuring Performance

Successful optimization relies on accurate data and continuous analysis.

Professionals monitor key metrics such as:

- Traffic growth

- User behavior

- Conversion rates

- Search visibility

- Audience engagement

These insights help guide future improvements.

Continuous Refinement

Digital marketing is never static. Effective strategies evolve based on performance data and changing market conditions.

Regular analysis enables ongoing improvements that support long-term growth.

Cost-Effective Marketing Investment

Long-Term Value

Unlike short-term advertising campaigns, optimization efforts continue delivering benefits long after implementation.

Strong organic visibility can generate consistent traffic and leads without ongoing advertising expenses.

Improved Return on Investment

Because optimization targets users actively searching for products and services, it often produces highly qualified traffic.

This can lead to improved conversion rates and better overall marketing efficiency.

Supporting Business Growth

Generating Qualified Leads

Professional optimization helps attract visitors who are more likely to become customers.

Targeted traffic often results in higher-quality leads and increased sales opportunities.

Strengthening Brand Recognition

Consistent visibility across search results increases brand awareness and familiarity.

Over time, stronger recognition can influence purchasing decisions and customer loyalty.

Why Professional Support Matters

Saving Time and Resources

Managing optimization internally can be time-consuming and resource-intensive.

By partnering with a professional SEO company in Dubai, businesses can focus on core operations while experts handle technical and strategic responsibilities.

Access to Specialized Tools

Professionals utilize advanced software for research, analysis, tracking, and reporting.

These tools provide valuable insights that help identify opportunities and improve campaign effectiveness.

Future-Proofing Your Business

Adapting to Digital Trends

Technology and consumer behavior continue to evolve rapidly.

Businesses that invest in professional guidance are better positioned to adapt to emerging trends and maintain competitiveness.

Building Sustainable Success

Rather than relying on short-term tactics, professional optimization focuses on creating lasting value and long-term growth opportunities.

This sustainable approach supports continued success regardless of market changes.

Conclusion

A strong online presence is no longer optional for businesses seeking growth in today's competitive marketplace. From increasing visibility and improving website performance to generating qualified leads and strengthening brand authority, the benefits of professional optimization are substantial.

Working with a trusted SEO company in Dubai gives businesses access to expert knowledge, proven strategies, and advanced tools that support long-term success. Through comprehensive SEO Dubai solutions, organizations can enhance their digital presence, outperform competitors, and create a sustainable foundation for future growth.

As customer behavior continues to shift toward digital channels, investing in professional optimization remains one of the most effective ways to secure a competitive advantage and achieve lasting business success.

Aluminium 2026 is going to take place from 06 to 08 October 2026 at Messe Düsseldorf, Germany, and it will somehow bring together professionals from all over the world’s aluminium business. This event, which people usually see as one of the most important international trade fairs focused on aluminium production, processing, and application technologies, is like a key meeting point. Acknowledged as one of the leading international trade shows related to the technology associated with aluminium manufacturing, processing, and application, the fair acts as an ideal forum for manufacturers, suppliers, engineers, and decision makers. Since industries keep asking for lighter but tough materials, plus sustainable options, Aluminium 2026 gives a solid chance to look into innovations that are shaping tomorrow’s industrial manufacturing and metal processing worldwide.

A Comprehensive Showcase of Industry Solutions

The exhibition pretty much spans the full aluminium value chain, from raw material production and processing tech to the finished products and even the more advanced manufacturing solutions. The exhibitors demonstrate innovations in processes related to casting, extrusion, rolling, surface technology, recycling, machining, and automation, making it broad-ranging and not limited to a specific aspect. There will be exhibits by firms involved in significant industries such as automobiles, aerospace, construction, packaging, transport, electronics, and renewable energy. With that broad industry mix, Aluminium 2026 ends up being a good destination for companies that are after new suppliers, fresh technologies, and some serious commercial chances.

Building International Business Connections

One of the strongest advantages of Aluminium 2026 is how it can sort of link businesses from different regions and market spaces. The event pulls in a pretty global mix of buyers, procurement specialists, producers, and technical experts, all searching for dependable partners and fresh approaches. For the exhibitors, there’s also this direct back and forth with decision-makers, those people who actually steer buying plans and investment direction. And those in-person moments, they make room for alliances to grow, for expansion of business too, and for a more durable collaboration that runs across international markets.

Exploring the Trends Transforming the Aluminium Sector

The aluminium industry is going through big shifts right now, sustainability, energy efficiency, and tech advancement are basically becoming the main agenda. Aluminium 2026 gives a platform where companies can look into the newest progress, especially around recovery and recycling processes, low-carbon ways of making metal, digital manufacturing, and those smart factory technologies. For those individuals in the industry attending the exhibition, they will have context about trends in the market and regulatory changes, as well as possible new applications that will help guide their future growth. As such, companies are able to compete in a global market that becomes increasingly difficult each year.

Strengthening Brand Presence in a Competitive Industry

Joining Aluminium 2026 lets companies really show what they can do to a very focused group of industry people. The exhibition creates a solid place for showing products, pointing out technical competence, and also boosting brand visibility a lot more than you might expect. When firms exhibit together with top international manufacturers, plus suppliers, they can strengthen their market role and gain trust across the aluminium sector. It also draws real industry attention via professional networks, in person business meetings, and media coverage, so brand recognition keeps going past the exhibition floor.

Conclusion

Aluminium 2026 at Messe Düsseldorf will once again sort of serve as a leading international platform for the global aluminium industry. It attracts manufactures, technology providers, suppliers and buyers from all over the world and, at the same time, gives a chance to establish productive links, innovate and do business, which appears rather helpful. The event focuses on emerging technologies, sustainability programs and industry collaboration; thus, it turns out to be an indispensable event for businesses seeking to expand their presence in the market and identify new areas for development. For companies looking for means to expand their market presence and stay relevant, Aluminium 2026 offers just such an atmosphere.

Achieving a lean, muscular physique requires far more than simply reducing calorie intake. Successful bodybuilders understand that maintaining hard-earned muscle while eliminating excess body fat demands a strategic combination of nutrition, training, recovery, and supplementation. This is why many athletes and fitness enthusiasts choose to buy fat burners supplements as part of their transformation journey. When used responsibly alongside a well-structured fitness program, these supplements can support metabolism, energy production, and fat utilization, helping individuals move closer to their physique goals.

The growing popularity of fat loss supplements for bodybuilding stems from their ability to complement disciplined training routines. Whether preparing for a competition, enhancing muscle definition, or accelerating progress during a cutting phase, the right supplements can provide valuable support. However, understanding how these products work and selecting them wisely is essential for achieving safe and sustainable results.

Why Fat Burners Are Popular Among Bodybuilders

Bodybuilders often face the challenge of reducing body fat without sacrificing lean muscle mass. During calorie-restricted phases, the body may naturally break down muscle tissue for energy. This is where many athletes choose to buy fat burners supplements that are designed to support metabolic activity and improve energy expenditure.

Quality fat burners may help:

- Support thermogenesis and calorie burning

- Increase workout intensity and endurance

- Promote mental focus during training sessions

- Assist in maintaining lean muscle during cutting phases

- Enhance overall body composition when combined with proper nutrition

While supplements are not magic solutions, they can become effective tools when paired with consistency and discipline.

Common Fat Loss Supplements Used in Bodybuilding

Several advanced products are commonly discussed within the bodybuilding community for weight management and fat reduction. Some of the best and prescription fat loss supplements for bodybuilding or fat burners supplements are the following:

- Bitiron (T3 – Liothyronine 12.5mcg / T4 – Thyroxine 50mcg Mix)

- Clenbuterol Hydrochloride 40 mcg

- L-Carnibol (L-Carnitine HCl 2000mg/5ml)

- Saxenda 6 mg/ml Pen (Liraglutide)

- Levotiron (Levothyroxine Sodium) 100 mcg

- T4 – Levotiron (Levothyroxine Sodium) 150 mcg

- Tesofensine 500 mcg

Many individuals looking to buy fat burners supplements research these products because of their potential role in supporting metabolism, appetite control, or energy utilization. However, some of these compounds are prescription-based medications and should only be used under the supervision of a qualified healthcare professional.

How Fat Loss Supplements Support a Cutting Cycle

A successful cutting cycle focuses on reducing body fat while preserving muscle mass. High-quality fat loss supplements for bodybuilding may contribute to this goal by supporting metabolic efficiency and helping athletes maintain training intensity despite reduced calorie intake.

Certain ingredients can promote fat oxidation, while others may assist with appetite management or energy production. This added support often helps bodybuilders remain consistent with their nutrition plans and training programs during challenging fat-loss phases.

Individuals who buy fat burners supplements should remember that supplementation works best when combined with adequate protein intake, resistance training, hydration, and sufficient sleep.

Important Precautions and Possible Side Effects

Before using any supplement or weight-management product, understanding potential risks is essential. Certain fat-burning compounds may cause side effects, especially when used improperly or without medical supervision.

Possible side effects may include:

- Increased heart rate

- Elevated blood pressure

- Nervousness or anxiety

- Sleep disturbances

- Headaches

- Digestive discomfort

- Excessive sweating

- Thyroid-related complications when hormonal products are misused

Those with pre-existing medical conditions, cardiovascular concerns, thyroid disorders, or individuals taking prescription medications should consult a healthcare provider before deciding to buy fat burners supplements. Responsible usage and professional guidance are critical for both safety and effectiveness.

Choosing the Right Fat Loss Supplements for Bodybuilding

The supplement market offers countless options, making product selection an important decision. Effective fat loss supplements for bodybuilding should come from reputable suppliers that prioritize quality, transparency, and customer satisfaction.

When evaluating products, you must consider:

- Ingredient quality

- Manufacturing standards

- Brand reputation

- Product authenticity

- Customer reviews

- Professional recommendations

Rather than chasing quick fixes, focus on products that complement a comprehensive fitness strategy and support long-term results.

Buy Fat Burners Supplements in the USA from GenLabs

For athletes and fitness enthusiasts seeking reliable products, GenLabs has established itself as a trusted marketplace for bodybuilding and weight-management solutions. Whether you are looking to buy fat burners supplements or advanced fat loss supplements for bodybuilding, GenLabs offers a carefully selected range of products designed to support your fitness goals.

GenLabs is committed to providing authentic supplements, competitive pricing, and a seamless shopping experience for customers across the USA. In addition to offering premium bodybuilding products, the company provides attractive discounts that help fitness enthusiasts maximize value. You can receive 30% off on selected products by using the promotional code available on the GenLabs website.

With quality products, customer-focused service, and exceptional savings opportunities, GenLabs continues to be a preferred destination for individuals who want to buy fat burners supplements and pursue bodybuilding goals with confidence.

How AllAssignmentsPro Delivers Plagiarism-Free Assignment Help UK for Higher Grades

By assignmentjunkie, 2026-06-19

In today’s competitive academic environment, students across the United Kingdom face increasing pressure to submit high-quality assignments while managing lectures, part-time jobs, internships, and personal responsibilities. Universities expect students to demonstrate original thinking, critical analysis, and strong research skills in every assignment. However, meeting these expectations consistently can be challenging, especially when deadlines are tight and academic standards are high.

One of the biggest concerns students face is plagiarism. Universities in the UK have strict policies regarding academic integrity, and even unintentional plagiarism can result in penalties, reduced grades, or disciplinary action. This is why students seek professional academic support that guarantees originality and quality. AllAssignmentsPro has established itself as a trusted provider of plagiarism-free assignment help UK services, helping students achieve better grades while maintaining academic integrity.

This blog explores how AllAssignmentsPro ensures originality in every assignment and supports students in achieving academic success.

Understanding the Importance of Plagiarism-Free Assignments

Plagiarism occurs when someone presents another person's ideas, words, or work as their own without proper acknowledgment. In UK universities, plagiarism is considered a serious academic offense. Educational institutions use advanced plagiarism detection tools to identify copied content, making it essential for students to submit completely original work.

Submitting plagiarism-free assignments offers several benefits:

- Demonstrates genuine understanding of the subject.

- Enhances academic credibility.

- Improves critical thinking and analytical skills.

- Helps students earn higher grades.

- Prevents academic penalties and disciplinary actions.

Because originality is a key component of academic success, students need reliable support from experts who understand university standards and academic writing requirements.

Why Students Choose AllAssignmentsPro for Assignment Help UK

AllAssignmentsPro has built a strong reputation for delivering high-quality academic assistance to students across various disciplines. Whether students require help with essays, reports, case studies, dissertations, research papers, or coursework, the platform focuses on producing original and customized content.

Students choose AllAssignmentsPro because of its commitment to:

- Academic integrity

- Subject expertise

- Timely delivery

- Customized solutions

- Affordable pricing

- Quality assurance

By combining these elements, AllAssignmentsPro helps students submit assignments that meet university expectations and contribute to improved academic performance.

Customized Assignments Written from Scratch

One of the primary ways AllAssignmentsPro ensures plagiarism-free content is by creating every assignment from scratch.

Unlike generic writing services that rely on pre-written templates or recycled content, AllAssignmentsPro assigns each project to a qualified academic expert who develops the assignment based on the student's specific requirements.

The process includes:

- Understanding assignment instructions carefully.

- Reviewing marking criteria.

- Conducting independent research.

- Creating unique arguments and analyses.

- Writing original content tailored to the topic.

This personalized approach ensures that every assignment is unique and aligned with the student's academic objectives.

Expert Writers with Strong Academic Backgrounds

The quality of academic writing largely depends on the expertise of the writer. AllAssignmentsPro employs experienced professionals who possess advanced qualifications in their respective fields.

These experts have extensive knowledge in subjects such as:

- Business and Management

- Marketing

- Accounting and Finance

- Human Resource Management

- Nursing and Healthcare

- Engineering

- Information Technology

- Law

- Psychology

- Education

- Economics

Because these writers understand subject-specific concepts and university expectations, they can produce well-researched and original assignments that demonstrate academic excellence.

Comprehensive Research for Original Content

Research is the foundation of any successful academic assignment. AllAssignmentsPro emphasizes thorough research to ensure originality and credibility.

Writers use reliable academic sources, including:

- Peer-reviewed journals

- Academic databases

- Government publications

- Industry reports

- Scholarly articles

- University resources

Rather than copying information from existing sources, experts analyze, interpret, and present information in their own words. This approach not only eliminates plagiarism but also strengthens the quality of the assignment.

Comprehensive research helps students present well-supported arguments and achieve higher grades.

Proper Referencing and Citation Practices

Incorrect referencing is one of the most common causes of accidental plagiarism among students. Many students struggle with citation styles and referencing requirements, leading to unintentional academic misconduct.

AllAssignmentsPro addresses this issue by ensuring proper citation and referencing throughout every assignment.

Experts are proficient in various referencing styles, including:

- Harvard Referencing

- APA Style

- MLA Style

- Chicago Style

- OSCOLA Referencing

- IEEE Referencing

Accurate citations acknowledge original authors and demonstrate academic integrity. Proper referencing also enhances the credibility and professionalism of academic work.

Advanced Plagiarism Checking Procedures

To maintain the highest standards of originality, AllAssignmentsPro utilizes advanced plagiarism detection processes before delivering assignments to students.

Each assignment undergoes a thorough review to identify any similarities with existing content. This quality assurance step helps ensure that the final document is completely unique and ready for submission.

The plagiarism-checking process helps:

- Detect accidental duplication.

- Verify originality.

- Improve content quality.

- Ensure compliance with university guidelines.

As a result, students receive assignments that meet strict academic standards and provide confidence during submission.

Quality Assurance and Multiple Review Stages

Delivering plagiarism-free assignments requires more than simply writing original content. AllAssignmentsPro follows a comprehensive quality assurance process that includes multiple review stages.

The review process typically covers:

- Grammar and spelling checks

- Structural consistency

- Citation accuracy

- Content originality

- Logical flow of arguments

- Compliance with assignment requirements

Editors carefully evaluate each assignment before delivery to ensure it meets academic expectations. This attention to detail contributes to better grades and improved learning outcomes.

Tailored Solutions for Different Academic Levels

Different academic levels require different writing approaches. An undergraduate essay differs significantly from a postgraduate dissertation or research project.

AllAssignmentsPro understands these distinctions and tailors assignments according to the student's academic level.

The service supports:

Undergraduate Students

Assignments focus on foundational concepts, structured analysis, and clear explanations.

Postgraduate Students

Content includes advanced research, critical evaluation, and sophisticated arguments.

Research Scholars

Assignments emphasize originality, comprehensive literature reviews, and evidence-based analysis.

This customized approach ensures that students receive work appropriate for their educational level and grading criteria.

Timely Delivery Without Compromising Quality

Meeting deadlines is critical for academic success. Late submissions can result in grade reductions or missed opportunities.

AllAssignmentsPro prioritizes timely delivery while maintaining originality and quality. Experienced writers follow structured workflows that allow them to complete assignments efficiently without relying on copied content.

Students benefit from:

- On-time submissions

- Adequate revision opportunities

- Reduced academic stress

- Improved time management

Timely delivery ensures students can review assignments before submission and make any necessary adjustments.

Supporting Better Academic Performance

The ultimate goal of plagiarism-free assignment help is not just avoiding penalties but helping students achieve higher grades.

Assignments from AllAssignmentsPro contribute to academic success by:

- Demonstrating strong subject knowledge.

- Presenting clear and logical arguments.

- Using credible academic sources.

- Maintaining proper formatting and referencing.

- Meeting university assessment criteria.

High-quality assignments often receive better evaluations from professors, leading to improved academic outcomes and greater confidence among students.

Ethical Academic Assistance

AllAssignmentsPro believes in supporting students responsibly. The service is designed to provide educational guidance, research assistance, and writing support that helps students better understand academic concepts and requirements.

By offering customized and original solutions, the platform encourages learning while maintaining academic integrity.

Students can use the provided materials as valuable references to improve their own writing, research, and analytical skills.

Conclusion

In an academic environment where originality is essential, students need trustworthy support that prioritizes quality and integrity. AllAssignmentsPro has become a reliable provider of plagiarism-free assignment help UK by combining expert writers, comprehensive research, proper referencing, rigorous quality checks, and personalized academic assistance.

Every assignment is written from scratch, carefully reviewed, and tailored to meet university standards. This commitment to originality not only protects students from plagiarism-related issues but also enhances their chances of achieving higher grades.

Whether you need assistance with essays, reports, dissertations, coursework, or research projects, AllAssignmentsPro provides the professional support necessary to excel academically. By choosing a service dedicated to plagiarism-free content and academic excellence, students can confidently submit high-quality assignments and move closer to their educational goals.

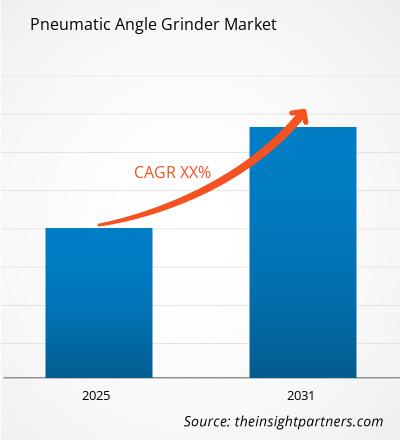

North America Pneumatic Angle Grinder Market Analysis and Manufacturing Demand Forecast 2034

By sammkaran, 2026-06-19

The industrial landscape is constantly evolving, driven by the demand for tools that offer high efficiency, durability, and safety. Among these, the pneumatic angle grinder has emerged as a fundamental tool across manufacturing, construction, and metalworking environments. Powered by compressed air rather than electric motors, these tools are highly valued for their ability to deliver consistent power without the risk of electrical overheating or sparking in volatile atmospheres.

According to a comprehensive study by The Insight Partners, the global Pneumatic Angle Grinder Market size is projected to reach US$ 1.8 Billion by 2034 from US$ 1.06 Billion in 2025. The market is anticipated to register a CAGR (compound annual growth rate) of 5.9% during the forecast period 2026–2034. This steady expansion underscores the growing reliance on robust air-powered tools in heavy-duty industrial operations worldwide.

Market Dynamics and Growth Drivers

Several key factors are propelling the global pneumatic angle grinder market forward. First and foremost is the rapid expansion of the manufacturing, automotive, and aerospace industries. In these sectors, surface preparation, metal finishing, weld grinding, and cutting are daily, high-volume tasks. Pneumatic angle grinders offer a superior power-to-weight ratio compared to their electric or battery-powered counterparts. This means operators can work with lightweight tools that reduce fatigue while still generating immense speed and torque to cut through hardened materials.

Safety regulations in heavy industries also play a vital role. In environments such as oil and gas refineries, chemical processing plants, and shipyards, the presence of flammable gases or moisture poses a severe risk for electric tools, which can emit sparks or short-circuit. Pneumatic tools naturally eliminate these electrical hazards because they rely entirely on mechanical air pressure. Additionally, since air motors cannot burn out from overloading they simply stall without damage when pushed beyond capacity they boast a significantly longer operational lifespan, reducing long-term maintenance costs for industrial facilities.

Furthermore, the rise of infrastructure projects across developing economies in the Asia-Pacific region, Latin America, and parts of Africa is creating a substantial demand for reliable construction tools. As governments invest in railways, bridges, pipelines, and commercial buildings, heavy fabrication activities increase, directly feeding the demand for pneumatic grinding machinery.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00023232

Competitive Landscape and Key Players

The global market features a blend of established multinational manufacturers and specialized regional players focusing on precision engineering and durable components. Companies are continuously investing in research and development to improve ergonomics, lower vibration levels, and integrate advanced noise-reduction systems to safeguard workers.

The key players operating in the global pneumatic angle grinder market include:

-

Robert Bosch Power Tools GmbH: A global leader in engineering and technology, providing high-performance industrial tools with a strong emphasis on precision and safety.

-

Bhagwati Tools Private Limited: A well-known manufacturer specializing in rugged, reliable pneumatic equipment designed for demanding metalworking environments.

-

Chicago Pneumatic: Renowned worldwide for high-quality air compressors and pneumatic tools, delivering heavy-duty performance across the automotive and construction sectors.

-

Rodcraft: A brand built on innovative compressed air tools and workshop equipment, focusing on user-friendly designs and durability.

-

Sumake Industrial Co., Ltd.: An international manufacturer specializing in professional high-end pneumatic tools, compressor options, and associated accessories.

-

GISON MACHINERY CO., LTD.: A premier manufacturer based in Taiwan, offering a diverse portfolio of air tools with decades of manufacturing experience.

-

RUKO GmbH Präzisionswerkzeuge: Celebrated for its high-precision drilling and cutting tools, catering to precise metal craftsmen and industrial operations.

-

Ralliwolf: An established name in the power tool space, known for manufacturing resilient industrial gear tailored for tough site conditions.

-

TORA KING: A specialized provider of industrial-grade tools designed for efficient material removal and consistent workshop throughput.

-

Associated Pneumatic Tools: A key supplier of specialized pneumatic solutions focused on reliability, performance, and heavy-duty capabilities.

Market Segmentation and Regional Highlights

The market can be segmented based on product type, disc size, and end-use industry. In terms of disc size, standard 4-inch and 5-inch grinders hold a substantial share due to their versatility in common fabrication tasks. However, larger heavy-duty models designed for 7-inch to 9-inch discs are seeing increased adoption in large-scale shipbuilding and heavy structural steel fabrication.

Geographically, North America and Europe remain mature, highly technical markets. These regions are characterized by stringent workplace safety standards (such as OSHA guidelines), forcing companies to adopt sparks-free pneumatic systems over electric alternatives. On the other hand, the Asia-Pacific region is recognized as the fastest-growing market. Rapid urbanization, massive industrialization in countries like India and China, and the expansion of automotive manufacturing facilities are major catalysts for market growth in this part of the world.

Future Outlook

The future of the pneumatic angle grinder market is closely tied to the themes of ergonomics, energy efficiency, and industrial automation. Moving forward, manufacturers are expected to focus heavily on lightweight composite materials to minimize tool weight, alongside advanced internal dampening systems that drastically reduce hand-arm vibration (HAV) syndromes in operators. Additionally, as industrial facilities look to optimize their carbon footprints, air compressor technology is becoming more energy-efficient, indirectly reducing the cost of running pneumatic tool networks. We are also likely to see a closer integration of pneumatic grinding heads onto robotic arms for automated deburring and finishing systems, paving the way for pneumatic power to stay highly relevant in the era of smart manufacturing and Industry 4.0.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

Medical Smart Textile Market Witnesses Growth Driven by Wearable Healthcare Innovations

By komal234, 2026-06-19

According to the latest report published by Data Bridge Market Research, the Medical Smart Textile Market

CAGR Value

The universal Medical Smart Textile Market report has explained in-depth market insights about market size, latest trends, market threats and key drivers driving the market. This market research report also supports to secure economies in the distribution of products and find out the best way of approaching the potential. This report deeply attempts to determine the impact of buyers, substitutes, new entrants, competitors, and suppliers on the market. The wide ranging Medical Smart Textile Market analysis report is evaluated mainly on two segments namely types and applications which cover all the analytical data for current and future markets.

Stay informed with our latest keyword market research covering strategies, innovations, and forecasts. Download full report: https://www.databridgemarketresearch.com/reports/global-medical-smart-textile-market

Medical Smart Textile Market Segmentation and Market Companies

Segments

- Based on product type, the medical smart textile market can be segmented into garments, braces, bandages, implants, and others. Garments segment is expected to dominate the market due to the increasing adoption of smart textiles in healthcare to monitor vital signs, body movements, and other health parameters. These garments offer comfort and mobility while providing real-time health monitoring.

- By application, the market can be segmented into patient monitoring, therapy, diagnostics, and others. The patient monitoring segment is anticipated to lead the market as smart textiles enable continuous monitoring of patients without additional wires or devices. This real-time monitoring helps healthcare professionals in providing better care to patients.

- On the basis of end-user, the market can be segmented into hospitals and clinics, home healthcare, fitness and wellness centers, and others. The hospitals and clinics segment is expected to hold the largest share as smart textiles are extensively used in hospital settings for patient monitoring, rehabilitation, and post-operative care.

Market Players

- Sensoria Inc.

- AIQ Smart Clothing

- Vista Medical Ltd.

- Schoeller Switzerland

- Noble Biomaterials, Inc.

- Directa Plus S.p.A.

- Gentherm

- Sensoria Fitness

- ThermoSoft International Corporation

- Textronics, Inc.

The global medical smart textile market is witnessing significant growth due to advancements in wearable technology, increasing prevalence of chronic diseases, and growing awareness about personal health management. The integration of sensors and connectivity technologies in textiles has revolutionized healthcare by enabling continuous monitoring of patients' health parameters. Companies like Sensoria Inc., AIQ Smart Clothing, and Vista Medical Ltd. are at the forefront of developing innovative medical smart textiles. These market players are investing in research and development to introduce new products that offer enhanced functionality and comfort to users. The medical smart textile market is expected to continue its growth trajectory in the coming years as the demand for remote patient monitoring and personalized healthcare solutions rises globally.

The global medical smart textile market is poised for remarkable growth in the upcoming years, driven by a multitude of factors shaping the healthcare and textile industries. One of the key trends revolutionizing the market is the increasing adoption of smart textiles in healthcare applications. These innovative textiles have the capability to monitor vital signs, track body movements, and offer real-time health insights, thereby enhancing patient care and management. The market players mentioned in the segments are actively engaged in developing cutting-edge solutions that cater to the evolving needs of medical professionals and patients alike.

Advancements in wearable technology have played a pivotal role in propelling the growth of the medical smart textile market. The integration of sensors and connectivity technologies into textiles has paved the way for seamless patient monitoring and personalized healthcare solutions. Companies such as Sensoria Inc., AIQ Smart Clothing, and Vista Medical Ltd. are leading the charge in developing next-generation smart textiles that offer advanced functionalities and improved user experience. These market players are heavily investing in research and development to bring forth innovative products that meet the stringent requirements of the healthcare sector.

Moreover, the rising prevalence of chronic diseases worldwide has further accelerated the demand for medical smart textiles. These textiles play a crucial role in the early detection and management of chronic conditions by providing continuous health monitoring and timely interventions. The ability of smart textiles to offer comfort, mobility, and real-time health insights makes them invaluable tools in improving patient outcomes and reducing healthcare costs. With the shift towards remote patient monitoring and telehealth services gaining traction globally, the medical smart textile market is expected to witness sustained growth in the foreseeable future.

In addition, the increasing emphasis on personalized health management is driving the adoption of smart textiles in various healthcare settings. Hospitals, clinics, home healthcare providers, and fitness centers are leveraging the benefits of smart textiles to enhance patient care, rehabilitation programs, and post-operative monitoring. These textiles not only improve the efficiency of healthcare delivery but also empower individuals to take charge of their health and well-being. As consumers become more health-conscious and tech-savvy, the demand for medical smart textiles is projected to escalate, creating lucrative opportunities for market players to innovate and expand their product offerings.

In conclusion, the global medical smart textile market is experiencing robust growth fueled by technological advancements, changing healthcare dynamics, and evolving consumer preferences. Market players are well-positioned to capitalize on this burgeoning market by developing innovative solutions that cater to the diverse needs of healthcare professionals and individuals seeking proactive health management. With a strong focus on research, product development, and strategic partnerships, the medical smart textile market is poised to witness sustained growth and continued innovation in the coming years.The global medical smart textile market continues to witness significant growth as a result of the increasing integration of smart textiles in healthcare applications. These innovative textiles are transforming patient care by offering real-time health monitoring, enhancing comfort, and enabling seamless data collection. Market players such as Sensoria Inc., AIQ Smart Clothing, and Vista Medical Ltd. are pioneering the development of cutting-edge medical smart textiles to meet the evolving demands of healthcare professionals and patients. The convergence of wearable technology with healthcare solutions has opened up new avenues for remote patient monitoring, personalized health management, and improved healthcare outcomes.

Moreover, the escalating prevalence of chronic diseases globally is driving the demand for medical smart textiles that enable early detection, continuous monitoring, and timely interventions. These textiles play a pivotal role in improving patient outcomes, reducing healthcare costs, and empowering individuals to proactively manage their health. With the increasing focus on personalized healthcare and wellness management, smart textiles are increasingly being adopted across various healthcare settings including hospitals, clinics, home healthcare, and fitness centers. The versatility of smart textiles in providing vital health insights, enhancing mobility, and optimizing patient care workflows is positioning them as indispensable tools in the healthcare industry.

Furthermore, as consumers become more health-conscious and technology-savvy, the demand for medical smart textiles is anticipated to surge in the foreseeable future. The market's growth trajectory is expected to be driven by advancements in sensor technologies, data analytics, and material science, leading to the development of more sophisticated and user-friendly smart textile solutions. Market players are investing heavily in research and development to introduce innovative products that offer enhanced functionality, improved user experience, and greater compatibility with existing healthcare systems. The collaborative efforts between technology companies, textile manufacturers, and healthcare providers are set to propel the medical smart textile market into a new era of healthcare innovation and patient-centered care.

In conclusion, the global medical smart textile market is poised for substantial growth fueled by the convergence of textile innovation, healthcare technology, and consumer-driven healthcare trends. Market players are well-positioned to capitalize on the expanding market opportunities by focusing on product differentiation, strategic partnerships, and customer-centric solutions. The transformative potential of medical smart textiles in revolutionizing patient care, improving healthcare delivery, and empowering individuals to actively engage in their health journey underscores the significant role these textiles will play in shaping the future of healthcare.

Frequently Asked Questions About This Report

What will be the most lucrative part of the Medical Smart Textile Market value chain in 2033?

What are the legal barriers to entry in the Medical Smart Textile Market?

How does the Adopter Category (Innovators vs. Laggards) look for Medical Smart Textile Market?

How are Green regulations changing the Medical Smart Textile Market?

How much revenue did the ground/minced products segment generate in 2025?

How are top players using M&A to secure their value chain?

Which region has the highest adoption rate of Medical Smart Textile Market technology?

How is the Medical Smart Textile Market responding to Consolidation?

What is the impact of the Blue Economy on Medical Smart Textile Market trends?

What is the impact of Natural Disasters on Medical Smart Textile Market production hubs?

How is the shift toward sustainability driving Medical Smart Textile Market trends?

What is the Overall Equipment Effectiveness (OEE) in the Medical Smart Textile Market industry?

What is the growth potential of the within the Medical Smart Textile Market?

Browse More Reports:

Europe Web Hosting Services Market

Asia Pacific Biochar Market

North America Biochar Market

Malaysia Metal Roofing Market

Global Customer Data Management Market

Global Mobile C-Arm Equipment Market

Global Automotive Refinish Coatings Market

Global Point of Care Diagnostics Market

Global Neurovascular Stents Market

Global Osteoarthritic Pain Management Treatment Market

Global Pass-By Noise Testing Market

Global Cashew Milk Market

Global Aerosol Propellant Market

Global Agrigenomics Market

Global Aluminium-extruded Products Market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 995

Email:- corporatesales@databridgemarketresearch.com"

Health Simulation Software Market Accelerates Through Digital Healthcare Training Solutions

By komal234, 2026-06-19

According to the latest report published by Data Bridge Market Research, the Health/Medical Simulation Software Market

CAGR Value

The persuasive Health/Medical Simulation Software Market report covers several topics including market trend analysis, market drivers, market restraints, opportunities, threats, application analysis, emerging markets, and futuristic market scenario. Moreover, it analyses Health/Medical Simulation Software Market industry by product type, by equipment type, by price category e.g. discount, mainstream, or premium etc., by distribution channel, by application and by geography. All the numerical data included in the report is backed up by excellent tools such as SWOT analysis, Porter's Five Forces Analysis and others. Analytical study of Health/Medical Simulation Software Market document helps in mapping growth strategies to increase sales and build brand image in the market.

Stay informed with our latest keyword market research covering strategies, innovations, and forecasts. Download full report: https://www.databridgemarketresearch.com/reports/global-health-medical-simulation-software-market

Health/Medical Simulation Software Market Segmentation and Market Companies

Segments

- Based on component, the global health/medical simulation software market can be segmented into software and services. The software segment is anticipated to dominate the market due to the increasing demand for advanced simulation solutions to enhance medical training and patient safety. Additionally, the services segment is expected to witness significant growth as healthcare institutions increasingly opt for simulation software services to improve operational efficiency and performance.

- On the basis of application, the market can be categorized into training, education, patient simulation, and others. The training segment is projected to hold a substantial market share as healthcare professionals and students utilize simulation software for hands-on learning and skill development. The patient simulation segment is also expected to experience rapid growth as the need for realistic patient scenarios for practice and assessment rises.

- By end-user, the global health/medical simulation software market can be segmented into hospitals, academic institutions, and others. Hospitals are expected to be the largest end-users of simulation software, driven by the growing focus on patient safety and quality of care. Academic institutions are also likely to contribute significantly to market growth as they incorporate simulation technology into medical education curriculum.

Market Players

- Some of the key players in the global health/medical simulation software market include Laerdal Medical; CAE Healthcare; 3D Systems, Inc.; Simulab Corporation; Mentice AB; Kyoto Kagaku Co., Ltd.; Simbionix USA Corporation; Limbs & Things; and Simulaids, Inc. These companies are actively involved in product development, strategic collaborations, and acquisitions to strengthen their market position and meet the evolving needs of healthcare professionals.

- Other notable players in the market are Gaumard Scientific, Surgical Science Sweden AB, IngMar Medical, OSSimTech, and Medical-X. These companies are focusing on innovative simulation solutions, such as virtual reality and augmented reality-based platforms, to enhance the effectiveness of medical training and improve patient outcomes.

For more detailed market insights and analysis, visit: The global health/medical simulation software market is witnessing significant growth driven by various factors such as the increasing demand for advanced simulation solutions to enhance medical training, improve patient safety, and optimize operational efficiency in healthcare settings. The market segmentation based on components into software and services showcases the dominance of the software segment owing to the need for sophisticated simulation tools among healthcare professionals. Software providers are focusing on developing innovative solutions that offer realistic and immersive simulation experiences to cater to the evolving training needs of medical practitioners and students. On the other hand, the services segment is gaining traction as healthcare institutions look for comprehensive simulation software services to streamline their operations and enhance overall performance.

In terms of application segmentation, the emphasis on training, education, patient simulation, and other use cases underscores the diverse applications of health/medical simulation software across the healthcare ecosystem. The training segment stands out as a key driver of market growth, with healthcare professionals leveraging simulation software for hands-on training and skill enhancement. Moreover, the patient simulation segment is poised for rapid expansion, driven by the increasing emphasis on realistic patient scenarios for practice and assessment, leading to improved clinical outcomes and enhanced patient care quality.

When analyzing the market from an end-user perspective, hospitals emerge as the largest consumers of health/medical simulation software due to their focus on enhancing patient safety and care quality through advanced training methodologies. Academic institutions also play a crucial role in driving market growth as they integrate simulation technology into medical education programs to better prepare students for real-world healthcare challenges. The adoption of simulation software in healthcare settings is expected to continue rising, driven by the proven benefits of simulation-based training in improving clinical skills, patient outcomes, and overall healthcare delivery.

Key players in the global health/medical simulation software market, such as Laerdal Medical, CAE Healthcare, and 3D Systems, Inc., are actively engaged in product innovation, strategic partnerships, and acquisitions to strengthen their market presence and cater to the evolving needs of healthcare providers. The focus on developing advanced simulation solutions, including virtual reality and augmented reality platforms, reflects the industry's commitment to enhancing medical training effectiveness and driving positive patient outcomes. As the market continues to evolve, collaboration between software developers, healthcare institutions, and technology providers will be crucial in shaping the future of health/medical simulation software solutions and driving innovation in the healthcare industry.The global health/medical simulation software market is witnessing substantial growth propelled by the surging demand for cutting-edge simulation solutions in the healthcare sector. This increased demand is fueled by the need to enhance medical training, elevate patient safety standards, and optimize operational efficiency within healthcare facilities. The market segmentation based on components into software and services highlights the dominance of the software segment, as healthcare professionals seek more sophisticated simulation tools to enrich their training practices. Software providers are focusing on developing innovative solutions that offer realistic and immersive simulation experiences to cater to the evolving needs of medical practitioners and students. Concurrently, the services segment is gaining momentum as healthcare institutions strive for comprehensive simulation software services to streamline their operations and boost overall performance.

When analyzing the market from the perspective of applications, the emphasis on training, education, patient simulation, and other utility scenarios underscores the diverse applications of health/medical simulation software across the healthcare landscape. The training segment emerges as a key driver of market expansion, with healthcare professionals leveraging simulation software for practical training and skills enhancement. Furthermore, the patient simulation segment is poised for rapid growth, driven by the increasing need for realistic patient scenarios for practice and assessment, ultimately leading to improved clinical outcomes and enhanced patient care quality.

From an end-user viewpoint, hospitals emerge as the primary consumers of health/medical simulation software due to their unwavering commitment to enhancing patient safety and care quality through advanced training methodologies. Academic institutions also play a vital role in propelling market growth as they integrate simulation technology into medical education programs to better equip students for real-world healthcare challenges. The adoption of simulation software in healthcare settings is expected to continue its upward trajectory, supported by the proven benefits of simulation-based training in enhancing clinical skills, patient outcomes, and overall healthcare delivery.

Key industry players such as Laerdal Medical, CAE Healthcare, and 3D Systems, Inc., are actively involved in product innovation, strategic partnerships, and acquisitions to fortify their market presence and address the evolving needs of healthcare providers. The focus on developing advanced simulation solutions, including virtual reality and augmented reality platforms, underscores the industry's commitment to boosting medical training effectiveness and driving positive patient outcomes. As the market evolves, collaboration among software developers, healthcare institutions, and technology providers will be pivotal in shaping the future of health/medical simulation software solutions and driving innovation in the healthcare industry.

Frequently Asked Questions About This Report

How much do the top 10 players contribute to the overall Health/Medical Simulation Software Market share?

What are the dominant pricing models in the Health/Medical Simulation Software Market (Fixed vs. Dynamic)?

How is the supply chain of the Health/Medical Simulation Software Market being optimized?

How do Ethical Concerns affect consumer sentiment in the Health/Medical Simulation Software Market?

What is the projected CAGR for the Health/Medical Simulation Software Market in South East Asia?

How is vendor selection criteria changing in the Health/Medical Simulation Software Market?

What is the valuation of the Health/Medical Simulation Software Market excluding the [Region] market?

What is the projected value of the Health/Medical Simulation Software Market by 2033 based on current tech trends?

What is the average order value (AOV) in the Health/Medical Simulation Software Market industry?

What is the revenue split between different tiers of players in the Health/Medical Simulation Software Market?

What is the impact of Self-Service models on Health/Medical Simulation Software Market demand?

Who are the major raw material suppliers in the Health/Medical Simulation Software Market?

Browse More Reports:

Middle East and Africa Electrostatic Precipitator Market

North America Food Storage Container Market

Middle East and Africa Electrical Steel Market

North America Electrical Steel Market

Europe Airless Dispenser Market

Europe Microalgae Market

North America Popping Boba Juice Balls Market

Asia-Pacific Botanical Extract Market

Middle East and Africa Eggs Market

North America Cosmetics Market

Middle East and Africa Refractive Surgery Devices Market

North America Aesthetic Dermatology Market

Asia-Pacific Frozen Ready Meals Market

North America Submarine Cable System Market

Middle East and Africa Wood Pellet Market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 995

Email:- corporatesales@databridgemarketresearch.com"

Coffee is more than just a morning beverage—it's a daily ritual that fuels millions of people around the world. As wellness trends continue to evolve, many consumers are searching for coffee products that offer additional nutritional benefits beyond caffeine. Bryt Better Coffee is designed to meet that demand by combining premium coffee with functional ingredients that support energy, focus, and overall wellness.

Unlike traditional coffee, Bryt Better Coffee features a unique blend of high-quality Arabica coffee, collagen peptides, and functional mushrooms. The result is a smooth, flavorful drink that aims to provide steady energy without the intense jitters or crashes often associated with regular coffee.

What Is Bryt Better Coffee?

Bryt Better Coffee is a functional coffee blend created for individuals who want to improve their daily routine while enjoying a delicious cup of coffee. Instead of relying solely on caffeine for stimulation, the formula incorporates natural ingredients that may support cognitive function, immune health, skin wellness, and sustained energy.

Its convenient instant format allows users to prepare a cup in seconds, making it suitable for busy professionals, students, fitness enthusiasts, and anyone looking for a healthier coffee alternative.

Premium Ingredients

One of the biggest strengths of Bryt Better Coffee is its carefully selected ingredient profile.

100% Arabica Coffee

Arabica beans are known for their rich aroma, smooth taste, and balanced flavor. They naturally contain less caffeine than many Robusta varieties, providing a gentler energy boost that many coffee drinkers appreciate.

Hydrolyzed Collagen Peptides

Collagen is one of the most abundant proteins in the human body and plays an important role in maintaining healthy skin, hair, nails, joints, and connective tissues. Hydrolyzed collagen is processed into smaller peptides that dissolve easily and are simple to incorporate into a daily routine.

Functional Mushroom Complex

Bryt Better Coffee contains a blend of functional mushrooms that have been traditionally valued for their wellness-supporting properties. These include:

-

Lion's Mane

-

Reishi

-

Chaga

-

Cordyceps

-

Maitake

-

Shiitake

-

Turkey Tail

-

King Trumpet

-

Agaricus

-

Willow Bracket

These mushrooms contribute antioxidants and naturally occurring compounds that complement a balanced lifestyle.

Potential Benefits

Many people choose Bryt Better Coffee because it offers more than the typical coffee experience.

Smooth Energy

The moderate caffeine content provides a balanced lift without overwhelming the body. Users may experience improved alertness while avoiding the sharp spikes and crashes common with highly caffeinated drinks.

Enhanced Mental Focus

Functional mushrooms like Lion's Mane have become increasingly popular among individuals looking to support concentration and productivity. Combined with coffee, they create a beverage designed for mental performance.

Daily Wellness Support

The mushroom blend contributes antioxidants, while collagen provides nutritional support for skin and connective tissues. Together, these ingredients create a multifunctional drink that fits easily into everyday routines.

Better Morning Routine

Instead of taking multiple supplements, Bryt Better Coffee combines several wellness ingredients into one convenient beverage, simplifying busy mornings.

Taste and Texture

One concern many people have about mushroom coffee is flavor. Bryt Better Coffee is formulated to maintain the rich taste of premium coffee while minimizing any earthy mushroom notes.

The beverage delivers:

-

Smooth consistency

-

Rich coffee aroma

-

Mild natural sweetness

-

Balanced flavor

-

Pleasant finish

It can be enjoyed black or customized with milk, plant-based alternatives, or natural sweeteners according to personal preference.

How to Use Bryt Better Coffee

Preparing Bryt Better Coffee is simple and convenient.

-

Add one serving to your favorite mug.

-

Pour in hot water.

-

Stir until fully dissolved.

-

Add milk or sweetener if desired.

-

Enjoy as part of your morning or afternoon routine.

It can also be mixed into iced coffee recipes or blended with protein shakes for additional variety.

Who Can Benefit?

Bryt Better Coffee is suitable for a wide range of lifestyles, including:

-

Office professionals seeking steady energy

-

Students preparing for long study sessions

-

Entrepreneurs managing busy schedules

-

Fitness enthusiasts interested in collagen support

-

Coffee lovers looking for a functional beverage

-

Individuals reducing excessive caffeine intake

Its balanced formula makes it a versatile option for everyday use.

Pros

Bryt Better Coffee offers several notable advantages:

-

Premium Arabica coffee blend