Blogs

Film photography continues to grow in popularity as photographers and hobbyists rediscover the unique character and timeless appeal of analog images. However, preserving old negatives and transforming them into digital files requires the right tools and knowledge. Understanding what are film negatives, learning how to scan negatives, and selecting the best budget film scanner 2026 can help you create high-quality digital archives without spending a fortune.

In this guide, we’ll explore everything you need to know about film negatives, scanning techniques, and how to choose the best film scanner 2026 for your needs.

What Are Film Negatives?

Before learning how to scan negatives, it is important to understand what are film negatives. Film negatives are photographic images captured on film where the colors and brightness values are reversed. Light areas appear dark, and dark areas appear light.

These negatives serve as the original source material from which photographs are printed or digitized. Film negatives are available in various formats, including:

- 35mm film negatives

- Medium format negatives

- Large format negatives

- Black-and-white negatives

- Color negatives

- Slide film (positives)

Because negatives contain a significant amount of image detail, digitizing them correctly can preserve memories and create high-resolution digital files for sharing, editing, and storage.

Why Digitize Film Negatives?

Many photographers and families have collections of negatives stored in boxes, albums, or archives. Digitizing these negatives provides several advantages:

Long-Term Preservation

Film can degrade over time due to moisture, dust, and environmental conditions. Scanning helps preserve images before damage occurs.

Easy Sharing

Digital files can be shared instantly with family, friends, clients, and social media audiences.

Better Organization

Digital archives are easier to search, categorize, and back up compared to physical film storage.

Photo Restoration

Once scanned, images can be restored using editing software to remove scratches, fading, and dust.

This is why many photographers are searching for the best film scanner 2026 to protect their valuable collections.

How to Scan Negatives Properly

One of the most common questions among beginners is how to scan negatives effectively while maintaining image quality.

Step 1: Clean the Negatives

Before scanning, carefully remove dust and debris from the film.

Useful cleaning tools include:

- Air blowers

- Anti-static brushes

- Microfiber cloths

- Film cleaning solutions

Clean negatives produce significantly better scan results.

Step 2: Choose the Right Scanner

Selecting the proper scanner is essential. The best budget film scanner 2026 should offer:

- High optical resolution

- Color correction capabilities

- Film holders

- Dust removal technology

- User-friendly software

The right scanner helps maximize image quality while simplifying the scanning process.

Step 3: Insert the Film Correctly

Most dedicated film scanners include holders that keep negatives flat and properly aligned.

Proper positioning prevents:

- Cropped images

- Distortion

- Focus issues

- Uneven lighting

Step 4: Select Scan Settings

When learning how to scan negatives, scan settings play a major role in final image quality.

Recommended settings include:

- Resolution: 2400–6400 DPI

- Color depth: 48-bit color

- File format: TIFF for archival quality

- JPEG for everyday sharing

Higher resolutions preserve more detail for future editing and printing.

Step 5: Preview and Adjust

Most scanner software allows users to preview images before final scanning.

Adjust:

- Brightness

- Contrast

- Exposure

- Color balance

- Cropping

Proper adjustments can dramatically improve scan quality.

Step 6: Convert Negative to Positive

After scanning, software automatically converts the negative image into a normal photograph.

Advanced scanning software often includes:

- Color restoration

- Automatic correction

- Dust removal

- Scratch reduction

Step 7: Save and Back Up Files

Always store scans in multiple locations:

- External hard drives

- Cloud storage

- NAS systems

- Backup servers

This ensures long-term protection of your digital archive.

Features to Look for in the Best Budget Film Scanner 2026

Finding the best budget film scanner 2026 requires balancing performance and affordability.

High Optical Resolution

Resolution determines how much detail is captured.

Recommended optical resolutions:

- Entry-level: 2400 DPI

- Mid-range: 3600 DPI

- Advanced: 6400 DPI+

Higher resolution scanners are ideal for enlargements and professional restoration projects.

Dynamic Range

Dynamic range affects shadow and highlight detail.

A scanner with strong dynamic range preserves subtle details that may otherwise be lost.

Fast Scanning Speeds

Users digitizing large collections benefit from faster scanning performance.

Features that improve efficiency include:

- Batch scanning

- Automatic frame detection

- Multi-frame holders

Image Enhancement Tools

Modern scanners often provide:

- Infrared dust removal

- Color restoration

- Grain reduction

- Scratch correction

These features save time during post-processing.

Software Compatibility

The best film scanner 2026 should support:

- Windows

- macOS

- Modern image editing workflows

Reliable software significantly improves the scanning experience.

Best Uses for Film Scanners

The best budget film scanner 2026 can serve a variety of purposes.

Family Photo Preservation

Many families possess decades of negatives containing valuable memories.

Digitization protects these images from deterioration.

Professional Photography Archives

Photographers often maintain extensive film collections.

Scanning allows easy access to historical work while creating backup copies.

Historical Preservation

Museums, libraries, and archives regularly digitize negatives to preserve cultural history.

Creative Projects

Artists frequently incorporate scanned negatives into:

- Fine art projects

- Mixed media work

- Digital editing workflows

- Commercial photography

Dedicated Film Scanners vs Flatbed Scanners

When researching the best film scanner 2026, you’ll encounter two primary categories.

Dedicated Film Scanners

Advantages:

- Higher image quality

- Better sharpness

- Superior color accuracy

- Optimized for negatives

Best for serious film photographers.

Flatbed Scanners

Advantages:

- Lower cost

- Multi-purpose functionality

- Ability to scan documents and photos

Ideal for casual users seeking a best budget film scanner 2026 solution.

Common Mistakes When Learning How to Scan Negatives

Many beginners make avoidable errors while learning how to scan negatives.

Scanning at Low Resolution

Low-resolution scans limit future editing and printing possibilities.

Always scan at the highest practical resolution.

Ignoring Film Cleaning

Dust becomes highly visible during scanning.

Thorough cleaning improves image quality significantly.

Using Automatic Settings Only

Automatic corrections can occasionally produce inaccurate colors.

Manual adjustments often yield superior results.

Saving Only JPEG Files

JPEG compression reduces image quality.

For archival purposes, save master files in TIFF format.

Poor Storage Practices

Always maintain multiple backups of scanned files.

Digital preservation is just as important as physical preservation.

How Modern Technology Improves Film Scanning

The latest scanners have evolved dramatically compared to older models.

Modern innovations include:

- AI-powered color correction

- Advanced dust detection

- Improved dynamic range

- Faster processing speeds

- Better software integration

These advancements help users achieve professional-quality results with the best budget film scanner 2026 while keeping costs manageable.

Choosing the Best Film Scanner 2026 for Your Needs

Not every scanner suits every photographer.

Consider the following factors:

Casual Users

Look for:

- Affordable pricing

- Easy operation

- Automatic corrections

A reliable best budget film scanner 2026 option may be sufficient.

Enthusiasts

Prioritize:

- Higher resolution

- Better color accuracy

- Manual controls

Professionals

Focus on:

- Maximum image quality

- Superior dynamic range

- Advanced software tools

The best film scanner 2026 for professionals should deliver archival-grade results and extensive workflow flexibility.

Future Trends in Film Digitization

Film photography continues to maintain a loyal following, and scanner technology is evolving accordingly.

Emerging trends include:

- Cloud-connected scanning workflows

- AI-assisted restoration

- Faster batch processing

- Enhanced color science

- Automated archival systems

These developments make preserving film collections easier and more efficient than ever before.

Conclusion

Understanding what are film negatives is the first step toward preserving valuable photographic memories. Once you know how to scan negatives, you can transform aging film archives into high-quality digital collections that remain accessible for generations.

Whether you’re preserving family photos, organizing a professional archive, or exploring analog photography, selecting the best budget film scanner 2026 can provide outstanding results without exceeding your budget. As technology continues to improve, the best film scanner 2026 options offer better image quality, faster workflows, and smarter restoration tools than ever before.

Investing in the right scanner today ensures that your treasured negatives remain protected, organized, and ready to enjoy for years to come.

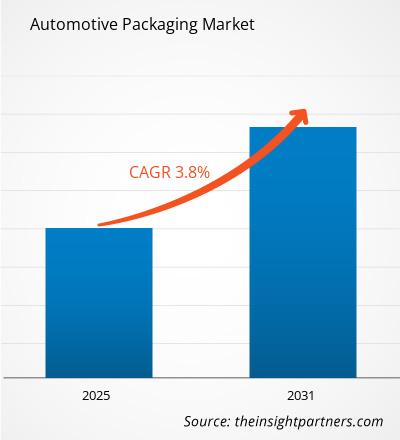

Automotive Packaging Market Share Analysis Expanding at 4.50% CAGR to 13.18 Billion USD 2034

By sammkaran, 2026-06-26

The automotive manufacturing sector relies on a highly complex, interconnected global supply chain where millions of components ranging from heavy steel engines to microscopic electronic sensors must be transported safely across continents. As vehicle designs shift toward advanced electronics and electrification, the protective systems handling these components are undergoing a parallel evolution.

The Automotive Packaging Market size is expected to reach US$ 13.18 Billion by 2034 from US$ 9.27 Billion in 2025. The market is estimated to record a CAGR of 4.50% from 2026 to 2034. This steady expansion underscores the crucial role that specialized logistics and packaging solutions play in modern automotive manufacturing and the aftermarket sector.

Key Drivers Shaping the Market

Several macroeconomic and industry-specific shifts are steering the development of the automotive packaging sector:

-

The Transition to Electric Vehicles (EVs): Unlike traditional internal combustion engines, electric vehicles depend on massive, highly sensitive lithium-ion battery packs, power electronics, and intricate wiring systems. These components require unique packaging solutions that offer thermal insulation, impact resistance, and compliance with stringent international regulations for hazardous materials.

-

Rising Electronic Complexity: The integration of Advanced Driver Assistance Systems (ADAS), autonomous driving technologies, and infotainment screens has turned modern cars into computers on wheels. Fragile semiconductor-based parts are highly vulnerable to electrostatic discharge (ESD), moisture, and physical vibrations during transit. Protective packaging using specialized anti-static films, custom molded foam, and robust cushioning is vital to prevent multi-million dollar supply chain losses.

-

The Push for Circular Economies: Automakers are facing heavy pressure from regulatory frameworks and internal corporate social responsibility (CSR) targets to reduce their carbon footprint. This has accelerated the transition from single-use, disposable packaging to returnable and reusable systems. Reusable plastic crates, steel racks, and bulk containers offer long-term cost efficiencies and minimize waste.

-

Just-In-Time (JIT) Manufacturing: To save on warehousing costs, original equipment manufacturers (OEMs) operate on tight JIT delivery schedules. Packaging must be standardized, modular, easily stackable, and collapsible when empty to maximize shipping container space and optimize inbound and outbound logistics.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00026590

Material and Segment Insights

The global market features a balanced blend of rigid, flexible, and corrugated solutions designed to handle specific component categories:

-

Rigid Packaging (Crates, Pallets, and Racks): Heavy components like engines, gearboxes, and suspension systems are transported via heavy-duty, reusable plastic and steel racks. These provide maximum structural protection and are built to handle multiple round trips across supply chain routes.

-

Corrugated Solutions: Corrugated cardboard boxes and die-cut custom packaging remain highly popular for medium and small-sized spare parts due to their lightweight properties and high recyclability. Advanced corrugated designs offer strong barrier properties and shock resistance at lower initial costs.

-

Flexible and Protective Packaging: Bubble wraps, expanded polypropylene (EPP) foam inserts, and protective pouches are critical layers within outer boxes. They shield sensitive surfaces from scratches and absorb transit vibrations, ensuring components arrive at the assembly line in pristine condition.

Competitive Landscape

The automotive packaging industry is highly competitive, with global and regional players continuously innovating to introduce lighter, stronger, and more sustainable materials. Companies focus on strategic partnerships with OEMs and invest heavily in localized fabrication to meet precise geometric requirements for vehicle parts.

Key players driving innovation and operational scale within the market include:

-

Nefab Group

-

New-Tech Packaging

-

Kronus

-

D S Smith

-

Victory Packaging

-

Schoeller Allibert

-

Orcon Industries

-

PRIMO

-

Robinson Industries

-

THIMM Group

Future Outlook

The future of the automotive packaging market will be defined by smart technology and deep sustainability integration. We can expect a significant increase in the adoption of "smart packaging" systems embedded with RFID tags, IoT sensors, and GPS trackers. These technologies will allow logistics managers to monitor the precise location, temperature, and shock exposure of high-value parts like EV batteries in real time. Furthermore, innovations in bio-based plastics and high-strength, lightweight paper composites will help manufacturers satisfy stringent global eco-regulations while driving down shipping weights. As global vehicle production volumes stabilize and move deeper into the electric era, packaging will cease to be treated as a mere transit cost and will instead become a core pillar of lean, digitalized, and green automotive logistics.

Related Reports-

Flexible Packaging Solutions Market

Temperature Controlled Packaging Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

Business Incorporation in Dubai: A Step-by-Step Guide to Launching Your Business Successfully

By Stratrich, 2026-06-26

Dubai has earned its reputation as one of the world's most dynamic business destinations. From ambitious startups to global corporations, thousands of entrepreneurs choose the emirate every year because of its strategic location, modern infrastructure, and business-friendly environment. If you're planning to establish a company in the UAE, understanding the process of Business Incorporation in Dubai is the first step toward building a successful venture.

While the opportunities are enormous, the incorporation process involves several legal, regulatory, and administrative requirements. Working with an experienced consulting partner like Stratrich can make the journey smooth, efficient, and stress-free.

Why Dubai Is a Global Business Hub

Dubai offers much more than an attractive skyline. It provides an ecosystem where businesses can thrive across industries such as technology, trading, manufacturing, healthcare, logistics, finance, and professional services.

Entrepreneurs are drawn to Dubai because of:

- Strategic access to markets across Europe, Asia, and Africa

- Business-friendly regulations

- World-class infrastructure

- Competitive tax environment

- Advanced banking and financial systems

- Diverse and highly skilled workforce

These advantages have made Dubai one of the preferred destinations for investors looking to expand internationally.

What Is Business Incorporation in Dubai?

Business Incorporation in Dubai refers to the legal process of establishing a company that is officially recognized by the UAE authorities. This process involves selecting the right business activity, choosing the appropriate jurisdiction, obtaining a trade license, and fulfilling all regulatory requirements before beginning operations.

Every business has unique objectives, which is why incorporation should never be treated as a one-size-fits-all process. Choosing the correct structure from the beginning can save both time and money in the future.

Choosing the Right Business Structure

One of the first decisions you'll make is selecting where your company will be incorporated.

Mainland Company

A mainland company offers flexibility to operate across the UAE and work with government and private-sector clients. It is often the preferred option for businesses planning long-term expansion.

Free Zone Company

Free Zones are popular among startups and international investors because they offer simplified incorporation procedures, industry-focused ecosystems, and attractive ownership benefits.

Offshore Company

Offshore incorporation is suitable for businesses looking to manage international operations or hold assets while benefiting from an efficient corporate structure.

At Stratrich, our consultants evaluate your business goals before recommending the most suitable incorporation route.

The Business Incorporation Process

Many entrepreneurs assume company registration is simply about obtaining a trade license. In reality, successful Business Incorporation in Dubai involves several carefully coordinated steps.

The process typically includes:

- Understanding your business objectives

- Selecting the appropriate jurisdiction

- Choosing the legal structure

- Reserving a company name

- Preparing incorporation documents

- Applying for the required trade license

- Obtaining government approvals

- Processing investor and employee visas

- Opening a corporate bank account

- Meeting ongoing compliance requirements

Having experienced professionals manage these steps significantly reduces delays and administrative challenges.

Why Professional Guidance Matters

Business regulations in the UAE continue to evolve, making expert advice increasingly valuable. A small mistake during incorporation can result in additional costs, licensing delays, or compliance issues later.

Professional consultants help by:

- Explaining legal requirements clearly

- Preparing accurate documentation

- Coordinating with government authorities

- Reducing processing time

- Ensuring regulatory compliance

- Providing ongoing business support

Instead of spending weeks navigating paperwork, entrepreneurs can focus on developing their products, building customer relationships, and growing their businesses.

Why Businesses Choose Stratrich

At Stratrich, we believe incorporation is just the beginning of a company's journey. Our objective is not only to register your business but also to provide the strategic support needed for sustainable growth.

Our Business Incorporation in Dubai services include:

- Business setup consultation

- Mainland company formation

- Free Zone company incorporation

- Offshore company registration

- Trade license assistance

- PRO services

- Visa processing

- Corporate banking guidance

- Regulatory advisory

- Tax and accounting support

- Corporate compliance services

Our experienced consultants work closely with entrepreneurs to recommend practical, cost-effective solutions tailored to their business goals.

Common Mistakes to Avoid

Many entrepreneurs unintentionally delay their company formation by making avoidable mistakes.

Some of the most common include:

- Choosing the wrong business activity

- Selecting an unsuitable jurisdiction

- Preparing incomplete documentation

- Underestimating licensing requirements

- Ignoring future expansion plans

- Overlooking ongoing compliance obligations

Working with experienced consultants helps eliminate these risks while ensuring every stage of incorporation is completed accurately.

More Than Company Registration

A successful business requires ongoing support long after incorporation is complete.

That's why Stratrich continues assisting clients with services such as:

- Trade license renewals

- Corporate tax guidance

- Bookkeeping and accounting

- Regulatory compliance

- Business advisory

- Expansion planning

- Corporate restructuring

Our long-term partnership approach allows entrepreneurs to focus on scaling their businesses while we handle the administrative responsibilities.

Start Your Business Journey with Confidence

Every successful company begins with a strong foundation. Whether you're a first-time entrepreneur or an established international business entering the UAE market, professional guidance can make your incorporation experience faster, simpler, and more efficient.

At Stratrich, we combine industry expertise, transparent communication, and personalized service to help businesses establish themselves confidently in Dubai. From your initial consultation to post-incorporation support, we're committed to making every step of your business journey seamless.

Conclusion

Dubai continues to offer exceptional opportunities for entrepreneurs who are ready to invest in one of the world's fastest-growing business environments. However, a successful launch depends on making informed decisions from the very beginning.

Choosing expert support for Business Incorporation in Dubai ensures your company is established correctly, complies with local regulations, and is positioned for long-term success.

With Stratrich as your trusted business partner, you gain more than incorporation services—you gain experienced advisors dedicated to helping your business grow, adapt, and succeed in the UAE's competitive marketplace.

The trucking industry continues to create opportunities for people looking for a stable and rewarding career. If you are considering a future in commercial driving, enrolling in CDL training Brownsville TX can be the first step toward achieving your goals. With growing demand for qualified drivers across Texas and the United States, earning a Commercial Driver’s License can open doors to a variety of career paths in transportation and logistics.

Whether you are researching a CDL school Brownsville TX, trying to understand what is a CDL A truck driver, comparing the cost of truck driving school, or wondering how long does it take to get your CDL license, this guide will help you understand everything you need to know before getting started.

Why Choose a Truck Driving Career?

Truck drivers play a vital role in keeping businesses and supply chains moving. Nearly every product people use daily is transported by commercial vehicles at some point. This creates a constant demand for skilled drivers who can safely and efficiently move freight across cities, states, and the country.

Some benefits of becoming a truck driver include:

- Strong job demand

- Competitive earning potential

- Opportunities for career growth

- Flexible career paths

- Ability to travel and see different places

- Short training periods compared to many other professions

For many people, truck driving offers a faster path to a new career without spending years in traditional college programs.

What Is a CDL A Truck Driver?

One of the most common questions prospective students ask is, what is a CDL A truck driver?

A CDL A truck driver is a professional driver licensed to operate combination vehicles with a gross combination weight rating of 26,001 pounds or more, provided the towed vehicle exceeds 10,000 pounds. These drivers typically operate:

- Tractor trailers

- Semi trucks

- Flatbed trucks

- Tanker trucks

- Livestock carriers

- Refrigerated freight vehicles

A Class A CDL is considered the most versatile commercial driver’s license because it qualifies drivers for a wider range of vehicles and job opportunities. Many long haul and regional trucking positions require a Class A CDL. CDL training programs focus on vehicle inspection procedures, backing maneuvers, road safety, defensive driving, and real world driving experience.

Why Enroll in CDL Training Brownsville TX?

Professional training provides the knowledge and practical experience needed to pass CDL exams and become a safe driver. Students who complete structured CDL training Brownsville TX programs often gain confidence through classroom instruction and hands on driving practice.

Brownsville is strategically located in South Texas, making it an important transportation and logistics hub. The region’s strong freight activity creates opportunities for qualified commercial drivers.

Benefits of professional CDL training include:

Hands On Experience

Students receive behind the wheel training using commercial vehicles. This practical experience helps prepare them for state CDL testing and real world driving situations.

Safety Training

Learning proper safety procedures is critical for every commercial driver. Training programs emphasize vehicle inspections, road awareness, and defensive driving techniques.

Test Preparation

CDL schools help students prepare for:

- CDL permit exams

- Pre trip inspections

- Skills testing

- Road testing

Career Readiness

Many schools provide guidance that helps students transition from training into entry level driving positions.

Finding the Right CDL School Brownsville TX

Selecting the right CDL school Brownsville TX can significantly impact your learning experience and career readiness.

When evaluating schools, consider:

Instructor Experience

Experienced instructors can provide valuable industry knowledge and practical driving tips.

Hands On Training Time

Look for programs that emphasize actual driving experience rather than only classroom instruction.

Equipment Quality

Modern trucks and training equipment can help students become familiar with the vehicles they may operate professionally.

Training Structure

Quality programs typically include:

- Classroom instruction

- Vehicle inspections

- Backing practice

- Road driving

- CDL test preparation

Several training providers in and around Brownsville offer CDL programs designed to help students prepare for commercial driving careers.

Cost of Truck Driving School

Another important question students ask is about the https://roadmastersacademy.com/how-long-does-it-take-to-get-a-cdl-licence/" class="markup--anchor markup--p-anchor" target="_blank" rel="noreferrer noopener">cost of truck driving school.

The total cost varies depending on factors such as:

- School location

- Program length

- Equipment and training resources

- Additional endorsements

- Testing fees

In Texas, CDL training programs can range from a few thousand dollars to several thousand dollars depending on the level of instruction provided. Some programs may also offer financing options or tuition assistance opportunities.

When comparing the cost of truck driving school, remember that the cheapest option is not always the best value. Consider:

- Driving hours included

- Instructor support

- Training quality

- Job placement assistance

- Testing preparation

A quality training program can provide a strong return on investment by helping graduates qualify for commercial driving opportunities more quickly.

How Long Does It Take to Get Your CDL License?

Many future drivers want to know, how long does it take to get your CDL license?

The answer depends on several factors, including:

- Training schedule

- Full time or part time enrollment

- Individual learning pace

- State testing availability

Many CDL training programs can be completed within one to two months, while others may take several weeks longer depending on the curriculum and schedule. Some intensive training programs are designed to help students prepare efficiently for CDL testing.

The typical process includes:

Step 1: Meet Eligibility Requirements

Applicants must meet state requirements regarding age, identification, and driving history.

Step 2: Obtain a Commercial Learner’s Permit

Students study CDL materials and pass written knowledge exams.

Step 3: Complete CDL Training

Professional instruction provides classroom education and practical driving experience.

Step 4: Pass Skills and Road Tests

Students demonstrate their ability to safely operate commercial vehicles.

Step 5: Receive CDL License

Upon successful completion of all requirements, drivers receive their CDL and can begin pursuing employment opportunities.

Skills You Learn During CDL Training

Professional CDL programs teach much more than simply driving a truck.

Students typically learn:

Vehicle Inspection Procedures

Pre trip inspections help identify potential safety concerns before operating a commercial vehicle.

Backing Techniques

Proper backing skills are critical for safe operation in loading docks, yards, and tight spaces.

Road Safety

Drivers learn how to navigate highways, intersections, traffic conditions, and challenging weather situations.

Vehicle Control

Training focuses on maintaining control of large commercial vehicles under various driving conditions.

Regulatory Compliance

Commercial drivers must understand transportation regulations and safety requirements.

Experienced drivers often emphasize the importance of mastering pre trip inspections early in training because it helps students focus on other important driving skills.

Career Opportunities After CDL Training

Completing CDL training Brownsville TX can lead to several career opportunities.

Common positions include:

- Local delivery driver

- Regional truck driver

- Long haul truck driver

- Flatbed driver

- Tanker driver

- Refrigerated freight driver

- Dedicated route driver

Many drivers begin with entry level positions and later move into specialized roles with additional experience and endorsements.

A Class A CDL often provides access to a broader range of transportation careers compared to other license classifications.

Tips for Success in CDL School

If you are preparing to enroll in a CDL school Brownsville TX, consider these helpful tips:

Study Consistently

Review CDL manuals regularly and prepare thoroughly for permit exams.

Practice Inspections

Understanding inspection procedures can improve confidence during testing.

Ask Questions

Take advantage of instructor knowledge and experience.

Focus on Safety

Safe driving habits developed during training can benefit you throughout your career.

Stay Committed

Consistency and practice are key to mastering commercial driving skills.

Final Thoughts

Starting a career in trucking begins with quality training and a commitment to learning. Whether you are exploring CDL training Brownsville TX, researching the best CDL school Brownsville TX, trying to understand what is a CDL A truck driver, comparing the cost of truck driving school, or asking how long does it take to get your CDL license, the right training program can help you move toward your career goals.

Commercial driving continues to offer opportunities for individuals seeking a practical career path with strong demand and long term potential. By choosing professional CDL training, gaining hands on experience, and developing safe driving habits, you can position yourself for success in the transportation industry.

Meta Title: CDL Training Brownsville TX | CDL School & License Guide

Meta Description: Learn about CDL training Brownsville TX, CDL school options, CDL A truck driver careers, truck driving school costs, and how long it takes to get your CDL license.

Dubai has established itself as a major global hub for healthcare, trade, and logistics. With world-class hospitals, specialized clinics, and advanced medical facilities continuing to expand, the demand for imported medical devices and equipment remains high. However, importing medical equipment involves much more than transportation. Medical equipment clearance Dubai is a structured process that requires compliance with customs regulations, proper documentation, and adherence to healthcare standards to ensure shipments reach their destinations without unnecessary delays. Whether importing diagnostic machines, laboratory instruments, surgical equipment, or hospital furniture, businesses must understand every stage of the clearance process. Proper planning reduces risks, minimizes costs, and ensures that essential medical equipment reaches healthcare providers on time. This guide explores the key considerations that businesses should keep in mind when handling medical equipment imports into Dubai.

Understanding Medical Equipment Clearance

Medical equipment clearance refers to the process of obtaining the necessary approvals, documentation, and customs permissions before imported medical products are released for distribution or installation.

Unlike standard commercial goods, medical equipment is subject to additional scrutiny because it directly impacts patient care and public health.

The clearance process typically involves:

- Customs documentation

- Product classification

- Regulatory compliance

- Import approvals

- Inspection procedures

- Duty and tax assessment

- Final shipment release

Each stage must be completed accurately to prevent shipment delays or compliance issues.

Why Compliance Matters

Healthcare products are regulated to ensure they meet quality and safety standards before entering the market.

Proper compliance helps achieve several important objectives:

- Protect patient safety

- Maintain product quality

- Prevent counterfeit medical products

- Ensure equipment functions correctly

- Support healthcare regulations

Failure to comply with import requirements can result in shipment delays, financial penalties, additional inspections, or even shipment rejection.

Because medical equipment often serves hospitals and emergency healthcare providers, timely clearance is especially important.

Understanding Documentation Requirements

Documentation is one of the most critical aspects of successful imports.

Although specific requirements may vary depending on the equipment type, importers generally prepare documents such as:

- Commercial invoices

- Packing lists

- Bill of lading or airway bill

- Certificate of origin

- Import permits where applicable

- Product specifications

- Manufacturer documentation

Accuracy is essential. Even minor inconsistencies between shipping documents can create unnecessary delays during customs processing.

Maintaining organized documentation also simplifies future imports and regulatory audits.

Accurate Product Classification

Every imported product must be assigned the correct customs classification.

Medical equipment includes a wide variety of products, including:

- Imaging systems

- Diagnostic instruments

- Surgical devices

- Patient monitoring equipment

- Laboratory machinery

- Rehabilitation equipment

- Sterilization systems

Each category may fall under different tariff codes and regulatory requirements.

Proper classification helps ensure:

- Correct duty calculations

- Appropriate inspections

- Faster customs processing

- Regulatory compliance

Incorrect classifications can result in penalties or shipment delays.

Importance of Regulatory Approvals

Many medical products require approvals before they can be imported or distributed.

Regulatory review often focuses on:

- Product safety

- Intended medical use

- Manufacturing standards

- Technical documentation

- Product certifications

Businesses should verify approval requirements before arranging shipment.

Obtaining required approvals in advance significantly reduces the likelihood of customs complications.

Working with Experienced Customs Professionals

Medical imports involve complex procedures that extend beyond standard cargo clearance.

Experienced customs professionals assist with:

- Documentation review

- Customs declarations

- Product classification

- Regulatory coordination

- Inspection scheduling

- Shipment tracking

A knowledgeable Dubai Customs Broker can help businesses navigate evolving import requirements while minimizing delays.

Professional support is especially valuable for first-time importers or companies handling specialized medical equipment.

Managing Customs Inspections

Some shipments may be selected for customs inspection.

Inspections help verify:

- Shipment contents

- Product descriptions

- Documentation accuracy

- Regulatory compliance

- Packaging integrity

Proper preparation allows inspections to proceed efficiently.

Importers should ensure that:

- Labels match documentation.

- Packaging protects sensitive equipment.

- Serial numbers are properly recorded.

- Technical documents are available if requested.

Preparation reduces inspection time and facilitates quicker shipment release.

Packaging and Transportation Considerations

Medical equipment often includes sophisticated electronics and precision components.

Proper packaging protects equipment from:

- Moisture

- Dust

- Vibration

- Temperature fluctuations

- Physical impact

Sensitive devices may require specialized shipping conditions throughout transportation.

Importers should also verify that packaging complies with international shipping standards while protecting equipment during customs handling.

Damaged equipment can create significant financial losses and delay healthcare operations.

Temperature-Controlled Medical Equipment

Certain medical products require strict environmental control throughout transportation.

Examples include:

- Diagnostic reagents

- Laboratory supplies

- Specialized medical devices

- Sensitive electronic equipment

Maintaining proper environmental conditions helps preserve product integrity.

Temperature monitoring, protective packaging, and proper handling procedures all contribute to successful imports.

Planning these logistics before shipment departure helps prevent costly complications upon arrival.

Importance of Timely Clearance

Medical equipment frequently supports critical healthcare services.

Delays can affect:

- Hospital expansion projects

- Laboratory operations

- Surgical scheduling

- Patient diagnostics

- Emergency healthcare services

Efficient medical equipment clearance Dubai minimizes disruptions and helps healthcare providers maintain uninterrupted operations.

Proper planning, complete documentation, and regulatory compliance all contribute to faster clearance times.

Understanding Duties and Import Costs

Importing medical equipment involves several potential costs beyond transportation.

Businesses should budget for:

- Customs duties where applicable

- Administrative fees

- Inspection charges

- Storage costs

- Documentation expenses

- Logistics coordination

Understanding these costs before shipment arrival improves financial planning and prevents unexpected expenses.

Working closely with customs professionals helps ensure accurate cost estimation.

Digital Transformation in Customs Clearance

Modern customs operations increasingly rely on digital systems to improve efficiency.

Electronic processing offers several advantages:

- Faster document submission

- Improved shipment tracking

- Reduced paperwork

- Better communication

- Enhanced transparency

Digital customs platforms also reduce processing errors by improving document accuracy and accessibility.

Importers who prepare digital documentation in advance often experience smoother clearance procedures.

Risk Management During Medical Equipment Imports

Every international shipment carries potential risks.

Common challenges include:

- Documentation errors

- Regulatory changes

- Shipping delays

- Customs inspections

- Packaging damage

- Classification issues

Effective risk management begins long before the shipment reaches Dubai.

Businesses should establish procedures for:

Documentation Verification

Review every document carefully before shipment departure to identify discrepancies early.

Regulatory Monitoring

Import requirements may change over time. Staying informed helps businesses remain compliant.

Logistics Planning

Working with experienced logistics partners reduces transportation risks and improves shipment visibility.

Customs Coordination

A qualified Dubai Customs Broker helps ensure customs declarations are completed accurately while coordinating with relevant authorities throughout the clearance process.

Best Practices for Smooth Medical Equipment Imports

Organizations can improve import efficiency by following several practical strategies.

Plan Ahead

Begin documentation and approval processes well before shipment departure.

Early preparation reduces last-minute complications.

Maintain Complete Records

Organized records simplify future imports and facilitate regulatory reviews.

Maintain documentation for:

- Product specifications

- Import approvals

- Shipping records

- Customs declarations

- Inspection reports

Verify Supplier Information

Accurate supplier documentation helps ensure customs records remain consistent throughout the import process.

Coordinate with Logistics Providers

Communication between suppliers, freight providers, customs professionals, and importers helps prevent misunderstandings and delays.

Monitor Shipment Progress

Tracking shipments throughout transportation allows businesses to anticipate arrival dates and prepare customs documentation accordingly.

Supporting Dubai's Expanding Healthcare Sector

Dubai continues to invest heavily in healthcare infrastructure.

Growing demand exists for:

- Advanced diagnostic systems

- Surgical technology

- Medical laboratories

- Specialized treatment centers

- Rehabilitation facilities

Efficient medical equipment clearance Dubai supports these developments by ensuring healthcare providers receive essential equipment without unnecessary delays.

Reliable import processes contribute to stronger healthcare delivery while supporting the city's long-term medical expansion.

As healthcare technology continues to evolve, businesses importing advanced equipment must remain prepared for changing regulations and increasingly sophisticated customs procedures.

Partnering with an experienced Dubai Customs Broker provides valuable expertise in managing these complexities while maintaining regulatory compliance throughout the import process.

Final Thought

Medical equipment imports require careful planning, accurate documentation, and thorough compliance with customs and regulatory requirements. Successful medical equipment clearance Dubai depends on preparation, attention to detail, and effective coordination across the entire supply chain. By working closely with knowledgeable professionals, including an experienced Dubai Customs Broker, businesses can streamline the import process, reduce delays, and ensure critical medical equipment reaches healthcare facilities safely and efficiently.

Parents always want the very best for their children, especially when it comes to their health and well-being. One important aspect that often deserves extra attention is child’s skin care. Children’s skin is naturally softer, thinner, and more delicate than adult skin, making it more sensitive to environmental factors, weather changes, and harsh ingredients. Along with proper hair care for kids, maintaining a gentle daily routine can help children stay comfortable while supporting healthy skin and hair development.

Choosing products specifically designed for young skin is essential. Whether you’re looking for a gentle kids face cleanser or exploring thoughtful skincare gifts sets, understanding your child’s skincare needs makes it easier to establish healthy habits that last a lifetime.

Why Child’s Skin Needs Special Care

A child’s skin continues developing throughout the early years. Because the protective skin barrier is still maturing, it loses moisture more quickly and can become irritated by products formulated for adults.

Practicing proper child’s skin care helps:

- Maintain healthy moisture levels

- Protect against dryness

- Reduce irritation

- Support healthy skin development

- Keep skin feeling soft and comfortable

Developing a simple skincare routine early also encourages children to understand the importance of personal hygiene as they grow.

Understanding Skin Care for Kids

Effective skin care for kids doesn’t require complicated routines. Instead, consistency and gentle products make the biggest difference.

A basic skincare routine typically includes:

Gentle Cleansing

Children’s skin should be cleaned using mild cleansers that remove dirt, sweat, and impurities without stripping away natural oils. Washing the face after outdoor play or before bedtime helps keep skin fresh and clean.

Using a specially formulated kids face cleanser ensures that delicate facial skin remains balanced while reducing unnecessary dryness.

Daily Moisturizing

Hydration plays a major role in child’s skin care. Applying a lightweight moisturizer after bathing helps lock in moisture and supports the skin’s natural protective barrier.

Sun Protection

While skincare often focuses on cleansing and moisturizing, protecting skin from UV exposure is equally important. Applying sunscreen before outdoor activities helps reduce the effects of prolonged sun exposure.

Choosing the Right Kids Face Cleanser

Not every facial cleanser is suitable for children. Adult products may contain ingredients that are too strong for delicate skin.

A quality kids face cleanser should offer:

- Gentle cleansing

- Mild ingredients

- Soap-free formulas

- Balanced hydration

- Easy rinsing

- Suitable daily use

Children who spend time outdoors often collect dust, sweat, and environmental impurities throughout the day. A gentle facial cleanser helps remove these without causing discomfort.

Parents should encourage children to wash their face twice daily using lukewarm water and gentle circular motions.

Hair Care for Kids Starts with Healthy Habits

Healthy hair begins with proper scalp care. Just like skin, children’s scalps are sensitive and benefit from products designed specifically for them.

Effective hair care for kids focuses on maintaining cleanliness while preserving natural moisture.

Healthy habits include:

- Washing hair with mild shampoo

- Avoiding excessive washing

- Using lukewarm water

- Brushing gently

- Preventing tangles

- Keeping the scalp clean

Regular hair care for kids also helps reduce product buildup while supporting healthy-looking hair.

Building a Simple Daily Routine

Parents often wonder how much skincare children actually need. The answer is surprisingly simple.

Morning Routine:

- Wash face using a gentle kids face cleanser

- Apply moisturizer if needed

- Use sunscreen before outdoor activities

Evening Routine:

- Cleanse the face

- Remove dirt and sweat

- Apply moisturizer

- Brush hair gently before bedtime

Keeping routines short and enjoyable makes it easier for children to follow them consistently.

Common Skin Concerns in Children

Many children experience occasional skin concerns as they grow. While most are temporary, proper child’s skin care can help maintain comfort.

Some common concerns include:

Dry Skin

Dry patches may appear during colder months or after frequent bathing.

Solutions include:

- Gentle cleansers

- Regular moisturizing

- Avoiding very hot water

Sensitive Skin

Some children naturally have sensitive skin that reacts quickly to fragrances or harsh chemicals.

Parents should choose products with simple formulations designed specifically for skin care for kids.

Dirt and Sweat Buildup

Active children spend hours playing outdoors. Daily cleansing helps remove accumulated dirt while supporting healthy skin.

Seasonal Skin Care Tips

Children’s skincare needs often change throughout the year.

Summer

Higher temperatures increase sweating.

Helpful practices include:

- Gentle cleansing

- Frequent hydration

- Lightweight moisturizers

- Daily sunscreen

Winter

Cold weather can dry out delicate skin.

Parents should:

- Moisturize regularly

- Limit very hot baths

- Protect exposed skin outdoors

Adapting routines with the seasons helps maintain effective child’s skin care year-round.

Hair Care for Kids During Every Season

Seasonal weather also affects children’s hair.

During summer:

- Wash away sweat after outdoor play

- Brush regularly

- Keep hair clean

During winter:

- Prevent dryness

- Use gentle shampoos

- Avoid excessive washing

Consistent hair care for kids helps maintain healthy-looking hair regardless of the season.

Encouraging Healthy Hygiene Habits

Children often learn best through routines and positive reinforcement.

Parents can make skin care for kids enjoyable by:

- Creating morning routines

- Allowing children to participate

- Using child-friendly products

- Making skincare educational

- Leading by example

These habits often continue into adolescence and adulthood.

Why Ingredients Matter

Because children’s skin is delicate, ingredient selection is important.

Parents often prefer products that are:

- Gentle

- Dermatologically tested

- Mildly formulated

- Suitable for sensitive skin

- Free from unnecessary harsh ingredients

Selecting products made specifically for child’s skin care provides greater confidence during daily use.

Skincare Gifts Sets: A Thoughtful Choice

As children become interested in self-care, skincare gifts sets have become increasingly popular. They introduce children to healthy routines while making skincare feel fun and engaging.

Many skincare gifts sets include combinations such as:

- Gentle cleansers

- Moisturizers

- Mild shampoos

- Hair accessories

- Face towels

These sets are suitable for birthdays, holidays, celebrations, or simply encouraging good hygiene habits.

Parents also appreciate skincare gifts sets because they combine multiple everyday essentials into one convenient package.

Teaching Kids Independence Through Self-Care

As children grow older, they enjoy learning to care for themselves.

Simple tasks like:

- Washing the face

- Brushing hair

- Applying moisturizer

- Organizing skincare items

help build confidence and responsibility.

Introducing a gentle kids face cleanser alongside easy hair care for kids routines makes self-care manageable even for younger children.

Tips for Parents

When building a skincare routine, remember these practical suggestions:

- Choose products designed specifically for children.

- Keep routines simple and consistent.

- Avoid using adult skincare products on children.

- Encourage hydration throughout the day.

- Wash bedding and towels regularly.

- Maintain clean hair brushes and combs.

- Monitor skin for any signs of irritation.

- Introduce one new product at a time.

Consistency often produces better long-term results than using numerous products.

Creating Positive Daily Habits

Children respond well to routines that are easy to follow. A five-minute skincare and haircare routine every morning and evening can become an enjoyable family activity.

Combining child’s skin care, proper skin care for kids, and regular hair care for kids creates a balanced approach to personal hygiene. Over time, these habits help children become more confident in caring for themselves while keeping their skin and hair clean and comfortable.

Adding age-appropriate products such as a gentle kids face cleanser and carefully selected skincare gifts sets can make the experience even more engaging and enjoyable.

Conclusion

Healthy routines begin with simple daily habits. Proper child’s skin care focuses on gentle cleansing, hydration, and protection, while effective hair care for kids keeps the scalp and hair clean without causing dryness. Choosing products created specifically for skin care for kids helps support delicate skin and encourages children to develop lifelong hygiene practices.

Whether selecting a mild kids face cleanser for everyday use or thoughtful skincare gifts sets for a special occasion, parents can create enjoyable routines that promote healthy skin, clean hair, and growing confidence. By introducing these habits early, children learn the value of self-care in a way that is both fun and beneficial, laying the foundation for healthy skin and hair well into the future.

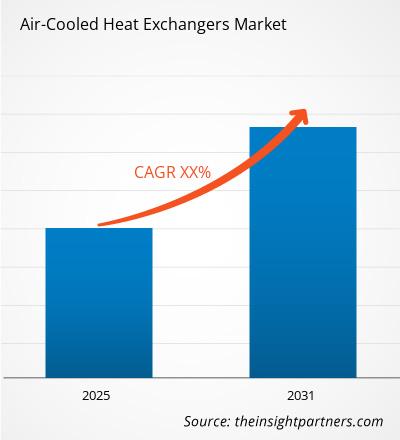

Air-Cooled Heat Exchangers Market Forecast Predicts USD 8.92 Billion Valuation by 2034 at 8.40% CAGR

By sammkaran, 2026-06-26

The global industrial landscape is experiencing a massive shift toward sustainability and operational optimization, placing a renewed focus on energy-efficient thermal management systems. Air-cooled heat exchangers (ACHEs) crucial systems used to reject heat from a process fluid directly into the ambient air have emerged as a vital technology across multiple heavy industries. According to a comprehensive research study by The Insight Partners, the global market for these systems is poised for exponential growth over the next decade.

The Air-Cooled Heat Exchangers Market size is expected to reach US$ 8.92 Billion by 2034 from US$ 4.68 Billion in 2025.The market is estimated to record a CAGR of 8.40% from 2026 to 2034. This robust growth trajectory is heavily driven by increasing water scarcity, stricter environmental regulations regarding thermal pollution, and a widespread industrial push toward lowering operational costs.

Market Dynamics and Primary Growth Drivers

Traditional cooling systems heavily rely on water, such as shell-and-tube heat exchangers coupled with cooling towers. However, massive industrial expansion in water-scarce regions has made water conservation a top priority for global enterprises. Air-cooled heat exchangers present an eco-friendly and highly practical alternative because they eliminate the need for an external water supply, thereby removing costs associated with water treatment, chemical conditioning, and disposal.

Furthermore, regulatory frameworks worldwide are tightening constraints on thermal water discharge, which can disrupt aquatic ecosystems when hot water is released back into natural bodies. By utilizing ambient air as the cooling medium, industries can seamlessly comply with strict environmental mandates. Technological advancements are also reshaping the market landscape.Manufacturers are leveraging innovative designs, specialized finned configurations, and eco-friendly materials to dramatically boost thermal efficiency, allowing ACHEs to perform exceptionally well even in high ambient temperature environments.

Segmentation Overview

To provide a detailed outlook of the marketplace, the air-cooled heat exchangers market is categorized into distinct segments based on configuration, material, and end-use industry:

-

By Configuration: The market is analyzed across Forced Draft, Induced Draft, Horizontal, Vertical, and A-frame designs. Forced draft configurations are highly favored for their ease of maintenance and structural stability, while induced draft units offer superior air distribution and reduced hot air recirculation.

-

By Material: Material selection is vital for ensuring corrosion resistance and thermal conductivity. The market is segmented into Stainless Steel, Carbon Steel, and Copper, with stainless steel witnessing significant demand in corrosive or highly hygienic industrial processes.

-

By Industry: ACHEs serve as critical infrastructure across a diverse array of sectors, including Cement, Chemical, Pharmaceutical, Power, Steel, and Oil and Gas. The oil and gas and power generation sectors remain dominant consumers due to the massive scale of cooling required in refineries and thermal power plants.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00025309

Competitive Landscape and Key Players

The global air-cooled heat exchangers market features a blend of established engineering conglomerates and specialized thermal management providers. These entities are consistently investing in research and development, strategic partnerships, and geographic expansions to secure a competitive edge.

The key players operating in the market include:

-

Alfa Laval

-

Boldrocchi

-

Chart Industries

-

Fbm Hudson Italiana

-

Howden Group

-

Kawasaki Heavy Industries, Ltd.

-

Paharpur Cooling Towers Ltd.

-

SPG Dry Cooling

-

SPX Cooling Technologies, Inc.

-

Thermax Limited

These industry leaders focus on delivering customized, highly reliable, and heavy-duty thermal systems tailored to survive harsh operational environments, ranging from sub-zero arctic oil fields to scorching desert chemical plants.

Regional Market Insights

Geographically, the market spans North America, Europe, Asia-Pacific, South & Central America, and the Middle East & Africa. The United States represents a pivotal hub within North America, heavily supported by a booming oil and gas sector, expanding chemical processing facilities, and a rapid adoption of green technology.

Meanwhile, the Asia-Pacific region is projected to experience the fastest growth rate through 2034. Massive industrialization, continuous infrastructure development in nations like China and India, and the rising demand for electricity are triggering substantial investments in new power and steel manufacturing plants, fueling the regional demand for industrial cooling solutions.

Future Outlook

The future of the air-cooled heat exchangers market points toward hyper-efficiency and digital integration.As industries embrace digital transformation and the Industrial Internet of Things (IIoT), smart monitoring systems are revolutionizing ACHE maintenance.Future designs will increasingly incorporate artificial intelligence (AI) and advanced sensors to predict mechanical failures, monitor fouling, and dynamically adjust fan speeds based on real-time ambient weather conditions. This evolution will dramatically lower energy consumption and mitigate unplanned downtime. Combined with the global transition toward green technologies such as hydrogen production and carbon capture systems, both of which require specialized thermal management the demand for advanced, eco-friendly air-cooled heat exchangers is set to remain exceptionally strong, ensuring a sustainable and profitable horizon for manufacturers worldwide.

Related Reports-

Automotive Heat Exchanger Market

Air Separation Equipment Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

ICFM - Stock Market Institute is a leading platform for "Nism Exam Preparation", offering structured learning programs for beginners, traders, and investors who want to build strong financial market knowledge. The institute focuses on providing practical training in areas such as stock market courses, share market learning, technical analysis, fundamental analysis, trading strategies, and investment planning. With expert guidance and industry oriented education, ICFM helps students understand market concepts, risk management, and real-time trading practices to develop confidence in the financial sector. Whether you are a beginner looking for stock market basics or an advanced learner improving trading skills, ICFM delivers quality education with structured courses and expert mentorship.

Choosing the right platform for Nism Exam Preparation can help learners gain a better understanding of stock market opportunities and trading techniques. ICFM - Stock Market Institute provides industry-focused training with experienced mentors, updated learning modules, and practical approaches that help students learn how to analyze market trends and make informed decisions. Whether you are looking for stock market courses, trading classes, share market training, investment learning, or professional trader development programs, ICFM delivers quality education designed for real-world application. With a focus on skill development, market awareness, and financial growth, ICFM aims to create knowledgeable traders and investors who can confidently participate in today’s competitive stock market environment.

Key Highlights of ICFM – Stock Market Institute:

- Professional Stock Market Education & Training

- Practical Live Market Learning Approach

- Experienced Faculty & Industry-Based Guidance

- Wide Range of Stock Market Courses

- Career-Oriented Financial Market Learning Platform

Nism Exam Preparation – Introduction

NISM Exam Preparation is an essential step for individuals who want to build a strong career in the Indian securities market and financial industry. The National Institute of Securities Markets (NISM) certification exams are designed to test practical knowledge of stock markets, investment products, mutual funds, trading practices, risk management, and regulatory frameworks. A structured NISM exam preparation approach helps beginners, traders, investors, and finance professionals understand complex market concepts with proper guidance, study material, mock tests, and expert learning support. With the increasing demand for skilled professionals in the financial sector, NISM certification has become a valuable qualification for those aiming to improve their market knowledge and career opportunities.

Market Demand and User Benefits of Nism Exam Preparation

The growing interest in stock market investing, trading, mutual funds, and financial planning has increased the demand for certified professionals with updated market knowledge. NISM Exam Preparation provides learners with a clear understanding of market operations, securities regulations, technical concepts, and investment strategies required to perform confidently in the financial ecosystem. Proper preparation helps candidates improve exam performance, develop practical trading skills, and gain industry-relevant knowledge. Whether a user wants to start a career in stock broking, research analysis, wealth management, or improve personal investing skills, NISM certification preparation offers a structured pathway. It benefits students, working professionals, traders, and investors by enhancing credibility, improving decision-making abilities, and creating better opportunities in the finance and stock market industry.

ICFM stock market course generally covers:

- Basics of equity markets

- Trading psychology

- Technical analysis concepts

- Intraday trading strategies

- Swing trading concepts

- Options trading knowledge

- Practical market analysis

Professional traders commonly analyse:

- Price action

- Market trends

- Volume movements

- Chart formations

- Trading indicators

- Entry and exit levels

Professional options trading education helps learners understand:

- Call and put options

- Option premiums

- Market volatility

- Risk-controlled strategies

- Trading setups

Trading psychology teaches:

- Patience during market fluctuations

- Discipline while following strategies

- Avoiding emotional decisions

- Maintaining consistency

Why Choose a Professional ICFM - Stock Market Institute?

- Experienced market guidance

- Practical learning approach

- Structured course modules

- Trading strategy understanding

- Technical analysis training

- Continuous learning support

- Training Partner British Express

- BFSI Approved Institute

ICFM India provides stock market education programs designed for beginners and advanced learners who want to improve their understanding of financial markets.

Ask an Analyst: https://www.icfmindia.com/get-in-touch?utm_source=google&utm_medium=suraj&utm_campaign=leads&utm_content=backlink&utm_term=icfm%20trading%20course

Key Questions Answered in This Report?

- What is NISM Exam Preparation and why is it important?

- Who should prepare for NISM certification exams?

- What are the different types of NISM certification modules?

- How can beginners start NISM exam preparation effectively?

- What topics are covered in NISM certification exams?

- How does NISM certification help in building a finance career?

- What study methods are best for clearing the NISM exam?

- Why is practical market knowledge important for NISM preparation?

- How do mock tests improve NISM exam performance?

- What career opportunities are available after completing NISM certification?

- And more:

About Us:

ICFM - Stock Market Institute is a leading Stock Market Institute in India dedicated to providing professional and practical financial market education for beginners, traders, and investors. With a focus on stock market courses, trading education, technical analysis, fundamental analysis, and investment strategies, ICFM helps learners understand the concepts of equity markets, derivatives, intraday trading, and wealth creation. Our mission is to bridge the gap between theoretical knowledge and real market experience by offering structured learning programs designed according to industry requirements.

Located in India, ICFM - Stock Market Institute focuses on creating skilled market participants through expert guidance, practical training, and updated market knowledge. Whether you are looking for a stock market course for beginners, professional trading training, or advanced financial market learning, ICFM provides a simple and effective learning environment to build confidence in trading and investing. We aim to empower students with the right skills, strategies, and understanding needed to make informed decisions in the dynamic world of the stock market.

Contact Us:

ICFM - Stock Market Institute

Complex, U 135, Laxmi nagar, Infront of Gate No. 4,

Laxmi Nagar Metro Station, Delhi 110092

Email: info@icfmindia.com

Phone: +91 9871230635

Running a commercial kitchen requires more than preparing great food. Behind every successful restaurant is a well-maintained plumbing system that keeps operations running smoothly. One of the most important components of that system is the grease trap. Without proper care, grease traps can become clogged, cause unpleasant odors, slow drainage, and even lead to costly plumbing repairs or regulatory issues.

Understanding the importance of grease trap maintenance can help restaurant owners protect their plumbing, maintain compliance, and avoid expensive downtime. Whether you’re learning how to clean a grease traps, exploring professional restaurant grease trap cleaning services, or considering hydrojet drain cleaning for stubborn blockages, this guide covers everything you need to know.

What Is a Grease Trap?

A grease trap is a plumbing device designed to capture fats, oils, and grease (FOG) before they enter the sewer system. As wastewater flows from sinks, dishwashers, and kitchen equipment, the grease trap separates grease from water, allowing cleaner water to continue through the plumbing system.

Without a grease trap, grease can accumulate inside pipes, leading to severe blockages, unpleasant odors, and expensive plumbing emergencies.

Regular grease trap maintenance ensures that this essential equipment continues working efficiently while protecting both your business and the municipal sewer system.

Why Grease Trap Maintenance Is Essential

Many restaurant owners underestimate how quickly grease can build up inside a trap. Over time, layers of fats, oils, and food particles reduce the trap’s efficiency and increase the risk of plumbing issues.

Proper grease trap maintenance offers several important benefits:

- Prevents clogged drains

- Reduces foul kitchen odors

- Improves plumbing efficiency

- Extends the life of grease traps

- Helps businesses meet local health regulations

- Minimizes emergency plumbing repairs

- Creates a cleaner kitchen environment

Routine maintenance also supports smoother day-to-day operations by preventing unexpected interruptions during busy service hours.

Common Signs Your Grease Trap Needs Cleaning

Recognizing early warning signs can prevent larger plumbing problems.

Watch for symptoms such as:

- Slow-draining sinks

- Strong grease odors

- Frequent drain backups

- Overflowing grease trap

- Excess grease accumulation

- Gurgling drain sounds

- Standing water around floor drains

Ignoring these warning signs often results in more expensive repairs that could have been avoided through regular grease trap maintenance.

How to Clean a Grease Traps

One of the most frequently asked questions by restaurant owners is how to clean a grease traps properly.

While small grease traps may be cleaned in-house, larger commercial systems generally require professional servicing.

The basic cleaning process includes:

Step 1: Turn Off Kitchen Equipment

Before opening the grease trap, stop water flow into the system to prevent additional waste from entering during cleaning.

Step 2: Remove the Grease Trap Lid

Carefully remove the cover while avoiding damage to the gasket or lid.

Step 3: Inspect the Grease Trap

Measure the amount of grease and solids inside the unit.

If grease occupies approximately 25% of the trap’s capacity, cleaning is recommended.

Step 4: Remove Grease and Solid Waste

Use appropriate tools to remove floating grease, food particles, and sludge.

Dispose of waste according to local environmental regulations.

Step 5: Scrape Interior Surfaces

Clean the walls, baffles, and covers thoroughly to remove stubborn grease buildup.

Step 6: Wash the Interior

Rinse the trap using water while avoiding harsh chemicals that may damage plumbing or interfere with grease separation.

Step 7: Reassemble the Trap

Replace all components securely before restoring normal water flow.

Understanding how to clean a grease traps helps maintain efficient operation, but professional servicing is often recommended for commercial kitchens with heavy grease production.

Restaurant Grease Trap Cleaning: Why Professional Service Matters

Although basic maintenance can be performed regularly, professional restaurant grease trap cleaning provides a deeper level of service that helps prevent serious plumbing issues.

Professional technicians typically:

- Completely pump out grease traps

- Remove hardened grease deposits

- Clean internal components

- Inspect for damage

- Verify proper operation

- Dispose of waste responsibly

- Recommend maintenance schedules

Restaurants producing large amounts of grease benefit from scheduled professional cleaning to reduce the risk of unexpected system failures.

How Often Should Restaurant Grease Trap Cleaning Be Performed?

Cleaning frequency depends on several factors:

- Restaurant size

- Daily customer volume

- Kitchen equipment

- Menu type

- Grease production

General recommendations include:

Small Cafés

Every one to three months.

Medium Restaurants

Every one to two months.

High-Volume Restaurants

Monthly or more frequently if needed.

Rather than waiting for problems to occur, proactive restaurant grease trap cleaning helps maintain uninterrupted kitchen operations.

The Importance of Hydrojet Drain Cleaning

Even with regular grease trap maintenance, grease can gradually accumulate inside drain lines over time.

This is where hydrojet drain cleaning becomes extremely valuable.

Hydrojetting uses highly pressurized water to remove:

- Grease buildup

- Food residue

- Soap deposits

- Mineral scale

- Sludge

- Tree root intrusion (in applicable systems)

Unlike temporary drain-clearing methods, hydrojetting thoroughly cleans the interior walls of plumbing pipes.

Benefits of Hydrojet Drain Cleaning

Many restaurant owners choose hydrojet drain cleaning because it provides a more complete solution than conventional drain snaking.

Benefits include:

Thorough Pipe Cleaning

Pressurized water removes buildup from the entire pipe diameter.

Environmentally Friendly

Hydrojetting relies on water instead of harsh chemicals.

Improved Drain Flow

Clean pipes allow wastewater to move more efficiently.

Prevents Future Blockages

Removing grease completely reduces recurring clogs.

Extends Plumbing Life

Less buildup places less strain on commercial plumbing systems.

When combined with consistent grease trap maintenance, hydrojetting helps keep restaurant plumbing operating at peak performance.

Best Practices for Grease Trap Maintenance

Following good kitchen habits significantly reduces grease buildup.

Never Pour Grease Down the Sink

Collect used cooking oil separately for recycling or proper disposal.

Scrape Plates Before Washing

Removing food scraps reduces solid waste entering the grease trap.

Train Kitchen Staff