Blogs

Maintaining a healthy weight can be challenging in today's fast-paced world. Busy schedules, unhealthy eating habits, stress, and limited physical activity often make it difficult to achieve long-term wellness goals. While a balanced diet and regular exercise remain the foundation of successful weight management, many people choose dietary supplements to complement their healthy routines. LumiLean is one such supplement that has gained attention for its carefully selected blend of botanical extracts, vitamins, and minerals designed to support metabolism, appetite management, and overall well-being.

This article explores what LumiLean is, how it works, its ingredients, potential benefits, recommended usage, and important considerations before adding it to your daily routine.

What Is LumiLean?

LumiLean is a dietary supplement formulated to support healthy weight management through a combination of natural plant extracts and essential nutrients. Rather than promoting unrealistic promises, the supplement is designed to work alongside a nutritious diet and an active lifestyle.

The formula focuses on providing nutritional support that may help individuals maintain healthy metabolic function, improve energy production, and reduce unnecessary cravings. LumiLean is intended for adults who are looking for a convenient addition to their wellness routine while pursuing sustainable health goals.

How Does LumiLean Work?

LumiLean is developed with ingredients that have traditionally been used to support metabolic health and nutritional balance. Its formula aims to assist the body in several ways.

First, the supplement provides nutrients that contribute to normal energy metabolism. Efficient energy production allows the body to perform daily activities while supporting an active lifestyle.

Second, several botanical ingredients are included to help support healthy appetite control. Managing cravings can make it easier for individuals to maintain balanced eating habits and avoid unnecessary snacking.

Finally, the vitamins and minerals included in the formula contribute to overall wellness by supporting normal bodily functions, helping users maintain consistency in their health and fitness journey.

It is important to understand that LumiLean is not a magic solution for weight loss. Instead, it is intended to complement healthy eating, regular physical activity, adequate hydration, and quality sleep.

Key Ingredients in LumiLean

One of LumiLean's strengths is its combination of carefully selected ingredients that each play a unique role in supporting overall health.

Berberine

Berberine is a plant-derived compound that has been studied for its role in supporting healthy metabolic function and maintaining normal blood sugar levels already within the healthy range.

Cinnamon Extract

Cinnamon has long been valued for its antioxidant properties. It may help support healthy glucose metabolism and contributes to overall nutritional balance.

Fenugreek Extract

Fenugreek is commonly used in traditional wellness practices and may help support digestion while promoting a feeling of fullness after meals.

Red Yeast Rice Extract

Red yeast rice has been traditionally used to support cardiovascular health when combined with a healthy lifestyle. Individuals taking cholesterol-lowering medications should consult a healthcare professional before using products containing this ingredient.

Chromium

Chromium is an essential trace mineral that contributes to normal macronutrient metabolism and helps maintain normal blood glucose levels.

Magnesium

Magnesium supports hundreds of biochemical processes within the body, including muscle function, energy production, and nervous system health.

Calcium

Calcium is essential for maintaining healthy bones and also contributes to normal muscle function.

Vitamin D3

Vitamin D supports immune function, bone health, and normal muscle performance.

Vitamin E

Vitamin E acts as an antioxidant that helps protect cells from oxidative stress.

Vitamin B3 (Niacin)

Niacin contributes to normal energy metabolism and helps reduce tiredness and fatigue.

Biotin

Biotin supports the metabolism of carbohydrates, proteins, and fats while contributing to healthy skin and hair.

Selenium

Selenium plays an important role in protecting cells from oxidative damage while supporting normal thyroid function.

Potential Benefits of LumiLean

When combined with healthy lifestyle habits, LumiLean may provide several potential benefits.

-

Supports healthy metabolism.

-

Helps manage appetite and food cravings.

-

Contributes to normal energy production.

-

Provides essential vitamins and minerals.

-

Supports overall wellness and nutritional balance.

-

Vegan-friendly formulation.

-

Easy-to-use daily supplement.

Individual experiences may differ depending on diet, exercise habits, age, metabolism, and overall health.

Who Can Use LumiLean?

LumiLean may be suitable for adults who:

-

Want additional nutritional support while managing their weight.

-

Follow a balanced diet and regular exercise program.

-

Prefer plant-based supplement ingredients.

-

Wish to support healthy metabolism naturally.

-

Are looking for a convenient daily wellness supplement.

The supplement is generally not recommended for children. Pregnant or breastfeeding women and individuals with existing medical conditions should consult a healthcare professional before using LumiLean.

How to Take LumiLean

Users should always follow the dosage instructions provided on the product packaging or official website.

For best results:

-

Take the supplement consistently.

-

Drink plenty of water throughout the day.

-

Eat a balanced diet rich in fruits, vegetables, lean proteins, and whole grains.

-

Exercise regularly.

-

Get sufficient sleep each night.

-

Avoid relying solely on supplements for weight management.

Consistency is often more important than expecting immediate results.

Advantages of LumiLean

There are several reasons why users may choose LumiLean as part of their wellness routine.

-

Contains botanical extracts and essential nutrients.

-

Supports healthy metabolic function.

-

Includes vitamins that contribute to energy production.

-

Vegan-friendly formula.

-

Convenient daily supplementation.

-

Designed to complement healthy lifestyle habits.

Things to Consider

While LumiLean offers nutritional support, there are some important considerations.

-

Results vary from person to person.

-

It should not replace healthy eating or exercise.

-

Some ingredients may interact with medications.

-

Individuals with medical conditions should consult a healthcare provider before use.

-

Dietary supplements work best when combined with consistent healthy habits.

Are There Any Effects?

Most healthy adults can generally use dietary supplements according to the recommended directions. However, some individuals may experience mild digestive discomfort or ingredient sensitivities.

Anyone taking prescription medications or managing chronic health conditions should seek professional medical advice before starting any new supplement, particularly products containing botanical extracts.

Is LumiLean Worth Trying?

LumiLean offers a thoughtful combination of plant extracts, vitamins, and minerals that support overall wellness and healthy weight management. Instead of promising unrealistic weight loss, it encourages users to combine supplementation with proper nutrition, physical activity, and healthy daily habits.

People looking for a nutritional companion to support their fitness goals may find LumiLean to be a practical addition to their routine. As with any dietary supplement, maintaining realistic expectations and following a balanced lifestyle remain the keys to achieving long-term success.

Final Thoughts

Healthy weight management is a gradual process that requires consistency, patience, and commitment. LumiLean provides nutritional support through a blend of carefully selected ingredients that may assist metabolism, appetite management, and daily energy production.

While no supplement can replace healthy lifestyle choices, LumiLean can serve as a valuable part of a comprehensive wellness plan. By combining balanced nutrition, regular exercise, adequate hydration, and positive daily habits, users can work toward achieving sustainable health and fitness goals with greater confidence. https://lumilean.co.uk/

Air Traffic Management Market Share and Scope Analysis to Touch 16.56 Billion by 2034

By sammkaran, 2026-06-26

The global aviation landscape is undergoing an unprecedented evolution. As passenger volumes surge and commercial airlines expand their fleets, the complexity of managing global airspace has escalated dramatically. To keep pace with this demand, the global Air Traffic Management (ATM) industry is embracing sweeping structural and technological transformations.

According to a comprehensive industry report by The Insight Partners, the Air Traffic Management Market size is projected to reach US$ 9.85 Billion in 2025 and is expected to reach US$ 16.56 Billion by 2034. The market is expected to register a CAGR of 7.31% during the forecast period. This steady growth highlights an urgent, industry-wide push to modernize aging aviation infrastructure, optimize fuel consumption, and ensure the highest standards of safety across international borders.

Driving Forces Behind Modern Air Traffic Management

The growth of the ATM market is fueled by a combination of recovering passenger demand, regulatory mandates, and the emergence of new airborne technologies. Legacy radar-based control systems are gradually reaching their capacity limits. As a result, civil aviation authorities and airport operators worldwide are turning toward integrated digital platforms to maximize airspace efficiency.

Key drivers reshaping the ATM ecosystem include:

-

Airspace Congestion and Capacity Optimization: Major international hubs face daily bottlenecks that ripple across regional networks. Modern ATM systems utilize precise data analytics to sequence arrivals and departures closer together without compromising safety margins.

-

Decarbonization and Green Routing: Airlines are under immense pressure to lower carbon emissions. Advanced ATM software enables "Trajectory-Based Operations" (TBO), allowing aircraft to fly optimized, fuel-efficient paths rather than rigid, legacy airways.

-

Unmanned Traffic Integration: The rapid proliferation of commercial drones, logistics quadcopters, and Urban Air Mobility (UAM) concepts demands a unified infrastructure. Traditional ATM systems are evolving into Unmanned Traffic Management (UTM) ready ecosystems to manage low-altitude traffic.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00005933

Key Market Competitors

The global ATM landscape features a mix of aerospace giants, defense conglomerates, and specialized software developers providing hardware, communications networks, and surveillance systems. Prominent entities shaping the market include:

-

Advanced Navigation and Positioning Corporation

-

BAE Systems PLC

-

Harris Corporation

-

Honeywell International, Inc.

-

Intelcan Technosystems Inc.

-

Lockheed Martin Corporation

-

Raytheon Company

-

SAAB AB

-

Saipher ATC

-

Thales Group

These market participants focus heavily on collaborative partnerships with national Air Navigation Service Providers (ANSPs) to roll out next-generation software architectures, artificial intelligence diagnostic tools, and resilient cybersecurity frameworks.

Technical Innovations: Automation, Cloud, and AI

At the heart of the modern ATM transformation is the shift toward automation and digital twins. Traditional control towers are increasingly supplemented or replaced by Remote Digital Towers (RDTs). Using high-definition cameras, infrared sensors, and real-time telemetry, controllers can safely manage airport operations from hundreds of miles away—a breakthrough particularly beneficial for managing multiple low-volume regional airports from a centralized hub.

Furthermore, artificial intelligence is migrating from a theoretical tool to active operational support. AI algorithms analyze historical flight data, current weather conditions, and aerodynamic wake turbulence patterns to predict potential traffic conflicts up to an hour before they occur. This predictive capability shifts the air traffic controller's role from reactive management to proactive routing.

Regional Variations in Infrastructure Upgrades

The deployment of these systems varies significantly across geographic regions:

-

North America & Europe: Driven heavily by well-established modernization frameworks like NextGen (FAA) and SESAR (Single European Sky ATM Research). The focus in these regions centers on satellite-based navigation, digital data communications (Data Comm), and tight integration of cybersecurity layers to defend critical aviation networks.

-

Asia-Pacific & Middle East: Experiencing massive infrastructure investments due to new airport constructions and major fleet expansions by regional carriers. ANSPs in these markets are investing aggressively in high-capacity automation platforms and advanced surveillance tools to cope with some of the densest air corridors in the world.

Future Outlook

The future of the Air Traffic Management market points toward an interconnected, cloud-native aviation ecosystem. Over the coming decade, traditional siloed national architectures will give way to cross-border, cloud-based data sharing networks. This shift will allow for seamless regional flight handoffs and significantly reduced flight delays. Additionally, as machine learning algorithms assume greater responsibility for routine routing adjustments, human controllers will transition to strategic supervisors overseeing automated workflows. The integration of artificial intelligence, green flight paths, and low-altitude drone tracking will redefine global airspace, ensuring that the skies remain highly scalable, environmentally conscious, and safe for decades to come.

Related Reports-

Air Traffic Control Equipment Market

Commercial Air Traffic Management Market

About Us

The Insight Partners is a one-stop industry research provider of actionable intelligence. We help our clients in getting solutions to their research requirements through our syndicated and consulting research services. We specialize in industries such as Semiconductor and Electronics, Aerospace and Defense, Automotive and Transportation, Biotechnology, Healthcare IT, Manufacturing and Construction, Medical Devices, Technology, Media, and Telecommunications, as well as chemicals and Materials.

Contact Us

If you have any queries about this report or if you would like further information, don’t hesitate to get in touch with us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876

Reliable waste management is essential for maintaining cleanliness, hygiene, and environmental responsibility in both residential and commercial spaces.

With rapid growth in suburban areas, the demand for efficient waste management Brighton services has increased significantly.

Choosing the right provider is not just about getting your bins emptied; it’s about consistency, compliance, and long-term convenience.

A dependable bin collection service helps prevent overflow, supports recycling efforts, and ensures your property remains clean and safe.

Understanding Your Waste Collection Needs

Residential vs Commercial Requirements

Before selecting a provider, it’s important to understand your specific needs. Residential properties typically require regular household waste and recycling collection, while businesses may need more frequent pickups and specialised services.

Commercial waste often involves larger volumes and a range of materials, requiring structured handling and disposal. Choosing a provider that understands these differences ensures better service delivery.

Types of Waste You Generate

Not all waste is the same, and a reliable provider should handle multiple categories efficiently.

- General household waste

- Green waste, such as garden clippings

- Recyclables like paper, plastic, and glass

- Hard or bulk waste

A service that supports proper waste segregation contributes to better environmental outcomes and smoother collection processes.

Reliability and Consistent Collection Schedules

Why Timely Pickups Matter

One of the most important qualities of a dependable provider is consistency. Missed or delayed collections can quickly lead to overflowing bins, unpleasant odors, and hygiene issues.

A reliable company ensures your bins are collected on time, every time, without the need for constant follow-ups.

Evaluating Service Reliability

Look for providers with a proven track record of punctual service. Customer reviews and testimonials often reflect how consistently a company adheres to its schedules.

Choosing a service known for reliable waste collection in Tarneit helps avoid disruptions and ensures peace of mind.

Range of Bin Sizes and Service Flexibility

Choosing the Right Bin Size

Different households and businesses have different waste volumes. A dependable provider should offer a variety of bin sizes to suit your needs.

Whether you need a small bin for home use or a larger one for commercial waste, flexibility in options ensures efficiency and cost-effectiveness.

Flexible Services for Changing Needs

Your waste requirements may change over time. A good provider lets you easily upgrade or adjust your service.

This is especially useful for:

- Home renovations

- Events or gatherings

- Seasonal increases in waste

Flexible bin collection services ensure you’re never stuck with inadequate or excessive capacity.

Compliance with Local Waste Regulations

Following Council Guidelines

Waste management is governed by local regulations, and non-compliance can result in fines or environmental harm. A dependable bin collection provider ensures that all waste is handled in accordance with council rules.

This includes proper disposal methods, adherence to recycling standards, and compliance with environmental guidelines.

Licensed and Certified Services

Always choose a provider that is licensed and follows industry standards. This ensures your waste is being managed responsibly and legally.

Focus on Recycling and Sustainability

Importance of Eco-Friendly Waste Management

Sustainability is becoming a key consideration in waste management. A reliable provider should actively support recycling and environmentally friendly practices.

Reducing Landfill Waste

Providers that prioritise recycling help reduce the amount of waste sent to landfills. This includes proper sorting and processing of recyclable materials.

Choosing eco-friendly waste management Brighton services not only benefits the environment but also supports community sustainability goals.

Transparent Pricing and No Hidden Costs

Clear Cost Structure

Pricing transparency is essential when selecting a bin collection provider. You should know exactly what you’re paying for without unexpected charges.

A trustworthy provider offers clear pricing based on bin size, frequency, and service type.

Value Over Cheap Pricing

While affordability is important, extremely low prices may indicate poor service quality. It’s better to choose a provider that offers a balance between cost and reliability.

Customer Support and Service Responsiveness

Easy Communication Channels

A dependable provider should be easy to reach and responsive to your needs. Whether it’s rescheduling a pickup or addressing a missed collection, quick support makes a big difference.

Handling Urgent Requests

In some cases, you may need urgent waste removal. Providers offering same-day or emergency bin collection in Tarneit add an extra layer of convenience.

Good customer service ensures a smooth and stress-free experience.

Equipment Quality and Cleanliness Standards

Well-Maintained Bins and Vehicles

The condition of bins and collection vehicles reflects a provider's professionalism. Clean, well-maintained equipment helps prevent leaks, odors, and pest problems.

Hygiene and Safety

Regular cleaning and proper waste management are essential for maintaining hygiene standards. This is particularly important for businesses that generate large volumes of waste.

Experience and Local Expertise

Benefits of Choosing a Local Provider

A company with local experience understands the specific needs and challenges of the Tarneit area. This includes knowledge of routes, regulations, and community requirements.

Proven Industry Experience

Experienced providers are better equipped to handle different waste scenarios efficiently. Their expertise ensures reliable service and effective problem-solving.

Technology and Modern Waste Management Solutions

Smart Scheduling and Tracking

Modern waste management services use technology to improve efficiency. Features like GPS tracking and optimised routes ensure timely pickups and reduced delays.

Digital Booking and Management

Online booking systems and automated reminders make it easier to manage your bin collection schedule. This adds convenience and helps avoid missed services.

Customised Waste Management Plans

Tailored Solutions for Different Needs

Every property has unique waste management requirements. A dependable provider offers customised plans based on your usage and preferences.

Scalable Services

As your needs grow, your waste management plan should adapt. Whether it’s a growing business or changing household needs, scalable solutions ensure long-term convenience.

Safety and Environmental Responsibility

Safe Waste Handling Practices

Proper waste management is essential for protecting both people and the environment. A reliable provider follows strict safety protocols during collection and disposal.

Minimising Environmental Impact

Responsible waste management includes reducing pollution and supporting sustainable practices. Choosing a provider committed to environmental responsibility ensures your waste is handled ethically.

Conclusion

Selecting a dependable bin collection provider involves more than just comparing prices.

Reliability, flexibility, compliance, and sustainability all play a crucial role in ensuring effective waste management.

By understanding your needs and evaluating providers based on these factors, you can choose a service that delivers consistent and high-quality results.

Tidy Waste Management delivers professional and reliable waste management Brighton services designed to meet both residential and commercial needs.

With a strong focus on consistency, eco-friendly practices, and customer satisfaction, their team ensures waste is managed efficiently and responsibly.

From flexible service options to modern waste management solutions, tidywaste.com.au provides a seamless experience that supports cleanliness and sustainability across the community.

Don’t let waste management become a problem.

Contact Tidy Waste Management today to book your service and experience hassle-free, tailored waste management.

Choosing the right gift for children can be exciting, especially when you’re looking for something creative, engaging, and budget-friendly. A Makeup Set for Kids has become one of the most popular gift options because it encourages imaginative play while allowing children to express their creativity in a safe and age-appropriate way. Whether it’s for a birthday, holiday, or special reward, parents are increasingly choosing Kids Makeup products designed specifically for young users.

From washable lip glosses to colorful pretend cosmetics and Nail Polish For Kids, today’s children’s beauty products are made with non-toxic ingredients and are easy to remove, giving parents peace of mind. If you’re searching for the Best Gifts Under $25 For Kids, you’ll find plenty of affordable options that combine fun, creativity, and safety.

In this guide, we’ll explore why Kids Nail Polish Sets and makeup kits have become favorite gifts, what features to look for, and how to choose the perfect set for your little one.

Why a Makeup Set for Kids Is So Popular

Children naturally enjoy role-playing and copying the adults around them. A Makeup Set for Kids gives them the opportunity to explore their imagination while developing important life skills.

Some of the biggest benefits include:

- Encourages creative thinking

- Supports imaginative role play

- Builds confidence and self-expression

- Improves hand-eye coordination

- Creates opportunities for family bonding

- Provides hours of screen-free entertainment

Unlike adult cosmetics, quality Kids Makeup products are specially formulated to be gentle on young skin and are typically washable, making cleanup simple and stress-free.

What Makes Kids Makeup Different?

Many parents wonder if children’s makeup is actually safe. The answer depends on the product you choose.

A quality Kids Makeup kit is designed specifically for children and often includes:

- Water-based formulas

- Non-toxic ingredients

- Washable colors

- Gentle pigments

- Child-friendly applicators

- Bright, playful packaging

These features make children’s makeup much safer than allowing kids to use adult beauty products.

Nail Polish For Kids: A Favorite Activity

One of the biggest highlights of any children’s beauty kit is Nail Polish For Kids. Young children love decorating their nails with colorful shades, glitter finishes, and fun designs.

Unlike traditional nail polish, kid-friendly versions are usually:

- Water-based

- Peel-off

- Odor-free or low odor

- Easy to wash away

- Free from harsh chemicals

This makes Nail Polish For Kids an enjoyable activity that parents can feel comfortable supervising.

Kids can enjoy changing colors frequently without using strong nail polish removers.

Why Kids Nail Polish Sets Are Great Gifts

Among the most popular beauty toys today are Kids Nail Polish Sets. These sets often include everything children need for a fun mini manicure session.

Many Kids Nail Polish Sets include:

- Multiple polish colors

- Nail stickers

- Glitter decorations

- Mini nail files

- Toe separators

- Decorative gems

- Storage cases

These complete kits encourage creativity while keeping everything organized.

Children enjoy creating different nail styles for birthdays, playdates, sleepovers, and family gatherings.

Best Gifts Under $25 For Kids

Shopping on a budget doesn’t mean sacrificing quality. Many of the Best Gifts Under $25 For Kids provide incredible value while offering educational and creative benefits.

Popular affordable gift ideas include:

- Makeup Set for Kids

- Kids Nail Polish Sets

- Coloring kits

- Craft supplies

- Building blocks

- Puzzle games

- Art sets

- Storybooks

- DIY jewelry kits

- Science experiment boxes

These gifts help children learn through play while keeping costs affordable.

A thoughtfully selected Makeup Set for Kids easily fits into the category of the Best Gifts Under $25 For Kids, making it an excellent option for birthdays, holidays, and party favors.

Choosing the Right Makeup Set for Kids

Not every children’s beauty kit is the same. Parents should look for products designed specifically for younger users.

Important features include:

Non-Toxic Ingredients

Safety always comes first. Choose products that clearly state they are made with child-safe ingredients.

Washable Formula

Washable makeup makes cleanup easy and reduces mess.

Age-Appropriate Design

Always select products suitable for your child’s age.

Variety of Accessories

A complete Makeup Set for Kids often includes:

- Lip gloss

- Blush

- Eye shadow

- Brushes

- Nail polish

- Mirrors

- Cosmetic bag

The more variety included, the more creative possibilities children have.

Creative Play with Kids Makeup

Using Kids Makeup isn’t about encouraging beauty routines. Instead, it supports imaginative activities that help children develop creativity and communication skills.

Fun ideas include:

- Princess dress-up

- Fashion shows

- Birthday parties

- Pretend salons

- Family makeover games

- Puppet performances

- Theater role-play

These activities encourage storytelling, confidence, and imaginative thinking.

Nail Polish For Kids Encourages Creativity

Children enjoy experimenting with colors and patterns. Nail Polish For Kids gives them an opportunity to express their personality in a playful way.

Popular themes include:

- Rainbow nails

- Animal prints

- Glitter designs

- Holiday colors

- Flower patterns

- Heart stickers

- Cartoon-inspired styles

Since many children’s nail polishes peel off easily, kids can enjoy creating new looks whenever they want.

Kids Nail Polish Sets Make Perfect Party Activities

If you’re planning a birthday party, Kids Nail Polish Sets can provide hours of entertainment.

Popular party ideas include:

- Mini nail salon

- Beauty stations

- Design competitions

- Sticker decorating

- Glitter nail art

- Color matching games

Each child gets involved while expressing their creativity.

Parents also appreciate that these activities are calm, organized, and easy to supervise.

Why Parents Prefer Kids Makeup

Modern parents look for toys that offer educational value alongside entertainment.

A quality Kids Makeup kit supports:

- Creative exploration

- Fine motor development

- Independent decision-making

- Confidence building

- Social interaction

Instead of passive entertainment, children actively create, imagine, and interact with others.

Budget-Friendly Gift Ideas

Finding the Best Gifts Under $25 For Kids has become easier than ever.

Affordable options include:

- Makeup Set for Kids

- Kids Nail Polish Sets

- Watercolor painting kits

- DIY slime kits

- Plush toys

- Educational flash cards

- Puzzle collections

- Building sets

- Gardening kits

- Animal figurines

These gifts offer lasting value without exceeding your budget.

Tips for Parents

To ensure a positive experience:

- Supervise younger children during play.

- Test products on a small area of skin if your child has sensitivities.

- Teach children to avoid sharing makeup to promote good hygiene.

- Store cosmetics in a cool, dry place.

- Clean accessories regularly.

- Follow the manufacturer’s recommended age guidelines.

These simple steps help make playtime both safe and enjoyable.

Why Kids Love Makeup Sets

Children enjoy activities that let them pretend, create, and explore.

A Makeup Set for Kids provides:

- Endless imaginative play

- Colorful accessories

- Creative freedom

- Fun bonding moments with siblings and parents

- Confidence through self-expression

When paired with Nail Polish For Kids, children can enjoy a complete pretend beauty experience designed specifically for their age group.

The Growing Popularity of Kids Makeup

As parents increasingly seek toys that combine creativity with learning, Kids Makeup continues to grow in popularity. Modern sets are designed with safety, affordability, and fun in mind.

Many families appreciate that these kits encourage imaginative play instead of screen time, making them a valuable addition to any toy collection.

Whether children enjoy pretend fashion shows, salon games, or simply decorating their nails with colorful Kids Nail Polish Sets, these products create memorable experiences that encourage creativity and self-confidence.

Conclusion

A Makeup Set for Kids is more than just a fun toy — it’s a creative activity that helps children build imagination, confidence, and fine motor skills while enjoying safe, age-appropriate play. Combined with Nail Polish For Kids and colorful Kids Nail Polish Sets, these kits offer endless opportunities for role-playing and artistic expression.

If you’re searching for the Best Gifts Under $25 For Kids, a thoughtfully chosen Kids Makeup set offers excellent value, combining affordability, entertainment, and educational benefits. By selecting products made with child-friendly, washable, and non-toxic ingredients, parents can give children a fun gift that inspires creativity while providing peace of mind.

With the right set, every play session becomes an exciting adventure filled with imagination, colorful designs, and joyful memories.

Children love to express themselves through creativity, imagination, and role-playing. Whether they’re pretending to be a princess, a fashion designer, or simply enjoying a fun afternoon with friends, make up for kids has become one of the most exciting ways for young ones to explore their creative side. Designed with child-friendly ingredients and easy-to-use accessories, modern beauty products for kids offer safe entertainment while encouraging confidence and imaginative play.

Parents today are more mindful than ever when choosing products for their children. That’s why specially designed makeup sets for kids and nail polishes for kids are becoming increasingly popular. These products are created with gentle formulas, vibrant colours, and fun packaging that children adore while giving parents peace of mind.

Why Make Up for Kids Is Growing in Popularity

Playtime has evolved beyond traditional toys. Children now enjoy activities that encourage creativity, self-expression, and social interaction. Make up for kids provides a wonderful opportunity for children to explore colours, styles, and imagination in a completely age-appropriate way.

Unlike adult cosmetics, children’s makeup is specifically formulated to be gentle on delicate skin. Most products are washable, non-toxic, and designed for occasional play rather than daily cosmetic use. This makes them ideal for birthdays, sleepovers, school holidays, and dress-up games.

Parents also appreciate that makeup play can help children develop fine motor skills, creativity, and confidence while having fun.

Benefits of Makeup Sets for Kids

One of the biggest advantages of makeup sets for kids is that they combine several exciting beauty accessories into one complete package. Instead of purchasing individual items, parents can give children an all-in-one set filled with colourful surprises.

A quality kids’ makeup set often includes:

- Washable lip colours

- Gentle eye shadows

- Soft blush shades

- Child-safe brushes

- Glitter gels

- Fun mirrors

- Decorative accessories

These sets encourage children to experiment with colours in a safe environment while learning about creativity rather than appearance.

Because every item is designed specifically for young users, parents can feel much more comfortable allowing supervised makeup play.

Why Nail Polishes for Kids Are a Favourite

Among all children’s beauty products, nail polishes for kids remain one of the most loved options. Bright colours, sparkly finishes, and peel-off formulas make nail painting exciting without creating the mess or chemical exposure associated with traditional nail polish.

Unlike regular nail polish, many children’s versions are:

- Water-based

- Non-toxic

- Odour-free

- Easy to peel off

- Quick drying

This allows children to enjoy colourful nails during parties, family gatherings, or weekend fun without requiring harsh nail polish removers.

Many parents choose nail polishes for kids because they are simple, safe, and easy to clean, making them perfect for younger children.

Nail Polish Sets for Kids Make Every Occasion Special

Rather than purchasing a single bottle, many families prefer complete Nail Polish Sets for Kids. These colourful collections usually include multiple shades along with nail stickers, glitter decorations, nail files, and child-sized accessories.

A complete nail polish set allows children to:

- Mix different colours

- Create unique nail designs

- Decorate with stickers

- Practice creativity

- Enjoy salon-style fun at home

Whether it’s a birthday celebration, a rainy afternoon, or a weekend activity, Nail Polish Sets for Kids provide hours of entertainment while encouraging imagination.

Safe Beauty Products Designed for Children

Safety should always be the first consideration when purchasing children’s beauty products.

The best make up for kids products are created using ingredients suitable for young skin. Parents should always look for products that are:

- Dermatologically tested

- Non-toxic

- Washable

- Gentle on skin

- Easy to remove

- Free from harsh chemicals

Choosing trusted children’s beauty products helps ensure that fun never comes at the expense of safety.

Encouraging Creativity Through Pretend Play

Pretend play plays a significant role in childhood development. Whether children are pretending to run a beauty salon or getting ready for an imaginary party, makeup sets for kids help build confidence, communication skills, and creativity.

During pretend play, children often:

- Learn social interaction

- Improve storytelling skills

- Build confidence

- Express emotions

- Practice coordination

- Develop artistic abilities

Beauty-themed play becomes another enjoyable way to support healthy development.

Perfect Gift Ideas for Every Celebration

If you’re looking for a gift that children genuinely enjoy, beauty-themed toys continue to be one of the most popular options.

A complete collection including makeup sets for kids, nail polishes for kids, and colourful accessories makes an exciting surprise for:

- Birthdays

- Christmas

- School holidays

- Reward gifts

- Family celebrations

- Sleepovers

Parents love practical gifts that encourage creativity, while children love colourful products they can immediately enjoy.

Choosing the Right Makeup Sets for Kids

Not every children’s beauty product offers the same quality. Before purchasing, parents should consider several important factors.

Look for products that include:

- Child-safe ingredients

- Easy-to-clean formulas

- Colourful but gentle makeup

- Durable packaging

- Clearly labelled age recommendations

- Non-toxic certification

High-quality makeup sets for kids provide better value while offering a safer experience.

Fun Activities Using Nail Polish Sets for Kids

Children enjoy much more than simply painting their nails. Nail Polish Sets for Kids can become part of many creative activities.

Ideas include:

- Mini spa days

- Birthday party stations

- Fashion shows

- Dress-up afternoons

- Princess-themed parties

- Friendship activities

- Family craft days

These activities help children spend quality time together while expressing their imagination.

Building Confidence Through Creative Expression

Children naturally enjoy experimenting with colours, styles, and accessories. Safe make up for kids allows them to explore creativity without focusing on beauty standards.

Instead, these products encourage:

- Self-expression

- Artistic creativity

- Confidence

- Imagination

- Communication

- Play-based learning

Parents can join in the fun by supervising activities and turning beauty play into quality family time.

Why Parents Choose Kids Beauty Products

Today’s parents look for products that combine safety, education, and entertainment.

Modern nail polishes for kids and makeup sets for kids offer exactly that. Children enjoy hours of imaginative play while parents appreciate products specifically designed for younger users.

Instead of copying adult beauty products, these collections celebrate creativity through colourful, washable, and child-friendly designs.

The Future of Children’s Beauty Play

The popularity of make up for kids continues to grow because it combines imagination with creativity in a safe and enjoyable way. New collections now feature brighter colours, eco-friendly packaging, washable formulas, and exciting accessories that keep children entertained.

From beginner makeup kits to complete Nail Polish Sets for Kids, families now have more options than ever to support imaginative play.

Whether it’s for a birthday gift, weekend activity, or special celebration, choosing high-quality makeup sets for kids and nail polishes for kids creates memorable experiences children will love.

Final Thoughts

Creative play is one of the most valuable parts of childhood, and beauty-themed activities offer children another exciting way to learn, imagine, and have fun. By choosing safe, washable, and age-appropriate make up for kids, parents can encourage creativity while ensuring peace of mind.

Complete makeup sets for kids, colourful nail polishes for kids, and exciting Nail Polish Sets for Kids make excellent gifts that combine entertainment, creativity, and quality family time. With child-friendly formulas and endless possibilities for imaginative play, these products continue to bring smiles to children and confidence to parents, making every play session colourful, safe, and unforgettable.

In today's competitive marketplace, ios app development ireland is playing a major role in helping businesses connect with customers and deliver exceptional digital experiences. Companies are increasingly investing in mobile technology and online strategies to strengthen their brand presence and stay ahead of changing consumer expectations.

The Growing Importance of Digital Innovation

Technology has transformed the way businesses operate. Consumers now expect instant access to information, products, and services through their mobile devices. This shift has encouraged organizations to adopt digital solutions that improve communication and create more convenient experiences for customers.

Digital innovation is no longer limited to large enterprises. Small and medium-sized businesses are also embracing technology to expand their reach and improve operational efficiency. Investing in digital tools can help organizations respond quickly to market changes and customer demands.

Mobile Applications as a Business Asset

Mobile applications have become an essential part of business growth strategies. They allow organizations to provide personalized services, improve customer support, and create seamless purchasing experiences.

Customers appreciate the convenience of having services available at their fingertips. Whether they are making purchases, booking appointments, or accessing important information, mobile applications make interactions faster and more efficient.

A well-designed app can also strengthen customer loyalty. Features such as notifications, reward programs, and personalized recommendations encourage users to engage with a business regularly and build long-term relationships.

Building a Strong Online Presence

Having a great product or service is not enough in today's digital environment. Businesses must also ensure that potential customers can easily find them online. This is where effective digital marketing strategies become essential.

Search engine optimization Ireland has become an important consideration for organizations that want to increase visibility and attract organic traffic. Optimizing digital content helps businesses improve their online presence and connect with customers who are actively searching for relevant solutions.

A strong online presence also builds credibility and trust. Consumers often research businesses before making purchasing decisions, making digital visibility a critical factor in long-term success.

Understanding Customer Expectations

Customer expectations continue to evolve as technology advances. People want quick responses, simple navigation, and personalized experiences across all digital platforms.

Businesses that understand these expectations are better positioned to create meaningful interactions with their audience. By analyzing customer behavior and preferences, organizations can develop solutions that meet specific needs and improve satisfaction.

Listening to customer feedback and making continuous improvements are also important aspects of maintaining a positive digital experience.

Also, Read

Blockify Fatal Error in WordPress: Easy Fix & Prevention Guide

The Role of Data in Business Growth

Data has become one of the most valuable resources for modern businesses. Every customer interaction provides information that can help organizations improve their products, services, and marketing strategies.

Analyzing data enables businesses to identify trends, measure performance, and make informed decisions. Companies that effectively use data often gain a better understanding of their customers and can develop strategies that lead to increased engagement and profitability.

Data-driven decision-making also allows businesses to allocate resources more effectively and identify opportunities for future growth.

Adapting to Future Trends

The digital landscape is constantly changing, and businesses must remain flexible to stay competitive. Emerging technologies, changing consumer habits, and new communication channels continue to create opportunities and challenges.

Organizations that embrace innovation are better prepared to adapt to these changes. Investing in digital transformation today can create a strong foundation for future success and help businesses remain relevant in an increasingly connected world.

Continuous learning and a willingness to adopt new technologies are essential for long-term growth. Businesses that prioritize innovation are more likely to achieve sustainable success and maintain a competitive advantage.

Conclusion

Technology has become a driving force behind modern business growth. Mobile applications, strong digital visibility, and customer-focused strategies are helping organizations improve efficiency and build lasting relationships with their audiences.

As the digital economy continues to evolve, businesses that invest in innovative solutions and adapt to changing trends will be better positioned to succeed. Embracing technology is not just about keeping up with competitors; it is about creating meaningful experiences that support long-term growth and customer satisfaction.

Explore the opportunities Quantum IT Innovation brings to your business contact their team today and consult with our experts.

LumiLean is a dietary supplement designed to support healthy weight management and overall wellness as part of a balanced lifestyle. It is intended to complement, not replace, nutritious eating habits, regular physical activity, adequate hydration, and sufficient sleep. Many people exploring weight management supplements are looking for additional support in maintaining healthy routines, and LumiLean is promoted as one option that may fit into a broader wellness plan depending on its specific formulation. Because ingredient blends can differ between products, it is important for consumers to carefully review the product label, understand the recommended serving size, and familiarize themselves with any precautions or potential interactions. Individuals who are pregnant, breastfeeding, taking prescription medications, or living with underlying medical conditions should consult a qualified healthcare professional before using LumiLean or any other dietary supplement. Consistency plays an important role in achieving long-term health goals, and supplements generally work best when paired with healthy daily habits rather than relied upon as standalone solutions. A well-rounded approach that includes meals rich in vegetables, fruits, lean proteins, whole grains, and healthy fats can provide essential nutrients while supporting overall well-being. Regular exercise, whether through walking, strength training, cycling, or other enjoyable activities, also contributes significantly to maintaining a healthy weight and improving fitness. Additionally, managing stress and getting adequate sleep are often overlooked but essential aspects of a successful wellness routine. Individual responses to dietary supplements vary because factors such as age, metabolism, genetics, activity level, and overall health influence results. Some users may notice changes sooner than others, while some may experience little difference. Keeping realistic expectations and focusing on gradual, sustainable progress can help maintain motivation over time. Purchasing LumiLean from trusted retailers or authorized sellers can help ensure product authenticity and proper labeling. Users should also store the supplement according to the manufacturer's recommendations and keep it out of the reach of children. If any unexpected side effects or adverse reactions occur, discontinue use and seek medical advice promptly. Consumers are encouraged to evaluate product claims carefully and rely on credible, evidence-based information when making decisions about dietary supplements. No supplement has been proven to produce effortless or guaranteed weight loss without healthy lifestyle changes, and products should not be viewed as miracle solutions. Instead, LumiLean may serve as one supportive element within a comprehensive wellness strategy that prioritizes balanced nutrition, regular movement, hydration, sleep, and ongoing self-care. By following the recommended directions, consulting healthcare professionals when appropriate, and maintaining healthy habits over time, individuals can make informed decisions about incorporating LumiLean into their personal wellness routines. A patient, consistent, and realistic approach is generally the most effective path toward achieving and maintaining long-term health and weight management goals, while ensuring safety remains a top priority throughout the journey. https://lumilean.co.uk/

The stone fabrication industry relies on precision, efficiency, and high-quality tools to deliver outstanding results. Whether working with granite, marble, quartz, porcelain, or engineered stone, professionals understand that every stage of fabrication requires specialized equipment and materials. From accurate cutting to flawless polishing, selecting the right Blades, Bridge Saw Blades, Chemicals, Grinding & Sanding tools, and Polishing Pads can significantly improve productivity and the final finish.

As customer expectations continue to rise, fabricators must invest in reliable products that enhance performance while reducing downtime and operational costs. Modern manufacturing technologies have transformed stone processing, making premium tooling an essential part of every successful workshop.

Why Quality Stone Fabrication Tools Matter

Stone fabrication is a highly technical process where precision is everything. Inferior tools often result in chipped edges, uneven finishes, increased waste, and frequent replacements. High-quality fabrication products are designed to withstand demanding workloads while delivering consistent performance.

Using professional-grade equipment offers several advantages:

- Greater cutting accuracy

- Improved production speed

- Longer tool lifespan

- Reduced material waste

- Superior surface finishes

- Lower maintenance costs

- Increased customer satisfaction

By investing in trusted fabrication solutions, businesses can improve efficiency and maintain a competitive advantage in today’s stone industry.

Choosing the Right Blades for Every Stone Cutting Project

Every fabrication project begins with selecting the proper Blades. Since different materials have varying hardness levels and cutting requirements, choosing the appropriate blade ensures cleaner cuts and longer service life.

Premium blades are engineered using advanced diamond technology that allows them to maintain sharpness even during continuous production. They are suitable for cutting:

- Granite

- Marble

- Quartz

- Porcelain

- Engineered stone

- Natural stone

- Ceramic materials

High-performance blades reduce vibration during operation, resulting in smoother cuts and minimizing edge chipping. Fabricators also benefit from faster cutting speeds, improved operator safety, and consistent results across multiple applications.

Selecting the right blade for each project helps maximize productivity while preserving valuable stone materials.

How Bridge Saw Blades Improve Precision and Productivity

Among all cutting tools, Bridge Saw Blades play a critical role in large-scale stone fabrication. Bridge saw machines demand blades capable of maintaining precise cutting accuracy while operating under heavy workloads.

Modern bridge saw blades are specifically designed for industrial applications where consistency and durability are essential.

Key benefits include:

- Smooth and accurate straight cuts

- Reduced edge chipping

- Excellent cutting speed

- Long operational life

- Stable performance on hard stone surfaces

- Lower vibration during cutting

Fabricators processing granite countertops, marble slabs, quartz surfaces, and porcelain panels depend on premium bridge saw blades to deliver reliable performance day after day.

When paired with properly maintained machinery, high-quality bridge saw blades help increase production efficiency while minimizing costly material waste.

The Essential Role of Chemicals in Stone Fabrication

Cutting and polishing are only part of the fabrication process. Professional Chemicals help protect, clean, strengthen, and enhance natural and engineered stone surfaces throughout manufacturing and installation.

Stone fabrication chemicals include products designed for:

- Surface cleaning

- Stone sealing

- Adhesives

- Color enhancement

- Crack repair

- Joint filling

- Surface protection

- Maintenance

Using premium chemicals ensures stronger bonding, improved durability, and longer-lasting finishes. These products also help fabricators deliver installations that resist stains, moisture, and everyday wear.

High-quality stone chemicals contribute to both the appearance and longevity of finished projects, making them indispensable in professional fabrication.

Achieving Smooth Surfaces with Grinding & Sanding

After cutting, stone surfaces require refinement before polishing. This is where professional Grinding & Sanding products become essential.

Grinding removes saw marks, levels uneven surfaces, and prepares stone for polishing. Sanding creates progressively smoother finishes while maintaining dimensional accuracy.

Professional grinding and sanding solutions provide:

- Consistent material removal

- Better surface preparation

- Reduced scratches

- Enhanced polishing results

- Increased productivity

- Extended equipment life

Different grit levels are used depending on the fabrication stage. Coarse abrasives remove excess material quickly, while finer grits prepare the surface for high-gloss finishing.

Using premium grinding and sanding products minimizes defects while improving overall workflow efficiency.

Why Polishing Pads Are Essential for Professional Finishes

The final appearance of any stone project depends heavily on the quality of the Polishing Pads used during finishing.

Professional polishing pads gradually refine the stone surface until it achieves the desired level of gloss. Whether the project requires a matte, satin, semi-gloss, or mirror finish, selecting the appropriate polishing pad is essential.

Premium polishing pads offer several advantages:

- Excellent gloss development

- Uniform surface finish

- Faster polishing cycles

- Longer working life

- Reduced heat generation

- Suitable for wet and dry polishing applications

Fabricators working with granite, marble, quartz, and porcelain rely on high-quality polishing pads to produce visually stunning results that exceed customer expectations.

The right polishing pads also reduce operator fatigue while maintaining consistent polishing performance throughout extended production runs.

Combining Quality Products for Maximum Efficiency

Every stage of stone fabrication depends on the previous one. Using premium products throughout the entire workflow creates better overall results.

A typical fabrication process includes:

- Precision cutting using professional Blades

- Large slab processing with premium Bridge Saw Blades

- Surface refinement through Grinding & Sanding

- Finishing with high-performance Polishing Pads

- Protection and installation using professional Chemicals

This integrated approach improves workflow, reduces production errors, and ensures consistent quality from raw material to finished installation.

Selecting the Right Products for Different Stone Materials

Different materials require specialized tooling to achieve optimal performance.

Granite

Granite is extremely hard and abrasive, requiring durable blades, efficient grinding tools, and long-lasting polishing pads capable of handling heavy workloads.

Marble

Marble is softer but more delicate. Precision blades and fine polishing pads help maintain clean edges while producing elegant finishes.

Quartz

Quartz surfaces require specialized bridge saw blades and polishing solutions designed to minimize chipping and preserve surface integrity.

Porcelain

Porcelain slabs demand advanced cutting technology due to their hardness and brittleness. Premium blades and polishing pads help produce precise cuts with smooth finishes.

Selecting products designed specifically for each material increases efficiency while reducing costly mistakes.

Improving Productivity Through High-Performance Tooling

Modern fabrication shops face increasing pressure to complete projects faster without sacrificing quality.

High-performance fabrication products contribute by:

- Reducing cutting time

- Extending tool life

- Minimizing downtime

- Lowering replacement costs

- Producing cleaner finishes

- Improving operator confidence

- Supporting higher production volumes

Reliable tooling enables businesses to complete more projects while maintaining exceptional workmanship.

Maintaining Stone Fabrication Equipment

Even premium tools require proper maintenance to achieve maximum performance.

Best practices include:

- Inspect blades regularly for wear.

- Clean bridge saw blades after heavy use.

- Store chemicals according to manufacturer recommendations.

- Replace worn grinding abrasives promptly.

- Keep polishing pads clean between applications.

- Follow recommended operating speeds.

- Use adequate cooling during cutting and polishing.

Routine maintenance helps extend product life while ensuring consistent fabrication quality.

Meeting Customer Expectations with Superior Results

Today’s customers expect precision, durability, and flawless finishes. Delivering these results depends on using professional-grade products throughout every fabrication stage.

Whether producing kitchen countertops, flooring, wall cladding, monuments, staircases, or commercial installations, premium fabrication tools help businesses exceed expectations while building long-term customer trust.

Investing in quality Blades, Bridge Saw Blades, Chemicals, Grinding & Sanding products, and Polishing Pads allows fabricators to produce exceptional workmanship while improving operational efficiency.

Conclusion

Success in the stone fabrication industry depends on precision, consistency, and the right equipment. Every step — from cutting and shaping to finishing and protection — requires products that are engineered for performance and reliability.

By choosing premium Blades, durable Bridge Saw Blades, professional Chemicals, advanced Grinding & Sanding solutions, and high-quality Polishing Pads, fabricators can improve productivity, reduce waste, and achieve outstanding finishes on granite, marble, quartz, porcelain, and other stone materials.

Businesses that invest in dependable fabrication solutions are better positioned to deliver superior craftsmanship, strengthen customer relationships, and remain competitive in a growing global market.

Modern businesses move fast. New partnerships, digital platforms, vendor relationships, and expanding customer expectations create opportunities — but they also introduce legal complexity. Whether a company is launching a product, entering a new market, negotiating partnerships, or managing intellectual property, having the right legal structure in place can protect growth and reduce costly mistakes.

Many businesses wait until legal issues appear before seeking help. In reality, proactive legal guidance can become a competitive advantage. Working with a business contract lawyer, engaging a fractional general counsel, and creating strong protections through a software license agreement can help organizations operate more confidently while staying focused on growth.

The Modern Business Environment Requires Strong Legal Foundations

Business growth creates legal obligations that often become more complex over time. Early-stage companies may begin with simple agreements and informal processes, but expansion quickly introduces new concerns:

- Vendor and supplier contracts

- Customer agreements

- Technology licensing

- Intellectual property protection

- Employment obligations

- Compliance requirements

- Risk management policies

Without a structured legal strategy, businesses may face delays, disputes, unexpected liabilities, or lost opportunities.

This is where strategic legal support becomes valuable — not just for solving problems, but for preventing them.

The Role of a Business Contract Lawyer in Long-Term Success

Contracts influence nearly every aspect of a business. From negotiating partnerships to defining service expectations, clear agreements reduce confusion and protect business interests.

A business contract lawyer helps organizations create, review, negotiate, and manage legally enforceable agreements that align with business objectives.

Key Areas Where Contract Support Matters

1. Contract Drafting and Review

Generic templates often fail to address the specific risks associated with a company’s operations. Customized agreements help ensure that terms are clear, enforceable, and aligned with commercial goals.

Common agreements include:

- Service agreements

- Partnership contracts

- Supplier agreements

- Non-disclosure agreements

- Independent contractor agreements

- Technology agreements

Professional contract drafting reduces ambiguity and strengthens business relationships.

2. Risk Identification and Prevention

Many legal disputes originate from unclear language or missing protections.

A business contract lawyer can identify concerns related to:

- Payment structures

- Liability limitations

- Ownership rights

- Termination conditions

- Performance obligations

- Confidentiality clauses

Preventive legal planning often costs less than resolving disputes later.

3. Negotiation Support

Business negotiations are not simply about securing favorable pricing. They involve balancing operational flexibility, legal protection, and long-term sustainability.

Legal guidance during negotiations helps businesses maintain leverage while avoiding unnecessary exposure.

Why Businesses Are Turning to Fractional Legal Leadership

Hiring a full-time in-house legal team may not be practical for every company. Growing organizations often need strategic legal oversight without committing to permanent executive-level legal staffing.

This is where a fractional general counsel provides significant value.

A fractional legal model allows companies to access experienced legal leadership on a flexible basis while maintaining operational efficiency.

What Does a Fractional General Counsel Do?

A fractional general counsel acts as an embedded legal advisor who supports executive decision-making and business strategy.

Responsibilities commonly include:

- Managing legal risk

- Overseeing contract processes

- Supporting business expansion

- Advising on compliance initiatives

- Coordinating external legal providers

- Improving governance practices

Unlike project-based legal services, this approach creates continuity and strategic alignment.

Benefits of Working with a Fractional General Counsel

Cost Efficiency

Companies gain access to experienced legal leadership without the overhead associated with a full-time executive hire.

Strategic Decision Support

Legal decisions affect operations, sales, marketing, partnerships, and technology. Ongoing legal guidance supports better business decisions.

Faster Contract Cycles

Organizations often experience delays when agreements move through fragmented review processes. Centralized legal oversight improves turnaround time.

Scalable Support

As businesses evolve, legal priorities shift. A fractional general counsel provides adaptable support that grows alongside the company.

Technology Growth Makes Software Agreements More Important Than Ever

Software has become central to business operations. Whether companies build technology internally, license platforms, or sell digital products, legal protection around software usage is essential.

One of the most important legal tools in technology-driven business environments is the software license agreement.

Understanding the Purpose of a Software License Agreement

A software license agreement establishes the terms under which software can be used, distributed, modified, or accessed.

Without a properly structured agreement, businesses may expose themselves to:

- Intellectual property disputes

- Unauthorized usage

- Revenue leakage

- Compliance challenges

- Security concerns

Well-defined licensing terms protect both software owners and users.

Essential Components of a Strong Software License Agreement

Scope of Use

The agreement should clearly define:

- Who may use the software

- Usage limitations

- Device restrictions

- Geographic limitations

Clear boundaries reduce misunderstandings.

Intellectual Property Ownership

Software ownership provisions determine who retains rights over source code, updates, customizations, and related assets.

Strong ownership language protects long-term business value.

Payment and Licensing Terms

Licensing models may include:

- Subscription pricing

- One-time licensing

- Usage-based structures

- Enterprise agreements

The agreement should explain payment obligations and renewal procedures.

Confidentiality Requirements

Technology agreements often involve sensitive business information.

Confidentiality provisions help protect:

- Source code

- Customer data

- Product roadmaps

- Technical documentation

Liability and Warranty Terms

Every agreement should define responsibilities and allocate risk appropriately.

Well-drafted limitation clauses create clarity during disputes.

How Contract Management Supports Business Growth

Contracts should not remain forgotten after signing.

Effective organizations treat agreements as operational assets.

Legal oversight helps businesses:

- Monitor deadlines

- Track renewals

- Manage obligations

- Reduce compliance risks

- Improve forecasting

Combining support from a business contract lawyer with strategic leadership from a fractional general counsel creates a more organized contract lifecycle.

Creating Alignment Between Legal and Business Strategy

Successful businesses integrate legal planning into broader operational decisions.

Rather than approaching legal services reactively, companies benefit from asking:

- Are our agreements supporting revenue goals?

- Are technology assets protected?

- Are growth initiatives creating avoidable risk?

- Are responsibilities clearly documented?

When legal and business functions align, organizations become more resilient.

A business contract lawyer supports transaction-level execution, while a fractional general counsel helps shape company-wide legal strategy.

Together, they establish systems that improve consistency and decision-making.

Common Mistakes Businesses Should Avoid

Even sophisticated companies sometimes overlook important legal considerations.

Relying on Generic Templates

Template agreements may overlook business-specific risks and obligations.

Delaying Legal Review

Waiting until negotiations are complete limits flexibility and increases risk.

Ignoring Software Licensing Terms

Weak licensing language can create ownership and enforcement problems.

A detailed software license agreement helps establish clear rights and expectations.

Treating Legal as a One-Time Expense

Legal planning should evolve alongside business operations.

Ongoing strategic guidance often produces stronger outcomes than occasional emergency support.

Building a Scalable Legal Framework

Companies that grow sustainably often invest early in legal infrastructure.

An effective framework typically includes:

- Standardized contract processes

- Defined approval workflows

- Legal review checkpoints

- Technology governance

- Risk monitoring systems

- Contract lifecycle management

With the right systems in place, businesses gain confidence to pursue expansion opportunities while maintaining stronger protection.

Final Thoughts

Business growth creates opportunities, but it also increases legal complexity. Organizations that prioritize proactive legal planning position themselves to operate more efficiently, reduce disputes, and protect valuable assets.

Working with a business contract lawyer can strengthen agreements and improve negotiation outcomes. Engaging a fractional general counsel provides strategic legal direction that scales with the organization. Establishing a well-structured software license agreement helps protect technology investments and clarify business relationships.

When these elements work together, companies create a legal foundation that supports sustainable growth, operational clarity, and long-term success.

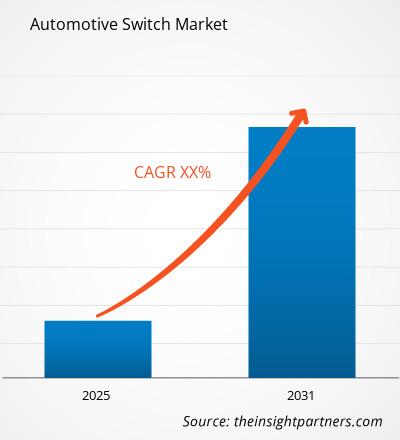

Automotive Switch Market Outlook and Forecast Predicting 79.29 Billion US Dollars at 4.08% CAGR

By sammkaran, 2026-06-26

The automotive industry is undergoing a monumental shift, transitioning from traditional mechanical engineering to software-defined, highly connected vehicles. At the heart of this evolution lies the automotive switch a seemingly basic component that serves as the crucial interface between the vehicle's driver, passengers, and its electronic ecosystem. As modern vehicles adopt increasingly sophisticated electronic architectures, the automotive switch market is witnessing consistent and healthy growth.

The Automotive Switch Market is expected to register a CAGR of 4.08% from 2026 to 2034, with the market size expanding from US$ 55.33 Billion in 2025 to US$ 79.29 Billion by 2034. This growth is fueled by a combination of stricter automotive safety mandates, an increase in standard electronic comfort features, and the global adoption of electric vehicles (EVs).

Market Dynamics and Drivers

A key catalyst accelerating the automotive switch market is the massive influx of consumer electronic features into cars. Today’s consumers demand the same level of touchscreen responsiveness, ambient lighting control, and digital convenience in their vehicles that they experience with smartphones and tablets. Consequently, conventional toggle and rotary switches are rapidly making way for smart touchpads, haptic feedback buttons, and multi-functional steering wheel controls.

Furthermore, the electrification of vehicles plays an instrumental role. Electric vehicles utilize sophisticated electronic control units (ECUs) to manage everything from battery cooling systems to advanced driver-assistance systems (ADAS). This expansion of a vehicle's electrical framework naturally requires an increased quantity of high-voltage and low-voltage switches to reliably regulate power and signal transmission.

Safety regulations mandated by governments globally also serve as a vital market driver. Standards requiring standard inclusion of backup cameras, electronic stability control, and automated emergency braking systems necessitate a dense array of sensory and manual override switches inside the cabin and under the hood.

Segmentation Overview

The automotive switch market can be segmented based on switch type, application, vehicle type, and geography. By switch type, the market includes push-button switches, toggle switches, rotary switches, and multi-function steering switches. Among these, multi-function steering and haptic smart switches are gaining substantial market share due to their role in reducing driver distraction.

In terms of application, switches are widely classified into powertrain systems, chassis systems, body electronics, and infotainment systems. The body electronics and comfort systems segment accounts for a considerable share, driven by features like power windows, electronic seat adjustments, sunroof controls, and motorized mirrors. By vehicle type, the passenger car segment continues to lead the demand, though commercial vehicles are gradually catching up as logistics companies upgrade to telematics-equipped smart trucks.

Get a PDF Sample– https://www.theinsightpartners.com/sample/TIPRE00023840

Competitive Landscape: Key Market Players

The global automotive switch market is highly competitive and characterized by the presence of prominent tier-1 automotive suppliers and electronics manufacturers. These enterprises are actively focusing on strategic product launches, lightweight component designs, and smart switch technologies to sustain their market positions.

The key players dominating this market landscape include:

-

Alps Electric Co., Ltd.

-

Continental AG

-

Hella KGaA Hueck and Co.

-

Johnson and Johnson

-

Omron Corporation

-

Panasonic Corporation

-

Robert Bosch GmbH

-

Tokai Rika Co., Ltd.

-

Valeo

-

ZF Friedrichshafen AG

These industry leaders heavily invest in Research and Development (R&D) to engineer switches capable of handling harsh automotive conditions such as extreme temperatures, high vibration, and moisture while maintaining ergonomic and aesthetic appeal.

Regional Analysis

Geographically, Asia-Pacific remains the powerhouse of the automotive switch market. The region’s dominance is anchored by massive automotive production hubs in China, Japan, India, and South Korea. Increased consumer spending power, paired with a rising demand for premium passenger cars featuring advanced cabin comfort, further accelerates the regional market.

Europe and North America represent highly mature markets. In these regions, growth is heavily supported by rigid safety standards and a swift consumer transition toward premium luxury electric vehicles. Original Equipment Manufacturers (OEMs) in Europe and North America are focusing tightly on integrating intelligent touch-capacitive panels, forcing traditional switch manufacturers to modernize their current portfolios.

Future Outlook