The global automotive sector is undergoing a massive transformation, driven by technological advancements, evolving consumer preferences, and stringent safety standards. At the heart of this transformation are components that bridge the gap between vehicle aesthetics, ergonomics, and safety. Among these, steering column cowls play an indispensable role. Serving as the protective housing for the steering column assembly, these components shield internal wiring, switches, and electronic modules while contributing to the vehicle's interior visual appeal.

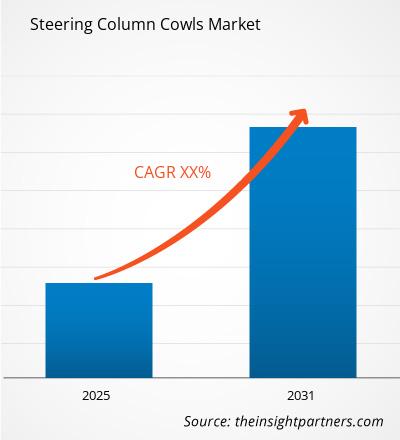

According to a comprehensive market study by The Insight Partners, the global Steering Column Cowls Market size is projected to reach US$ 8.36 billion by 2034 from US$ 5.36 billion in 2025. The market is anticipated to register a CAGR of 5.07% during the forecast period 2026-2034. This steady growth highlights the escalating production of passenger and commercial vehicles worldwide, combined with a rising demand for premium and technologically integrated vehicle interiors.

Market Dynamics and Driving Factors

The steady expansion of the steering column cowls market is heavily influenced by the global shift toward smart and connected vehicles. Today’s steering assemblies are no longer just mechanical links to the wheels; they host advanced electronics, including Advanced Driver Assistance Systems (ADAS) controls, infotainment toggles, and steering wheel heating systems. As a result, steering column cowls must be precision-engineered to accommodate complex wiring harnesses and electronic control units (ECUs) without compromising driver legroom or cabin comfort.

Another crucial factor driving market growth is the global surge in electric vehicle (EV) adoption. Lightweighting has become a top priority for EV manufacturers aiming to maximize battery range. Consequently, component suppliers are pivoting from traditional heavy plastics to advanced composite materials and lightweight polymers. This transition is injecting fresh momentum into the steering column cowls supply chain, creating lucrative opportunities for manufacturers who specialize in high-durability, lightweight injection-molded solutions.

Furthermore, strict crash safety regulations mandated by organizations like the New Car Assessment Program (NCAP) require automotive interiors to minimize driver injury during a collision. Modern steering column cowls are designed with energy-absorbing structures that break away safely under high impact, reducing the risk of injury to the driver’s lower limbs. This regulatory push ensures that the demand for high-quality, safety-compliant steering column cowls remains robust across all automotive segments.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00021251

Industry Landscape and Key Competitors

The global market features a highly competitive and fragmented landscape, comprising prominent Tier-1 automotive suppliers, specialized plastic injection molding companies, and niche classic car component providers. These entities continuously invest in material science, automated manufacturing processes, and strategic partnerships to strengthen their market presence and expand their geographic footprint.

Some of the key players operating in the global steering column cowls market include:

Allon White Sports Cars

Brown and Gammons

Cascade Engineering

DS Smith Plc

Fuji Autotech AB

Jaguar Land Rover Automotive PLC

Moss Motors, Ltd

SC Parts Group Ltd

TVR Parts Limited

Zanini Auto Grup, S.A.U.

These organizations play varied roles, ranging from high-volume OEM manufacturing to supplying high-quality aftermarket and replacement components for luxury, sports, and heritage vehicles.

Regional Analysis

Geographically, the Asia-Pacific region dominates the steering column cowls market, propelled by massive vehicle production volumes in China, India, Japan, and South Korea. Rapid urbanization, increasing disposable incomes, and expanding middle-class populations in these emerging economies continue to fuel the sales of passenger cars. Additionally, the presence of major manufacturing hubs lowers production costs, making the region a critical focal point for global suppliers.

North America and Europe follow closely, characterized by a high penetration of luxury vehicles and stringent automotive safety mandates. In these regions, the emphasis is heavily placed on premium material finishes, noise, vibration, and harshness (NVH) reduction, and sustainable manufacturing practices, encouraging suppliers to deploy advanced textures and sustainable bio-plastics in cowl production.

Future Outlook

The future outlook for the global steering column cowls market remains highly optimistic, driven by the inevitable evolution toward autonomous driving and highly integrated vehicle cockpits. As autonomous driving technology matures, the traditional steering wheel setup is expected to change drastically, with some concepts exploring retractable or fold-away steering columns. This paradigm shift will require next-generation steering column cowls to be highly modular, adaptable, and smart—potentially embedding touch-sensitive surfaces, ambient LED lighting, or driver-monitoring sensors directly into the housing. Furthermore, the industry's intensifying commitment to sustainability will accelerate the adoption of recycled plastics and carbon-neutral manufacturing processes. This pivot toward eco-friendly materials, combined with the rising worldwide demand for safer and more luxurious vehicle cabins, will solidify the market's upward trajectory, ensuring consistent growth and innovation through 2034 and beyond.

Related Reports-

Electronic Power Steering (EPS) Market

Marine Steering Systems Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global supply chain and logistics ecosystem is undergoing a massive transformation, driven by the exponential growth of e-commerce, expanding maritime trade, and the urgent need for operational efficiency at freight hubs. At the heart of these bustling hubs ranging from busy marine ports to sprawling distribution centers is the trailer terminal tractor. Often referred to as yard trucks, yard goats, or spotter trucks, these heavy-duty vehicles are engineered specifically for moving semi-trailers within cargo yards, warehouse facilities, and intermodal terminals. According to a comprehensive study by The Insight Partners, the market for these specialized vehicles is poised for remarkable growth over the next decade.

The global Trailer Terminal Tractor Market size is projected to reach US$ 16.16 billion by 2034 from US$ 8.42 billion in 2025. The market is anticipated to register a CAGR of 7.52% during the forecast period 2026-2034. This robust growth trajectory highlights the escalating reliance on automation and mechanized handling systems to mitigate operational bottlenecks and manage the unprecedented volumes of freight moving across the globe.

Market Drivers and Dynamics

Several critical factors are propelling the expansion of the trailer terminal tractor market. First and foremost is the pressure on logistics providers to reduce turnaround times. Standard over-the-road trucks are inefficient when it comes to short-distance, repetitive trailer spotting because drivers must repeatedly exit the cab to raise and lower landing gear. In contrast, terminal tractors are equipped with a hydraulic lifting fifth wheel that allows the operator to move trailers without leaving the driver’s seat. This significantly minimizes manual labor, enhances safety, and accelerates the movement of goods.

Furthermore, the expansion of inland container depots and the modernization of seaport infrastructure particularly across developing economies in the Asia-Pacific and Middle East regions are creating a sustained demand for high-capacity terminal tractors. Governments and private operators are investing heavily in updating port machinery to handle mega-container vessels, necessitating a reliable fleet of support vehicles on the ground.

Another massive shift steering the market is the transition toward sustainable energy. Stricter environmental regulations aimed at reducing carbon emissions in industrial zones have forced fleet operators to rethink their reliance on traditional diesel-powered tractors. As a result, manufacturers are investing heavily in research and development to introduce electric and hybrid alternatives, which not only curb emissions but also reduce long-term maintenance and fuel costs.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00020737

Competitive Landscape and Key Players

The trailer terminal tractor market features a mix of well-established automotive giants and highly specialized material handling equipment manufacturers. These companies are actively engaging in strategic partnerships, product innovations, and regional expansions to capture a larger share of this growing market.

Some of the prominent key players operating in the industry include:

BYD Co Ltd: A pioneer in electromobility, driving the market forward with its advanced, high-capacity electric yard tractors.

Capacity Trucks: Renowned for producing robust, customizable yard trucks tailored for port, rail, and warehouse operations.

Cargotec (Kalmar): A global leader in cargo handling solutions, consistently innovating with automated and eco-efficient terminal tractors.

CVS Ferrari S.P.A.: Highly regarded for manufacturing heavy-duty material handling machinery capable of enduring rigorous port environments.

Hoist Material Handling, Inc.: Known for high-quality, heavy-lift equipment and rugged vehicles optimized for industrial logistics.

Konecranes: A heavyweight in the lifting industry, offering smart, integrated terminal solutions that enhance port productivity.

MAFI Transport-Systeme GmbH: Specializing in heavy-duty tractors and trailers designed for internal transport in ports and industry.

Mol CY nv: An established manufacturer recognized for producing reliable, custom-engineered terminal and RoRo tractors.

The Autocar Company: A legendary American brand producing highly efficient, driver-focused spotter trucks with severe-duty capabilities.

The Volvo Group: A global automotive powerhouse delivering premium, high-performance powertrain technologies and sustainable transport solutions.

Future Outlook

The future of the trailer terminal tractor market points toward an increasingly automated, intelligent, and zero-emission ecosystem. Over the forecast period, the market will likely see a rapid displacement of diesel tractors by battery-electric (BEV) and hydrogen fuel-cell models, aligned with global net-zero goals. Beyond electrification, the integration of autonomous driving technology is set to redefine yard management. Autonomous terminal tractors, guided by sophisticated lidar, radar, and AI software, are already undergoing successful pilots in restricted, controlled port environments. As these technologies mature, fully driverless yard trucks will become standard in mega-distribution centers, seamlessly syncing with warehouse management systems to maximize throughput, eliminate human error, and ensure round-the-clock operational continuity.

Related Reports-

Four Wheel Drive Tractor Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

In an era defined by shifting geopolitical dynamics, expanding maritime trade, and an increasing frequency of climate-induced naval emergencies, the modernization of coastal and blue-water defense infrastructure has become paramount. Central to these defense strategies is the procurement of highly specialized vessels designed for rapid intervention, extraction, and lifesaving operations.

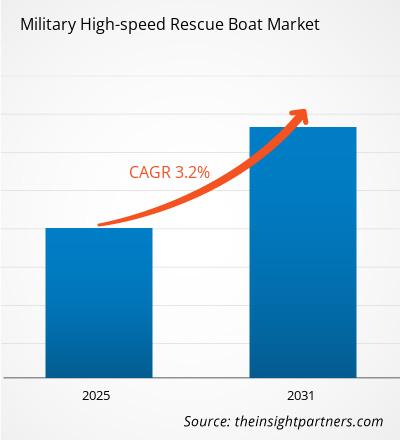

The Military High-Speed Rescue Boat Market size is expected to reach US$ 211.11 Million by 2034 from US$ 181.92 Million in 2025. The market is estimated to record a CAGR of 1.88% from 2026 to 2034. While a compound annual growth rate of 1.88% indicates a steady, conservative expansion, it reflects a deeply consolidated and highly specialized sector where the emphasis has transitioned from sheer volume procurement to advanced, tech-heavy asset modernization.

Market Drivers and Changing Operational Demands

The steady trajectory of this market is fueled by the evolving nature of maritime security threats and defense mandates. Modern military and paramilitary forces including coast guards, naval commandos, and search-and-rescue (SAR) agencies are facing challenges that demand unprecedented operational agility. High-speed rescue boats are no longer viewed simply as transport craft; they are highly integrated tactical platforms.

Key factors driving the market include:

Asymmetric Maritime Threats: The rise in piracy, human trafficking, and illegal seaborne incursions requires territorial defense forces to possess interceptors capable of extreme speeds and high maneuverability in rough sea states.

Disaster Response and Humanitarian Assistance: Climate change has amplified the frequency and severity of extreme weather events. Naval forces are increasingly deployed as first responders in humanitarian crises, necessitating ruggedized rescue craft that can operate safely in debris-strewn or shallow coastal environments.

Technological Integration: Transitioning to shock-mitigation seating, advanced satellite communications, forward-looking infrared (FLIR) cameras, and lightweight composite hulls has driven procurement cycles as aging fleets are retrofitted or replaced to match modern operational demands.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00023388

Key Industry Players

The global marketplace is shaped by a mix of premier defense contractors, specialized marine engineering firms, and maritime safety experts. These companies continuously innovate to meet stringent military standards (such as NATO requirements) regarding durability, speed, and launch-and-recovery capabilities.

Prominent players driving innovation and holding significant market share include:

VIKING LIFE-SAVING EQUIPMENT A/S – Renowned for high-end maritime safety solutions, providing defense forces with comprehensively equipped and reliable search-and-rescue vessels.

PALFINGER AG – A dominant force in marine cranes and launch-and-recovery systems, producing rugged, high-speed military interceptors and rescue craft designed for complex shipboard deployments.

Sealegs International Limited – Highly distinct for its patented amphibious craft technology, allowing military forces to transition seamlessly from deep water directly onto rugged terrain.

ZODIAC MILPRO – A global leader in inflatable and rigid inflatable boats (RIBs) engineered specifically for military, special forces, and law enforcement operations.

Asis Boats – Renowned for custom-built, high-performance military rigid hull inflatable boats (RHIBs) that focus on speed, tactical deployment, and advanced navigation arrays.

Fassmer – A premier German shipyard supplying sophisticated, high-performance rescue and patrol vessels tailored for complex naval architectures and coast guard duties.

Boomeranger Boats Ltd – Specialized in customized RIBs and rigid-hulled workboats utilized extensively by special forces, marine police, and naval boarding parties.

HATECKE GmbH – An established name in lifesaving equipment, engineering robust free-fall boats and high-speed rescue vessels that survive extreme maritime environments.

GEMINI MARINE BOATS – Highly regarded for manufacturing resilient, commercial, and military-grade RIBs utilized by international defense forces for coastal policing and rescue operations.

Survitec Group Limited – A global leader in survival and safety solutions, offering highly reliable critical safety equipment alongside specialized inflatable rescue assets.

Market Segmentation and Structural Overview

The market typically segments by hull type primarily Rigid Inflatable Boats (RIBs), inflatable boats, and aluminum/composite rigid boats as well as by propulsion type, where advanced inboard diesel waterjets and high-horsepower outboard motors dominate.

Geographically, coastal regions with extensive maritime borders and high geopolitical friction, such as the Asia-Pacific and Euro-Atlantic regions, represent significant demand centers. The North American market remains steady due to substantial defense budgeting and ongoing modernization programs by the U.S. Navy and Coast Guard. Meanwhile, emerging maritime strategies in developing nations are sparking localized procurement initiatives.

Future Outlook

Looking ahead, the military high-speed rescue boat market is poised to be profoundly transformed by digitization, automation, and eco-conscious engineering. While the fundamental requirement for speed and structural integrity remains unyielding, future demand will heavily lean toward autonomous or optionally-manned surface vessels (USVs) capable of conducting high-risk search-and-rescue sweeps without endangering crew members in hazardous conditions. Furthermore, integration with drone technology for real-time aerial scouting will become standard protocol. On the propulsion front, standard diesel arrays will gradually face competition from hybrid and electric marine powertrains tailored for stealth operations and reduced carbon footprints. As naval frameworks increasingly adopt networked, multi-domain operations, these rescue craft will transition into highly connected electronic nodes, ensuring their critical relevance through 2034 and beyond.

Related Reports-

Search and Rescue Robots Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global landscape of defense, aerospace, and advanced situational awareness is undergoing a profound technological transformation. At the heart of this evolution is the integration of highly sophisticated visual systems that combine real-time data streaming with precise threat tracking.

Market Size and Growth Trajectory

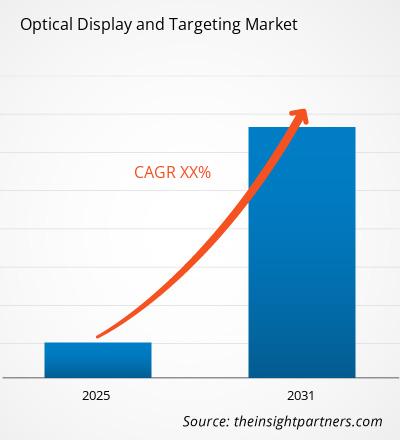

The global Optical Display and Targeting Market size is expected to reach US$ 14.55 Billion by 2034 from US$ 9.44 Billion in 2025. This expansion indicates a steady and robust modernization cycle across defense sectors, with the market anticipated to register a CAGR of 4.92% during the forecast period 2026–2034.

This sustained growth is heavily driven by the defense sector's transition away from legacy analog instrumentation toward fully integrated digital glass cockpits, augmented reality (AR) helmet-mounted displays, and electro-optical targeting systems (EOTS). As geopolitical landscape complexities require faster, multi-domain command operations, the reliance on high-definition optical targeting systems has evolved from a premium luxury to an operational necessity.

Key Market Drivers

Several fundamental factors are propelling the steady growth of this industry:

Rise of Next-Generation Combat Platforms: The deployment of fifth- and sixth-generation fighter aircraft, modern armored vehicles, and naval warships depends heavily on advanced sensor fusion. Optical displays are required to seamlessly merge inputs from radar, thermal imaging, and electronic warfare suites into a single, cohesive visual interface for operators.

Adoption of Augmented Reality (AR) and Head-Up Displays (HUDs): Military forces are increasingly relying on HUDs and Helmet-Mounted Display Systems (HMDS) to give pilots and dismounted soldiers a clear tactical advantage. These systems overlay critical flight telemetry, target coordinates, and threat alerts directly onto the user's field of view, maximizing reaction times and reducing cognitive fatigue.

Surge in Unmanned Systems: The exponential utilization of Unmanned Aerial Vehicles (UAVs) and autonomous ground systems has fueled massive demand for lightweight, high-performance optical payloads. Precision targeting gimbals and remote display stations are vital to ensuring the accuracy of long-range reconnaissance and strike missions.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00018547

Key Industry Players

The competitive landscape features a mix of aerospace pioneers and defense engineering giants driving hardware and software innovations. Leading companies anchoring the global marketplace include:

BAE Systems — Renowned for its advanced helmet systems and digital Head-Up Displays that improve situational awareness for pilots.

Collins Aerospace — A leader in flight deck interiors, smart displays, and integrated targeting electronics for commercial and military aviation.

ECA GROUP — Specializes in cutting-edge robotic solutions, remote control centers, and optical equipment tailored for naval and subsea defense operations.

Elbit Systems Ltd. — Globally recognized for its advanced line of helmet-mounted displays and electro-optical tracking payloads used across diverse terrain.

Kongsberg Defence and Aerospace — A major provider of remote weapon stations, naval strike missiles, and high-precision targeting sub-systems.

L3Harris Technologies, Inc. — Dominates the market in tactical communication systems and night-vision optical enhancements for ground forces.

Leonardo S.p.A. — An international leader in laser targeting pods, airborne infrared search-and-track systems, and naval firing radar.

Northrop Grumman — Integrates comprehensive sensor and display architectures for state-of-the-art military aircraft, including the F-35 program.

Rolta India Limited — Delivers defense-grade geospatial analytics, command-and-control software mapping, and digitized military display infrastructure.

Safran — A heavyweight in aerospace propulsion and optronics, manufacturing world-class military thermal sights, guidance systems, and laser rangefinders.

Regional Market Highlights

North America currently maintains the largest market share, driven primarily by the massive modernization budgets of the U.S. Department of Defense and ongoing investments in next-generation fighter programs. Meanwhile, Europe is witnessing accelerated growth as member nations update their tactical fleets and armored vehicle components in response to changing regional security dynamics.

The Asia-Pacific region is projected to register the fastest growth rate through 2034. Aggressive military expansion, localized manufacturing initiatives (such as India's "Make in India" defense push), and escalating maritime patrolling activities are compelling nations like China, India, and Japan to secure state-of-the-art targeting technology.

Future Outlook

Looking ahead, the future of the Optical Display and Targeting market will be defined by the convergence of artificial intelligence (AI), edge computing, and micro-display innovations. We will see standard target-tracking systems transition into predictive threat-evaluation platforms capable of identifying and prioritizing multiple hazards autonomously. The integration of high-refresh-rate micro-LED and micro-OLED screens will enable much smaller, lightweight form factors for ground infantry wearables, bringing high-end targeting diagnostics directly to the tactical edge. Over the next decade, as multi-domain operations become the standard framework for global security forces, the demand for ultra-low latency, jam-resistant optical display networks will remain an absolute pillar of defense technology investment.

Related Reports-

Airport Display Systems Market

Aerospace Helmet Mounted Display Market

Multi-Function Display (MFD) Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global industrial manufacturing landscape is undergoing a massive transformation, driven by the increasing need for component longevity, wear resistance, and high-performance surface engineering. At the forefront of this evolution is the thermal spray technology sector. Thermal spraying involves a group of coating processes in which finely divided metallic or non-metallic materials are deposited in a molten or semi-molten condition to form a protective or functional layer. As industries from aerospace to automotive strive to minimize equipment downtime and reduce maintenance costs, the adoption of advanced surface coatings has spiked dramatically.

Market Size and Growth Trajectory

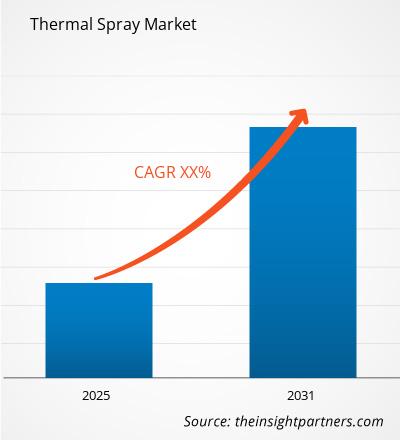

The global Thermal Spray Market size is projected to reach US$ 20.36 billion by 2034 from US$ 11.93 billion in 2025. The market is anticipated to register a CAGR of 6.12% during the forecast period 2026-2034. This steady compound annual growth rate reflects a robust demand across diverse end-use verticals, heavily supported by rapid industrialization, infrastructural developments, and the continuous search for materials that can withstand extreme environmental conditions.

Dynamic Market Drivers and Applications

The sustained expansion of the thermal spray market is primarily propelled by the burgeoning aerospace and defense industries. Aircraft engines and components operate under extremely elevated temperatures and corrosive environments, making thermal barrier coatings (TBCs) vital for ensuring safety and efficiency. Furthermore, the automotive sector relies heavily on thermal spraying for engine components, cylinder bores, and exhaust systems to enhance fuel efficiency and reduce friction.

Beyond transport, the energy and power sector utilizes thermal spray processes to protect gas turbines, wind turbine structures, and oil and gas drilling equipment from severe erosion and biofouling. As sustainability regulations tighten globally, industries are looking for ways to prolong the lifecycle of existing mechanical machinery rather than replacing it entirely, positioning thermal spray coatings as a highly cost-effective and eco-friendly manufacturing standard.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00012684

Competitive Landscape and Key Players

The global thermal spray market is characterized by intense competition, continuous research and development, and strategic collaborations among prominent market entities. Companies are focusing on introducing eco-friendly coating powders and high-velocity oxy-fuel (HVOF) solutions to gain a competitive edge.

The key players operating significantly within this marketplace include:

3M: Renowned for its diversified technological innovations, offering specialized abrasive and materials processing solutions utilized within coating preparation.

AandA Thermal Spray Coatings, Inc.: A dedicated provider of custom thermal spray coating services, catering to specific engineering requirements across heavy industries.

Bodycote PLC: A global leader in heat treatment and thermal processing services, playing a critical role in augmenting the mechanical properties of treated components.

Chromalloy Gas Turbine LLC: Specialized in providing advanced coatings and repairs for the aerospace and energy sectors, particularly for complex gas turbine engine parts.

Fisher Barton Group: A premier manufacturer of high-wear components, utilizing thermal spray to deliver exceptional durability in agriculture and industrial applications.

HC Starck GmbH: A major supplier of high-performance technology metals and ceramic powders essential for the production of thermal spray consumables.

Hoganas AB: A pioneer in metal powder production, developing innovative alloy powders designed specifically for surface coating and thermal spraying.

Kennametal Inc.: Known for its wear-resistant materials and tooling solutions, supplying advanced carbide powders optimized for extreme industrial environments.

Linde (Praxair Surface Technologies, Inc.): A global industrial gases and coatings powerhouse, delivering comprehensive thermal spray materials, equipment, and coating services.

Oerlikon: A market leader in surface solutions (through Oerlikon Metco and Oerlikon Balzers), offering an extensive portfolio of thermal spray equipment, materials, and specialized coating services.

These companies frequently invest in expanding their regional footprints and adopting cutting-edge automated thermal spray systems to meet the complex demands of modern manufacturing facilities.

Technological Transformations

Innovation is acting as a major catalyst in the thermal spray marketplace. Conventional methods like flame spraying and wire arc spraying are increasingly being augmented or replaced by advanced techniques such as High-Velocity Oxy-Fuel (HVOF) spraying, Plasma Spraying, and Cold Spraying. Cold spray technology, in particular, is gaining immense traction due to its ability to deposit materials at temperatures well below their melting points, minimizing thermal stresses and oxidation in the final coated material. Additionally, the integration of robotics and artificial intelligence (AI) in thermal spray systems ensures precise layer thickness, uniform distribution, and reduced material wastage, boosting overall productivity and safety on the factory floor.

Future Outlook

The future of the global thermal spray market looks exceptionally promising, characterized by a transition toward smart coatings and green manufacturing. Over the next decade, the market is expected to witness increased integration of nanostructured and biomaterial-based thermal spray coatings, which offer unprecedented levels of wear and corrosion resistance. As the global energy sector pivots toward hydrogen fuel and renewable infrastructure, thermal spray applications will expand to protect fuel cells and solar power components. Furthermore, the emergence of localized, on-site automated thermal spray repair services will significantly reduce transit costs and lead times for heavy industries. Bolstered by steady digital integration and the rising demands of next-generation aerospace and electric vehicle (EV) architectures, the thermal spray industry is well-positioned to maintain robust momentum through 2034 and beyond.

Related Reports-

Regenerative Thermal Oxidizer Market

Military Thermal Imaging Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global landscape for health, safety, and industrial hygiene has undergone a permanent shift over the last decade. At the heart of this transformation is the manufacturing infrastructure that supports personal protective equipment (PPE). According to a comprehensive study by The Insight Partners, the automation equipment responsible for producing protective gear is experiencing substantial, sustained growth worldwide.

The Face Mask Machines Market size is expected to reach US$ 2.87 Billion by 2034 from US$ 1.32 Billion in 2025. The market is estimated to record a CAGR of 9.01% from 2026 to 2034. This steady expansion highlights a transition from the chaotic, demand-driven spikes of the early 2020s to a structured, highly regulated, and technologically advanced industrial market.

Market Drivers and Industrial Shifts

The sustained demand for face mask machines is fueled by several critical factors across healthcare, manufacturing, and consumer sectors. Following global health crises, governments and healthcare regulatory bodies worldwide implemented strict mandates regarding national stockpiles and localized production capabilities. To reduce reliance on single-source supply chains, many countries have heavily incentivized the establishment of domestic mask manufacturing facilities.

Furthermore, industrial safety regulations have tightened considerably. Sectors such as semiconductor manufacturing, pharmaceuticals, biotechnology, and chemical processing require ultra-clean environments. Workers in these industries must use specialized respirators and surgical masks daily to prevent cross-contamination and protect themselves from hazardous airborne particulates. This consistent industrial consumption creates a highly predictable and recurring demand for mask manufacturers, who in turn must upgrade their machinery to maintain high-volume outputs.

Technological advancements in the machinery itself are also accelerating market growth. Modern face mask machines are no longer simple mechanical presses; they are highly integrated, fully automated systems utilizing ultrasonic welding, advanced PLC (Programmable Logic Controller) units, and high-speed rotary cutting mechanisms. These upgrades allow manufacturers to significantly reduce labor costs, minimize material waste, and ensure strict compliance with international quality standards like CE and FDA certifications.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00010610

Key Market Players

The global market features a diverse mix of specialized engineering firms, automation experts, and textile machinery manufacturers. These companies focus on increasing production speeds, enhancing machine reliability, and offering versatile lines capable of manufacturing various mask styles—such as 3-ply surgical masks, N95/KN95 respirators, and duckbill designs.

Prominent players operating in the face mask machines market include:

Aman Impex

Arora Industries

Cera Engineering

Intouch Resources Private Limited

KP Tech Machine Private Limited

NCM Nonwoven Converting Machinery Co., Ltd.

Sheetal Enterprises

Sri Sastha Engineering

TESTEX Textile Testing Instruments

TRM-Top Rank Machinery Inc.

These manufacturers are increasingly focusing on research and development to introduce modular machine designs. Modular systems allow factory owners to easily switch production lines between different types of masks with minimal downtime, providing the agility needed to respond to changing market demands.

Segmentation and Regional Landscape

The face mask machines market is typically segmented by machine type (fully automatic vs. semi-automatic) and mask type (surgical, respirator, and others). Fully automatic machines dominate the market share in developed regions due to the high cost of manual labor and the demand for extreme precision. These systems handle everything from non-woven fabric feeding, nose-bridge wire insertion, and pattern folding to ear-loop welding and final stacking without human intervention.

Geographically, the Asia-Pacific region remains both the largest producer and a massive consumer of these machines. Countries like China, India, and Taiwan boast robust textile and automation ecosystems, allowing them to produce high-quality manufacturing equipment cost-effectively. Meanwhile, North America and Europe are witnessing a surge in the adoption of high-tech, fully automated lines as they look to secure domestic supply chains and meet stringent safety certifications.

Future Outlook

Looking ahead, the future of the face mask machines market lies in the deep integration of Smart Manufacturing and Industry 4.0 technologies. The next generation of machinery will increasingly feature IoT (Internet of Things) sensors capable of real-time data tracking, predictive maintenance, and remote troubleshooting, which drastically reduces unexpected factory downtime. As sustainability becomes a core focus across all manufacturing sectors, equipment builders will likely redesign systems to seamlessly handle eco-friendly, biodegradable, and recyclable non-woven materials without sacrificing production speed or structural integrity. Driven by continuous automation upgrades, strict global workplace safety mandates, and a collective push for localized supply security, the market is well-positioned for steady, high-tech evolution over the next decade.

Related Reports-

Insulation Blowing Machines Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

Road safety has historically stood as a cornerstone of automotive innovation, but the modern era is shifting the focus from purely structural crash protection to proactive, intelligent prevention. At the heart of this transformation is the integration of advanced in-cabin electronics designed to protect drivers from their own physiological limits. As vehicles become increasingly autonomous, understanding the real-time cognitive and physical state of the person behind the wheel has grown from a premium novelty into a fundamental necessity. This shift is fueling unprecedented expansion within the global automotive driver state monitor systems (DMS) industry.

Market Valuation and Growth Trajectory

According to comprehensive research by The Insight Partners, the Automotive Driver State Monitor Systems Market size is expected to reach US$ 8.09 Billion by 2034 from US$ 2.99 Billion in 2025. This rapid expansion is estimated to record a CAGR of 13.25% from 2026 to 2034.

This multi-billion-dollar surge underscores a critical realization across the global supply chain: local and global transportation networks cannot safely transition to semi-autonomous driving without robust human-to-machine handoff mechanisms. The multi-fold leap in market capitalization reflects deep-tier investments from automakers who are standardizing hardware suites such as near-infrared (NIR) cameras, time-of-flight sensors, and steering column strain gauges directly into high-volume consumer vehicle platforms.

Key Market Drivers and Technological Catalysts

The primary mechanism propelling this market forward is a strict regulatory landscape. Government bodies worldwide have recognized that driver fatigue, micro-sleeps, and mobile device distractions are leading contributors to highway fatalities. In response, rigorous safety frameworks such as the European New Car Assessment Programme (Euro NCAP) and updated European General Safety Regulations have established stringent guidelines that effectively mandate driver monitoring technologies for new vehicle type approvals.

Technologically, the industry has evolved past primitive touch-based sensors on steering wheels. Modern driver state monitors rely heavily on Edge Artificial Intelligence (AI) and advanced computer vision architectures.Software layers can continuously map facial landmarks to compute eye-closure durations (PERCLOS), monitor gaze vector deviations, and trace erratic head positioning. If a driver looks away from the forward roadway for a dangerous interval, or if eyelid drooping patterns reflect deep cognitive fatigue, the system instantly triggers layered haptic, visual, or acoustic alerts. Furthermore, the introduction of Level 2 and Level 3 conditional driving automation requires these systems to verify "driver availability" before the vehicle passes operational control back to the human operator.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00026383

Competitive Landscape: Key Industry Players

The ecosystem comprises a specialized blend of tier-1 automotive suppliers, semiconductor manufacturers, and specialized software developers cooperating to engineer seamless in-cabin monitoring experiences.

Key players shaping the competitive dynamics of this market include:

Aptiv – A global technology leader delivering end-to-end vehicle architecture solutions, heavily focused on integrating scalable cabin sensing suites with advanced safety domain controllers.

VALEO – A pioneering tier-1 supplier known for its comprehensive driving assistance systems and interior intuitive controls optimized for real-time occupant tracking.

Veoneer Inc. – A specialized hardware and software provider dedicated to active safety and restraint control systems tailored for highly automated vehicles.

Renesas – A leading semiconductor supplier offering powerful, automotive-grade system-on-chips (SoCs) and microcontrollers optimized for processing complex computer vision pipelines at the edge.

PathPartner Technology Inc. – An embedded engineering firm providing high-performance, intelligent vision algorithms designed for low-footprint hardware deployments.

STMicroelectronics – A global semiconductor giant supplying high-dynamic-range global shutter image sensors that allow cameras to read facial geometry under highly volatile cabin lighting conditions.

Tata Elxsi – An engineering and design service provider focused on customizing, testing, and integrating deep learning models into next-generation ADAS and cabin software frameworks.

UniMax Electronics Inc. – An innovative developer of advanced in-vehicle infotainment and telematics hardware architectures that readily bridge driver monitoring data with cloud analytics platforms.

Affectiva – A pioneer in Human Perception AI, focusing on deep learning architectures capable of understanding complex cognitive states, emotional expressions, and subtle behavioral shifts.

Tobii Tech – The global leader in eye-tracking technology, providing specialized gaze-tracking platforms that unlock extreme precision in mapping exactly where a driver's attention is focused.

Future Outlook

Looking toward the horizon, the automotive driver state monitor systems market is on track to transcend basic hazard warnings and mature into a highly contextualized, holistic health-and-wellness hub. Future iterations will progressively incorporate multi-modal biometric fusion blending non-contact optical cameras with hidden physiological radar sensors to actively cross-reference heart-rate variability and respiration changes alongside visible fatigue cues. Concurrently, the integration of Large Language Models (LLMs) and conversational AI into vehicle cockpits will enable cars to respond to an impaired driver not with jarring buzzers, but with supportive, intelligent interventions such as adjusting cabin temperatures, playing stimulating audio, or suggesting nearby rest stops. As data privacy structures tighten and processing architectures migrate fully to the edge, these systems will ultimately transform the modern vehicle into an empathetic, highly secure sanctuary capable of actively protecting life on every mile of the journey.

Related Reports-

Marine Engine Monitoring System Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

The global automotive sector is undergoing a massive paradigm shift, leaving internal combustion engine (ICE) vehicles behind in favor of electrification. At the absolute core of this electric vehicle (EV) revolution lies the infrastructure that powers it both off-board and on-board. While public fast-charging networks capture major headlines, the technology tucked quietly inside the vehicle plays an equally vital role in daily usability. An on-board charger (OBC) converts alternating current (AC) from residential or commercial power sources into the direct current (DC) needed to replenish the car's battery pack. As automakers race to optimize charging speeds, minimize vehicle weight, and improve overall energy efficiency, this specific component has emerged as a high-stakes arena for technological innovation.

Explosive Market Valuation and Strategic Projections

According to comprehensive industry data, the financial and structural growth of this ecosystem is moving at an incredible pace. The EV On-Board Chargers Market size is expected to reach US$ 25.44 Billion by 2034 from US$ 7.86 Billion in 2025. This massive expansion highlights a robust trajectory, with the market anticipated to register a CAGR of 13.94% during the forecast period 2026–2034.

This multi-billion-dollar valuation is heavily driven by a compound increase in consumer adoption alongside strict global zero-emission mandates. Governments worldwide are enforcing aggressive timelines to phase out fossil-fuel-powered transport, which forces automotive original equipment manufacturers (OEMs) to scale up their electric offerings rapidly. Consequently, the demand for reliable, high-performing OBCs has transitioned from a niche automotive sub-segment into a baseline necessity for modern automotive manufacturing pipelines.

Crucial Catalysts Driving Core Industry Expansion

Several interconnected variables are fueling this 13.94% compound annual growth rate. First and foremost is the universal push toward resolving "range anxiety" and charging friction. Modern consumers expect their electric vehicles to charge safely, reliably, and rapidly overnight without overloading domestic electrical grids. To accommodate this, there is a distinct technological shift toward higher-capacity on-board chargers moving away from traditional low-power 3.7 kW variants toward 11 kW and 22 kW three-phase systems. Higher capacity OBCs drastically cut down AC charging times, making plug-in hybrid electric vehicles (PHEVs) and battery electric vehicles (BEVs) far more practical for everyday households.

Furthermore, the rise of bidirectional charging specifically Vehicle-to-Grid (V2G) and Vehicle-to-Home (V2H) systems is fundamentally redefining what an on-board charger can do. Rather than acting as a simple one-way power siphon, modern OBCs are evolving into intelligent energy management hubs. They allow vehicles to dump excess battery power back into a home during peak grid hours or sell energy back to utility providers. This turning point transforms an electric car into a mobile power bank, heavily incentivizing consumers and fleet managers to adopt next-generation EV platforms.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00022371

Dominant Key Players Shaping the Competitive Landscape

The global landscape features an intense mix of legacy automotive component giants, specialized power electronics manufacturers, and cutting-edge semiconductor innovators. These entities are consistently investing in research and development to reduce the physical footprint of the chargers while boosting their total power density.

The prominent key players driving innovation and distribution across the market include:

Bel Fuse Inc.

BorgWarner Inc.

BRUSA Elektronik AG

Current Ways

Eaton Corporation

Infineon Technologies AG

Innoelectric AG

Stercom Power Solutions GmbH

TOYOTA INDUSTRIES CORPORATION

Xepics Ltd

These market participants are highly focused on vertical integration and strategic partnerships. For instance, semiconductor leaders like Infineon work closely with power system developers to supply advanced Wide Bandgap (WBG) materials, ensuring that the hardware rolling off assembly lines can withstand higher thermal thresholds and deliver unmatched efficiency.

Technological Metamorphosis: Silicon Carbide (SiC) and GaN

The underlying architecture of EV on-board chargers is experiencing a profound material evolution. For years, traditional silicon-based transistors were the standard choice for power conversion. However, silicon is rapidly hitting its physical limits regarding efficiency, heat dissipation, and switching frequencies.

To break past these performance bottlenecks, tier-1 suppliers and key players are rapidly pivoting to Silicon Carbide (SiC) and Gallium Nitride (GaN) power semiconductors. These wide bandgap materials allow the OBC to operate at significantly higher voltages and temperatures while suffering minimal energy loss during the AC-to-DC conversion process. By deploying SiC-based architectures, engineering teams can shrink the physical size and weight of the charger by up to 50%. In the automotive world, less weight directly translates to extended driving range and better vehicle dynamics, giving SiC-equipped OEMs a powerful competitive edge.

Future Outlook

Looking down the road, the future of the EV on-board chargers market will be defined by extreme integration, high-voltage vehicle architectures, and intelligent power management. As the automotive industry shifts decisively from 400V toward ultra-fast 800V electrical systems, OBCs must evolve to handle these higher loads smoothly without driving up component costs. We will likely see the widespread adoption of "all-in-one" powertrain designs, where the on-board charger, DC-DC converter, and traction inverter are completely integrated into a single, highly compact enclosure. This modular design radically simplifies vehicle assembly, reduces wiring complexity, and lowers production overhead for automakers. Supported by intelligent grid systems and the mass roll-out of bidirectional V2X capabilities, the on-board charger will soon transcend its basic utility role, cementing its place as a critical cornerstone of both clean transportation and the global smart energy infrastructure.

Related Reports-

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876