The North America region commands a dominant position in the global traction control system market, primarily accelerated by early and strict vehicle safety mandates implemented by agencies like the National Highway Traffic Safety Administration (NHTSA). The market across the United States and Canada is heavily driven by a strong consumer preference for large passenger vehicles, particularly Sport Utility Vehicles (SUVs) and light-duty commercial trucks, which require highly sophisticated traction management hardware to handle their elevated centers of gravity and diverse weather conditions

The automotive industry is undergoing a monumental shift driven by technological innovations, stringent safety regulations, and an increasing consumer preference for intelligent vehicle systems. At the forefront of active vehicle safety is the Traction Control System (TCS). Designed to prevent wheel slip and maintain optimal traction between the vehicle's tires and the road surface especially during acceleration on slippery, wet, or uneven terrains TCS has evolved from a premium luxury feature into a standard automotive requirement.

According to comprehensive research by The Insight Partners, the global Traction Control System Market size is expected to reach US$ 10.56 billion by 2031. The market is anticipated to register a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2025 to 2031. This steady and robust growth is primarily fueled by the escalating production of passenger vehicles, commercial trucks, and electric vehicles (EVs) globally, alongside a rising awareness of road safety.

Government mandates across major regions including North America, the European Union, and parts of Asia-Pacific requiring Electronic Stability Control (ESC) and Anti-lock Braking Systems (ABS), which natively integrate TCS, act as a primary catalyst for market expansion. Furthermore, the integration of these systems into entry-level and mid-tier vehicles in emerging economies is broadening the market's geographic footprint.

The primary objective of a Traction Control System is to maximize longitudinal tire force while maintaining lateral stability. When the system detects a wheel spinning faster than the others, it automatically applies braking pressure to that specific wheel or reduces engine power to regain grip. This capability significantly reduces the risk of hydroplaning and loss of control during sharp cornering or sudden acceleration.

The rapid electrification of the automotive sector is another massive driver for the TCS market. Electric vehicles deliver instant torque, making them highly susceptible to wheel spin during initial acceleration. Consequently, manufacturers are developing advanced, faster-responding electronic TCS architectures tailored specifically for electric and hybrid powertrains. Additionally, the growing consumer demand for Advanced Driver Assistance Systems (ADAS) and autonomous driving features is cementing the importance of next-generation traction management systems, as self-driving platforms require ultra-reliable, real-time chassis and wheel control.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00004321

The global market is characterized by intense competition, with leading automotive component manufacturers continuously investing in research and development to introduce lightweight, cost-effective, and highly responsive safety systems. The prominent industry participants driving innovation in this market include:

ADVICS Co., Ltd

Autoliv Inc

Continental AG

Denso Corporation

Hitachi Automotive Systems Americas Inc

Hyundai Mobis Co., Ltd

Nissin Kogyo Co., Ltd

Robert Bosch GmbH

WABCO Holdings Inc

ZF Friedrichshafen AG

These key players are focusing on strategic collaborations, mergers, acquisitions, and technological expansions to consolidate their market presence. Innovations such as integrated braking systems, which consolidate the ABS, ESC, and TCS software into a single hardware control unit, are becoming the standard offering among these industry giants to reduce overall vehicle weight and manufacturing complexity.

Future Outlook

The future of the Traction Control System market points toward complete software integration and predictive vehicle dynamics. As the automotive industry transitions from traditional mechanical hardware to software-defined vehicles (SDVs), traction control logic will increasingly rely on cloud-connected telemetry, artificial intelligence, and machine learning algorithms. Future TCS architectures will not merely react to wheel slip after it occurs; instead, they will utilize predictive analytics by analyzing real-time weather forecasts, GPS terrain data, and sensor inputs to adjust torque distribution proactively before a tire ever loses grip. Furthermore, the expansion of high-performance multi-motor electric vehicles, which utilize independent torque vectoring at each wheel, will revolutionize the traditional concept of traction control. This technological leap will ensure that the TCS market remains an indispensable, high-value segment of the global automotive ecosystem for decades to come.

Related Reports-

Railway Traction Motors Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The North America inspection drone market leads the global industry due to early automation adoption and strict infrastructure safety regulations. The region’s growth is heavily propelled by the rapid modernization of aging utility grids, expansive oil and gas networks, and massive commercial construction projects. Furthermore, supportive regulatory frameworks established by the Federal Aviation Administration (FAA) are accelerating complex Beyond Visual Line of Sight (BVLOS) operations. Key regional players continually integrate advanced artificial intelligence and sensor payloads to lower asset downtime and eliminate human risk in hazardous industrial environments.

The global industrial landscape is undergoing a massive transformation, driven by automation, digital twins, and advanced robotics. At the forefront of this evolution is the commercial Unmanned Aerial Vehicle (UAV) sector. According to a comprehensive research report by The Insight Partners, the global inspection drone market size is expected to reach US$ 34.4 billion by 2031 from US$ 11.6 billion in 2024. This rapid expansion represents a robust market development, with the industry anticipated to register a compound annual growth rate (CAGR) of 16.8% during the forecast period of 2025–2031.

Historically, asset monitoring across heavy industries such as oil and gas refineries, major power grids, expansive transportation networks, and construction sites depended entirely on manual labor. Workers regularly climbed tall scaffolding, rappelled down wind turbines, or entered hazardous, oxygen-depleted confined spaces to verify structural integrity. These methods are inherently slow, financially draining, and present substantial safety risks. Inspection drones mitigate these challenges by offering automated, high-resolution aerial imaging and advanced data collection tools. They deliver significant cost savings and actionable insights while completely removing human operators from dangerous environments.

Core Market Dynamics and Technological Drivers

The surge in market demand is heavily driven by aging utility infrastructure globally, alongside stricter corporate safety regulations. Modern inspection drones are no longer simple flying cameras; they have evolved into highly specialized flying data-collection platforms. Outfitted with cutting-edge payloads like Light Detection and Ranging (LiDAR), advanced thermal sensors, and multispectral imaging systems, these aerial systems capture precise structural data points that are invisible to the naked human eye.

Structurally, rotary-wing designs currently lead the market due to their capacity to hover stably, take off vertically in tight environments, and closely monitor complex equipment geometries. Simultaneously, the market is seeing a major shift toward automated operations. This shift allows drones to navigate GPS-denied environments such as deep underground mines or heavy metallic indoor boilers completely independently.

Regionally, North America and Europe retain a major portion of global revenue due to their early adoption of predictive maintenance frameworks and stringent infrastructure safety mandates. However, the Asia-Pacific region is emerging as the fastest-growing geographical market. Rapid urbanization, massive smart city initiatives, and expanding energy grids in developing economies like India and China are fueling massive procurement of commercial drone technology.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00014697

Competitive Landscape and Strategic Key Players

The global inspection drone market features an incredibly intense competitive field. Leading manufacturers and software developers continuously innovate to improve flight endurance, strengthen airframe durability, and design industry-specific sensor packages.

The prominent organizations shaping the trajectory of this industry include:

Terra Drone Corp.

ScoutDI AS

Flyability SA

Flybotix SA

Voliro AG

Skydio, Inc.

SZ DJI Technology Co Ltd

AeroVironment Inc

Parrot SA

Delair SAS

Acecore Technologies

These market participants actively focus on strategic expansions, venture capital investments, and collaborative partnerships with global energy and construction conglomerates. By introducing resilient systems such as collision-tolerant indoor cages and omnidirectional aerial platforms these companies successfully lower asset downtime for corporate clients.

Future Outlook

Looking ahead, the future of the inspection drone market will be defined by the deeper convergence of artificial intelligence (AI), machine learning (ML), and cloud analytics. Rather than requiring human operators to manually scrub through hours of raw flight video, next-generation drone ecosystems will deploy AI algorithms directly at the edge to identify structural micro-cracks, corrosion patterns, and thermal anomalies in real-time. Additionally, as global aviation authorities establish standardized regulatory frameworks for Beyond Visual Line of Sight (BVLOS) flights, operations will shift toward decentralized, automated docking stations. These "drone-in-a-box" systems will automatically execute scheduled inspections across hundreds of miles of remote pipelines or electrical grids without a physical pilot on site. Ultimately, this paradigm shift from reactive troubleshooting to autonomous predictive maintenance will solidify drones as indispensable infrastructure assets across the global industrial economy.

Related Reports-

Inspection Drone for Confined Space Market

Drone Inspection and Monitoring Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global industrial landscape is placing a profound emphasis on occupational safety, environmental sustainability, and operational efficiency. Central to this evolution is the deployment of industrial dust collectors essential systems engineered to filter out harmful particulate matter, gases, and airborne contaminants generated during manufacturing processes. According to a comprehensive research report by The Insight Partners, the Industrial Dust Collector Market size is expected to reach US$ 16.18 Billion by 2034 from US$ 10.2 Billion in 2025. The market is estimated to record a CAGR of 5.26% from 2026 to 2034.

Key Market Drivers and Trends

The expansion of the industrial dust collector market is fueled by a combination of strict regulatory frameworks and a growing awareness of health hazards in the workplace. Regulatory bodies globally have established rigorous permissible exposure limits (PELs) to guard against long-term respiratory ailments like silicosis, which are common in mining, construction, and manufacturing environments.

Beyond protecting human health, industrial dust collectors safeguard heavy machinery.Uncontrolled particulate accumulation can settle onto moving machine elements, accelerating equipment degradation, increasing mechanical failure rates, and driving up routine maintenance costs.Furthermore, managing combustible dust is paramount across sectors like woodworking, chemical processing, and food production, where excessive atmospheric dust significantly elevates the risks of catastrophic workplace explosions.

Technological evolution is also altering the market landscape. Modern manufacturing plants are shifting away from traditional systems that operate uniformly at maximum capacity, which strains electrical grids and increases facility costs. Instead, current design paradigms focus heavily on energy optimization, integrating advanced pulse-jet cleaning systems with automated pulse intervals and intelligent variable speed drives. These intelligent systems alter power usage dynamically depending on real-time operational loads, promoting eco-friendly, energy-efficient manufacturing.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00009160

Industry Key Players

The global industrial dust collector marketplace features a mixture of established multinational engineering corporations and specialized filtration technology providers. These players are focused on continuous product development, strategic partnerships, and regional expansions to meet evolving clean-air standards.

Key players operating in the industrial dust collector market include:

3M

Aerotech Inc.

Alstom SA, Ltd

American Air Filter Company, Inc.

Atlas Copco

Beltran Technologies, Inc

Camfil APC

CECO Environmental

Donaldson Company, Inc

Nederman Holding AB

These organizations are progressively engineering modular, highly adaptable filtration configurations. These systems help diverse industrial end-users minimize their ecological footprint while maintaining compliance with local workplace regulations.

Market Segmentation and Insights

The market is analyzed across various parameters, including technology types, product categories, and end-user industries. By technology, the market includes:

Baghouse Dust Collectors: Widely preferred for heavy-duty industrial processing because of their ability to handle immense volumes of gas and highly diverse, coarse particulate streams.

Cartridge Collectors: Highly valued in facilities with limited space where high-efficiency filtration of fine, sub-micron airborne dust is necessary.

Cyclone Dust Collectors: Utilizing centrifugal forces to isolate larger, abrasive particles before they can reach secondary filters, lowering overall equipment wear.

Electrostatic Precipitators (ESPs): Utilizing electrical charging fields to trap ultra-fine particulates from exhaust gases with very little resistance to industrial airflow.

From an end-user standpoint, key sectors such as cement production, pharmaceutical manufacturing, metallurgy, chemicals, and food processing remain the primary consumers. The continuous mechanization and automation within these spaces demand consistent, high-capacity air filtration to sustain peak manufacturing uptime.

Future Outlook

Looking ahead, the future of the industrial dust collector market will be defined by the integration of Industry 4.0 technologies and the push toward net-zero industrial emissions. The deployment of Internet of Things (IoT) sensors within dust collection systems is moving the market from reactive maintenance to predictive servicing. Real-time tracking of filter pressure drops, airflow velocities, and particulate emissions will allow operations teams to address system inefficiencies before component failures occur.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global infrastructure landscape is undergoing a massive transformation, driven by rapid urbanization, aging municipal systems, and a heightened public focus on hygiene and sanitation. At the heart of this transformation is the maintenance of vital underground utilities. The Sewer and Drain Cleaning Services Market size is expected to reach US$ 8,415.25 million by 2031 from US$ 5,565.87 million in 2024. The market is estimated to register a CAGR of 6.0% during 2025–2031. This steady trajectory reflects the indispensable nature of specialized plumbing, maintenance, and wastewater management infrastructure in both residential and industrial sectors worldwide.

Market Drivers and Changing Infrastructure Demands

Several macro-economic and technical factors are propelling the sewer and drain cleaning services sector forward. In many developed regions, municipal pipeline networks have been operational for decades, making them highly susceptible to structural deterioration, root intrusion, and severe blockages. Concurrently, expanding urban centers in developing economies are putting an unprecedented load on existing wastewater frameworks.

Environmental regulations have also become considerably stricter. Regulatory authorities are increasingly penalizing commercial entities and municipalities for sewage overflows or untreated wastewater leaks, prompting a shift from reactive emergency repairs to proactive, scheduled maintenance protocols. Furthermore, extreme weather events caused by shifting global climates have resulted in frequent flooding, placing immense pressure on storm drains and demanding immediate, high-capacity cleaning interventions.

Technological Advancements Reshaping the Market

The industry is moving away from purely mechanical, invasive rod-and-cable methods toward sophisticated, technology-driven diagnostic and cleaning procedures. High-definition closed-circuit television (CCTV) camera inspections have become standard practice, allowing technicians to locate structural defects or blockages with pin-point accuracy without digging.

For clearance, hydro-jetting technology which utilizes ultra-high-pressure water streams to blast away grease, scale, and debris is heavily favored for its efficiency and eco-friendliness, as it eliminates the need for harsh chemical cleaners. Additionally, trenchless pipe rehabilitation techniques like Cured-in-Place Pipe (CIPP) lining are gaining popularity, enabling service providers to repair internal pipe structures from within existing access points, saving clients both time and significant excavation costs.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00040907

Key Industry Players

The competitive arena of the sewer and drain cleaning services market features a mix of massive, franchised commercial networks and highly specialized regional industrial contractors.

Key players operating in this space include:

Clean-Co Systems

Len The Plumber

Rooter Hero Plumbing

Benjamin Franklin Franchising SPE LLC.

Roto-Rooter Group Inc

Modern Plumbing Industries, Inc.

Mr. Rooter

Bob Oates

Haller Enterprises

Neptune Plumbing

Augusta Industrial Services

Frank’s Repair Plumbing, Inc.

These organizations are actively sustaining their market dominance by investing in advanced fleet vehicles, expanding their geographic service footprints through franchise networks, and implementing digital scheduling and dispatch platforms to enhance customer experience.

Future Outlook

Looking ahead, the sewer and drain cleaning services market is poised to become smarter and more integrated. The future of the industry lies in the adoption of Internet of Things (IoT) sensors within municipal and commercial plumbing networks, allowing for real-time monitoring of flow rates and sediment accumulation. This shift will enable service providers to transition completely into predictive maintenance models, clearing structural vulnerabilities before a physical backup even occurs. Additionally, as water scarcity escalates globally, technologies that recycle hydro-jetting water directly inside service trucks are expected to gain widespread adoption. Backed by expanding smart city initiatives and an unyielding global demand for sanitary living conditions, the market will remain a resilient and highly lucrative sector of the broader utility infrastructure industry through 2031 and beyond.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

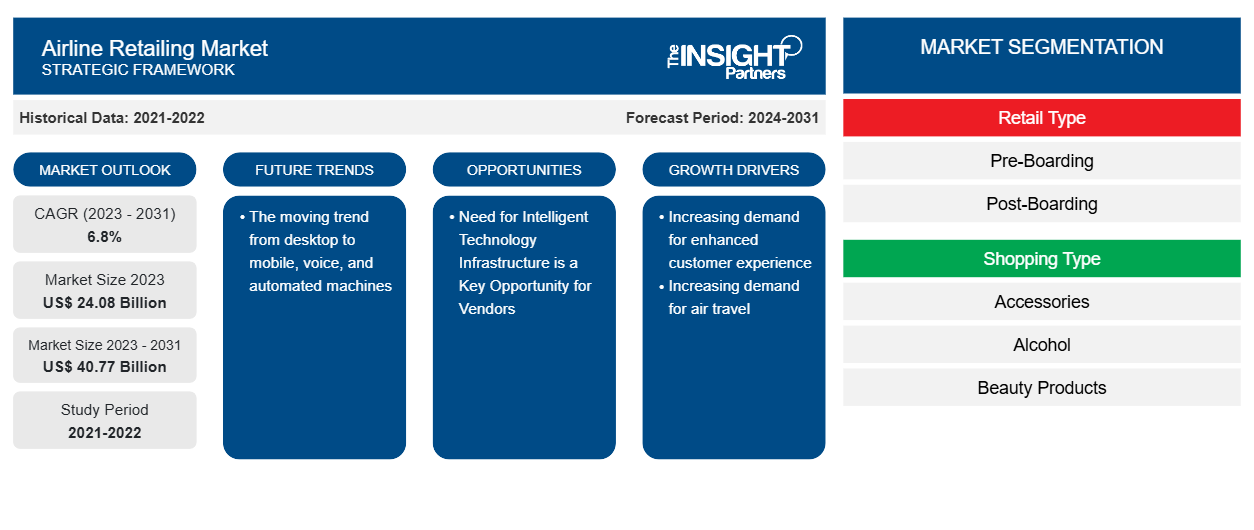

Driven by early technology adoption and a mature aviation ecosystem, the North America airline retailing market is experiencing substantial modernization. The United States, in particular, acts as a primary hub for this transition, as major carriers aggressively integrate IATA’s New Distribution Capability (NDC) standards to bypass legacy distribution bottlenecks. North American airlines are heavily prioritizing hyper-personalization, utilizing cloud infrastructure and artificial intelligence to offer tailored ancillary options such as customized baggage pricing, premium lounge access, and co-branded credit card loyalty rewards directly through mobile applications. Furthermore, the presence of major travel technology providers in the region guarantees continuous software innovation, ensuring that North American passenger experiences remain highly frictionless and retail-centric throughout the travel journey.

The commercial aviation landscape is undergoing a massive paradigm shift. Driven by a transition from traditional ticketing to dynamic, customer-centric commerce, the global aviation industry has embraced advanced digital strategies. Today, airlines no longer view themselves as mere transport providers; they operate as modern digital retailers.

According to a comprehensive study by The Insight Partners, the global Airline Retailing Market size is projected to reach US$ 40.77 billion by 2031 from US$ 24.08 billion in 2023. The market is expected to register a CAGR of 6.8% during the forecast period of 2023–2031. This steady growth highlights the rapid adoption of digital storefronts, personalized ancillary services, and artificial intelligence-driven dynamic pricing models designed to elevate the traveler experience.

Bearings are fundamental components in modern engineering, serving as the invisible backbone for virtually everything that rotates, rolls, or moves. From massive industrial wind turbines to the micro-motors found in medical devices, these precision-engineered components are critical for reducing friction and handling heavy mechanical loads. According to a comprehensive research report by The Insight Partners, the global bearing industry is currently experiencing a transformative growth phase, driven by rapid industrialization, automation, and the global shift toward cleaner energy systems.

Market Valuation and Growth Trajectory

The Bearing Market size is projected to reach US$ 210.864 billion by 2031 from US$ 127.912 billion in 2024. The market is expected to register a CAGR of 7.51% during 2025–2031. This robust growth trajectory highlights an escalating demand across diverse sectors, particularly automotive, aerospace, heavy machinery, and robotics.

As developing economies expand their manufacturing infrastructure and developed nations modernize their industrial plants with IoT-enabled technologies, the reliance on high-quality, long-lasting bearings has never been higher. The steady Compound Annual Growth Rate (CAGR) reflects a market that is not just expanding in volume, but also shifting toward higher-value, specialized bearing solutions.

Primary Growth Drivers

Several macro-economic and technological trends are fueling this market expansion:

The Electric Vehicle (EV) Revolution: The automotive industry is undergoing its most significant shift in a century. EVs require specialized bearings that can operate smoothly at much higher rotational speeds (RPMs) while minimizing noise, vibration, and harshness (NVH). Furthermore, these bearings must offer low friction to maximize battery range and prevent electrical arcing from damaging internal components.

Industrial Automation and Robotics: The rise of Industry 4.0 has led to widespread deployment of automated manufacturing lines and robotic arms. These systems demand high-precision miniature and slewing bearings capable of precise, repetitive movements over millions of cycles without failure.

Renewable Energy Infrastructure: The global push for green energy has led to massive investments in wind power. Wind turbines rely heavily on large-diameter main shaft and gearbox bearings that can withstand extreme, unpredictable aerodynamic loads and harsh environmental conditions over a multi-decade lifespan.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPTE100000700

Key Market Players

The global bearing market is highly competitive, characterized by a mix of established legacy manufacturers who continually innovate to maintain their market share. The prominent companies leading the industry include:

SKF (Sweden) – A global leader recognized for its extensive range of rolling bearings, seals, and lubrication systems, heavily focusing on digital monitoring and sustainability.

Schaeffler Group (Germany) – Renowned for its INA and FAG brands, driving innovation in high-precision components for automotive engines, transmissions, and industrial applications.

The Timken Company (USA) – A specialist in tapered roller bearings, widely trusted for heavy-duty industrial machinery, rail, and aerospace applications.

NSK Ltd. (Japan) – One of the foremost suppliers of ball bearings and automotive components, known for exceptional reliability and motion control technologies.

NTN Corporation (Japan) – A major global supplier specializing in eco-friendly bearing designs and constant velocity joints for the automotive sector.

NACHI-FUJIKOSHI CORP. (Japan) – A versatile manufacturer integrating bearing production with cutting tools, hydraulics, and industrial robotics.

JTEKT CORPORATION (Japan) – Known for its Koyo bearing brand, providing advanced steering systems and high-performance bearings across global supply chains.

These industry giants are aggressively investing in Research and Development (R&D) to develop "smart bearings" equipped with integrated sensors. These sensors monitor temperature, vibration, and lubrication levels in real time, allowing operators to perform predictive maintenance before a catastrophic failure occurs.

Future Outlook

The future of the bearing market points toward a convergence of material science and digital technology. Over the coming years, expect to see accelerated adoption of ceramic and hybrid bearings which utilize silicon nitride ceramic balls inside steel rings due to their superior heat resistance, lower weight, and electrical insulation properties. Furthermore, sustainability will become a core focus; manufacturers are increasingly utilizing recycled steel and carbon-neutral production processes to meet strict corporate environmental goals. As industries across the globe continue to prioritize energy efficiency, the development of ultra-low-friction bearings will remain paramount, solidifying the bearing industry's role as a vital catalyst for global economic and technological progress.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The aerospace industry relies on structural components that ensure vehicle integrity, passenger comfort, and operational safety. Among these critical elements, aircraft engine mounts play a fundamental role. These specialized components connect the aircraft engine to the fuselage or wing pylons. Beyond providing mechanical support, engine mounts absorb severe engine vibrations, secure heavy propulsion systems, and minimize structural stress transferred to the airframe during flight maneuvers. Driven by a surge in commercial airline fleets, continuous military modernizations, and rapid breakthroughs in lightweight materials, this sector is poised for substantial financial expansion.

Market Size and Significant Projections

According to a comprehensive industry study, the global aircraft engine mount market is entering a phase of robust, continuous growth. The Aircraft Engine Mount Market size is expected to reach US$ 1,741.57 Million by 2034 from US$ 918.92 Million in 2025. This long-term expansion highlights a stable market trajectory, with the industry estimated to record a CAGR of 7.36% from 2026 to 2034.

This sustained growth is heavily supported by the increasing global demand for single-aisle commercial aircraft, alongside a massive push to replace aging fleets with fuel-efficient, next-generation variants. Because engine mounts must endure extreme thermal conditions and intense kinetic forces, they are subject to regular, stringent maintenance and replacement schedules. This routine maintenance establishes a highly profitable aftermarket segment that complements original equipment manufacturer (OEM) demands.

Market Growth Drivers and Technical Shifts

Modern aviation demands quieter, lighter, and more aerodynamically efficient aircraft. To fulfill these design requirements, engine manufacturers have introduced high-bypass and ultra-high-bypass turbofan engines. While these propulsion systems offer superior fuel economy, they feature larger fan diameters and significantly increased weight. Consequently, aircraft structures must adapt, leading to the development of advanced engine mounts capable of distributing immense thrust loads without altering the aircraft's center of gravity or exceeding strict weight budgets.

Material science acts as another primary catalyst driving market growth. Traditional engine mounts constructed from standard steel alloys are steadily being replaced by high-performance materials. Advanced titanium alloys, nickel-based superalloys, and carbon fiber composite integrations are increasingly favored by modern aerospace designers. These advanced materials provide exceptional strength-to-weight ratios and superior resistance to corrosion and thermal fatigue, directly expanding product lifecycles and lowering long-term maintenance overhead for global commercial operators.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00029696

Competitive Landscape and Key Industry Players

The global aircraft engine mount market is characterized by a mix of established tier-1 aerospace component manufacturers, specialized engineering firms, and comprehensive aviation technology companies. These organizations focus on collaborative design cycles with major airframe and engine OEMs, expanding their domestic production capabilities, and dedicating capital to advanced metallurgy and elastomeric dampening research.

Prominent market participants steering the technical development and distribution of aircraft engine mounts include:

Acorn Welding

Cadence Aerospace

Continental Aerospace Technologies

EPI Inc.

Honda Aircraft Company

Parker Hannifin Corporation

SAM Suzhou

The Wag Aero Group

VAN'S AIRCRAFT, INC.

Strategic partnerships, long-term procurement contracts with defensive bodies, and precision additive manufacturing (3D printing) represent the core methodologies utilized by these key entities to secure market share and meet evolving custom engineering specifications.

Future Outlook

Looking ahead, the aircraft engine mount market will transform in parallel with the foundational evolution of modern aviation design. Over the next decade, the industry will pivot toward supporting advanced aerial mobility, electric vertical takeoff and landing (eVTOL) aircraft, and hybrid-electric propulsion systems. These emerging electric configurations present entirely unique engineering challenges, demanding engine mounts optimized for high-frequency electrical isolation and minimal acoustic profiles rather than traditional high-thrust dampening. Furthermore, the increasing integration of smart sensors into component structures will enable real-time health monitoring and predictive maintenance. By allowing structural flaws to be diagnosed before component failure occurs, these advanced technologies will enhance international flight safety and cement the engine mount sector's role in the future of automated, highly efficient aerospace ecosystems.

Related Reports-

Aircraft Engine Forging Market

Aircraft Engine Compressor Market

Aircraft Engine Fuel Systems Market

Aircraft Engine Component Market

North America Aircraft Engine Forging Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global automotive landscape is undergoing a monumental paradigm shift, transitioning rapidly from traditional internal combustion engines (ICE) to electric and hybrid vehicles. At the heart of this transformation is the lithium-ion battery pack, a component that demands precise environmental conditions to operate safely, efficiently, and durably. Consequently, the reliance on advanced cooling and heating infrastructure within vehicles has intensified, turning battery thermal management into a cornerstone of modern automotive engineering.

The Automotive Battery Thermal Management System Market size is expected to reach US$ 10.53 billion by 2031. The market is anticipated to register a CAGR of 15.2% during 2025-2031. This robust growth trajectory underscores the escalating production of electric vehicles (EVs), breakthroughs in battery chemistry, and stringent regulatory mandates worldwide aimed at curbing vehicular emissions.

Batteries are highly sensitive to temperature fluctuations. Operational environments that are too hot accelerate degradation, reduce driving range, and in extreme scenarios trigger thermal runaway, a catastrophic chain reaction leading to fires. Conversely, extremely cold temperatures severely restrict a battery's ability to accept or deliver a charge, diminishing performance and slowing down fast-charging capabilities.

Automotive battery thermal management systems (BTMS) resolve these issues by utilizing technologies such as liquid cooling, air cooling, phase change materials (PCM), and thermoelectric modules. By maintaining the battery pack within its optimal temperature window (typically between 20°C and 40°C), these systems optimize energy efficiency, ensure passenger safety, and extend the overall lifespan of the vehicle's powertrain.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00006121

Several critical factors are propelling the expansion of the BTMS market. First, the consumer demand for driving range autonomy has pushed automakers to deploy larger battery capacities and higher voltage architectures (such as 800V systems). Higher voltage architectures enable ultra-fast charging, but they also generate massive amounts of heat during the charging cycle, necessitating highly sophisticated liquid-cooling circuits.

Furthermore, governments globally are introducing strict fuel economy standards and offering lucrative incentives for EV adoption. This regulatory tailwind is forcing original equipment manufacturers (OEMs) to invest heavily in next-generation thermal management architectures. Integration is another key trend; modern systems do not just cool the battery in isolation but manage the thermal needs of the electric motor, power electronics, and passenger cabin holistically to conserve every watt of energy.

The global marketplace is characterized by intense competition, featuring a mix of established automotive tier-1 suppliers and specialized technology providers investing aggressively in research and development. Key players shaping the competitive landscape include:

Calsonic Kansei Corporation

Continental AG

Dana Incorporated

Gentherm Incorporated

Hanon Systems

LG Chem Ltd.

MAHLE GmbH

Robert Bosch GmbH

SAMSUNG SDI CO., LTD.

Valeo

These industry leaders are focused on scaling production, forming strategic partnerships with OEMs, and pioneering lightweight, compact thermal components to reduce the overall weight of electric vehicles.

Future Outlook

The future of the Automotive Battery Thermal Management System market points toward a highly integrated and intelligent ecosystem. As solid-state batteries edge closer to commercialization, thermal requirements will evolve, demanding systems capable of managing unique pressure and high-temperature operating thresholds. Additionally, the integration of artificial intelligence and predictive software into vehicle energy management will allow future BTMS to anticipate thermal loads based on driving habits, GPS terrain data, and weather forecasts. This shift from reactive cooling to proactive, intelligent thermal orchestration will significantly enhance EV range and charging speeds, securing BTMS as an indispensable technology in the next generation of autonomous and electrified transportation.

Related Reports-

Electric Vehicle Battery Swapping Market

Battery Production Machine Market

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876